Analysis: Launching a $201MM SPAC for Fintech, AI, and Crypto

The next SPAC cycle is being built around companies with real revenue, not pandemic-era projections.

Gm Fintech Architects —

Today we are diving into the following topics:

Summary: In this article, we discuss the launch of $IPVV, a $201M SPAC that target high-growth companies across fintech, digital assets, AI, and the machine economy. We argue that a growing backlog of venture-backed companies remains private despite reaching meaningful scale, while weak venture DPI and a constrained IPO market have created demand for alternative liquidity pathways. We review the SPAC structure, and note that today’s SPAC market is materially smaller than the 2020–2021 booms. We conclude that the next generation of SPAC targets is likely to be profitable or near-profitable companies with $50–250MM of revenue and $1–5B valuations rather than the pre-revenue growth stories that defined the prior cycle.

Topics: InterPrivate, Generative Ventures, Aeva, Microvast, Securitize, Abra, Animoca Brands, Kraken, Cantor Fitzgerald, BlackRock, Anthropic, OpenAI, SpaceX

To support this writing and access our full archive of newsletters, analyses, and guides to building in the Fintech & DeFi industries, see subscription options below.

🤖🏦🧭 Our Ecosystem:

Generative Ventures | AI Research | Robot Money | Linkedin & Twitter | Sponsors

🚀 Lex is actively meeting teams building machine-native financial companies. If that’s you, reach out here.

🤖 AI & Robotics Industry Encyclopedia: In this 100+ page report, we collate all the meaningful companies across public quities, private equity, and digital assets related to the machine economy. 👉Learn more here

Long Take

Launching our SPAC

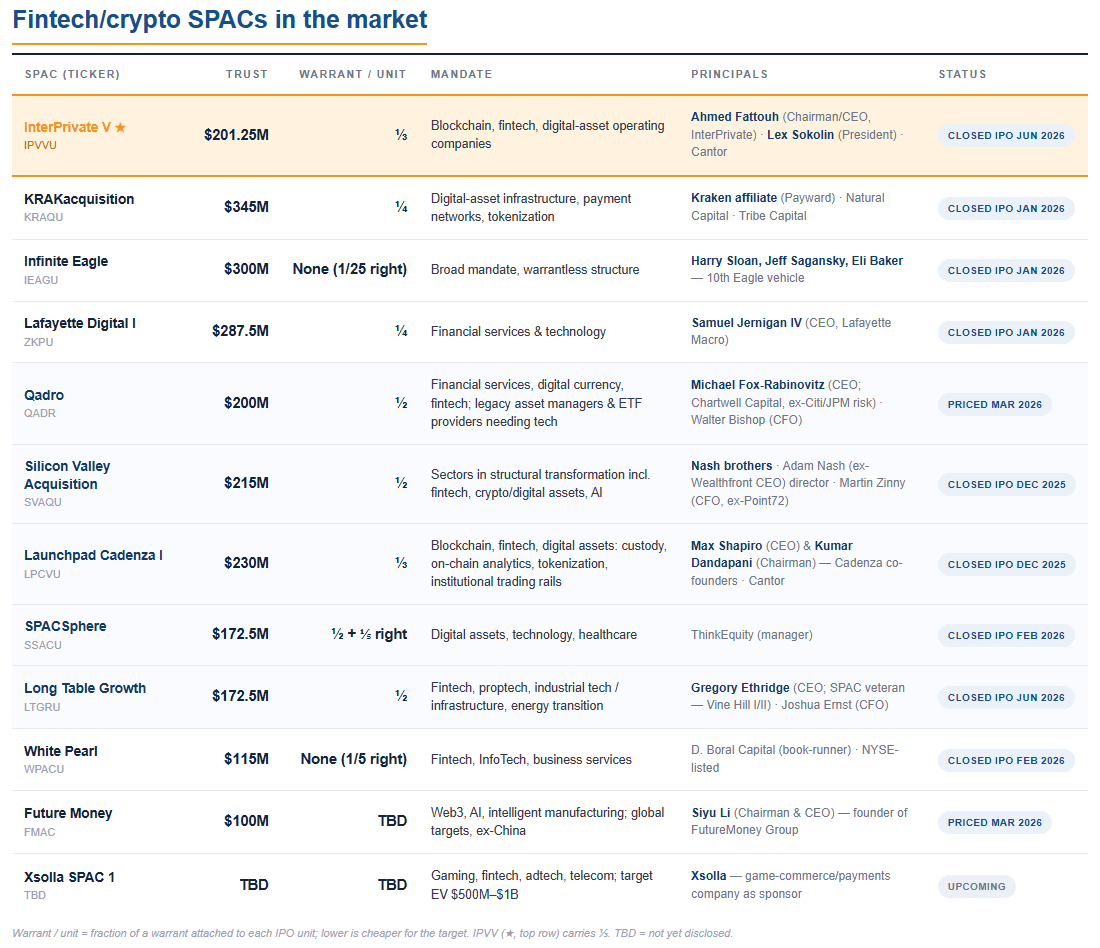

I am excited to share that, in partnership with InterPrivate and Ahmed Fattouh, we have launched a $201MM SPAC, now live at $IPVV.

I’m writing to explore in more detail my thinking on the SPAC market, why we launched a new vehicle, and the market dynamics.

At a high level, we are looking for unicorn companies in fintech, digital assets, AI, and the broader machine economy to bring to the public equity markets.

The last 5 years have been pretty wild.

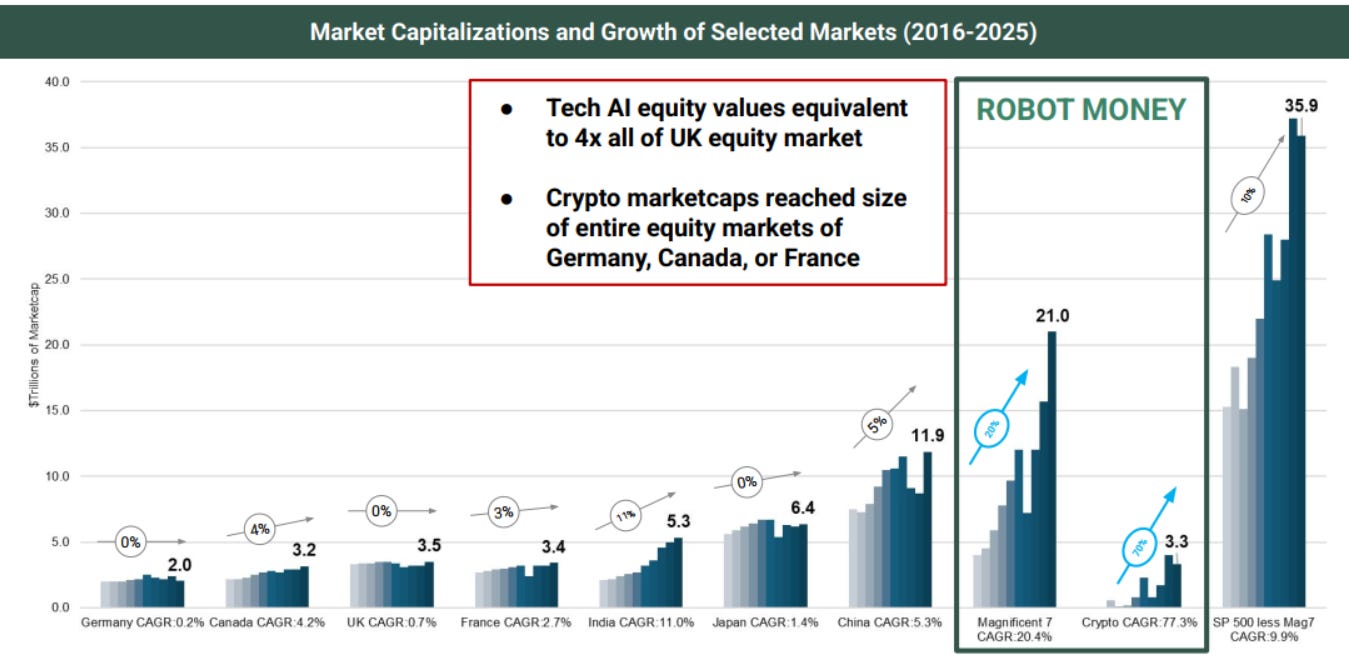

On the one hand, we have seen the blow-ups of multiple companies, banks, digital asset treasuries, and crypto assets. You had to have both vision and skill to survive, and a handful of companies (e.g., Hyperliquid, Polymarket) thrived on the volatility. On the other hand, an entire AI industry has been born, with the highest capital investment in technological infrastructure I have ever seen. This boom has already been expressed in energy and hardware prices, and several trillion of marketcap have been generated in just a handful of years.

Through this, I have seen founders build out strong ventures, sometimes scrambling through the fog but climbing out with successful businesses. They had done it through aggressive regulatory regimes, changing consumer expectations and behavior, and shifting global macro-economic relationships.

Fintech neobanks that have built $100MM+ revenues and profitability, using stablecoins or social media as leverage points against incumbents

New crypto infrastructure supporting billions in payment and trading volumes, connecting parts of the world others found hard to reach

Neoclouds, as well as energy and memory companies, scaling up to support the enormous AI build-out

AI-native applications that find incredible product-market-fit with coding, video, marketing, or other general employee tools

While some of these companies have gone public, been acquired, or merged into DATs, most still remain private. Everyone is waiting. SpaceX, Anthropic, and OpenAI are the big planes on the runway that must go public before anyone else has a chance for liquidity.

This means that investors will be holding mega-caps, both through retail participation and index investing, rather than buying companies in the $500MM to $5B range — a price that would allow more price discovery in the public, rather than private, markets.

The other effect of this is on venture capital. As founder of Generative Ventures, I’ve learned that DPI — the cash you return to investors — is the lifeblood of your LP relationships. If you don’t return DPI, then your investors will struggle to re-invest in your next vehicle. And the 2020+ vintage venture funds are struggling on DPI.

")

This means venture funds need to exit in order for the industry to keep raising money and investing in high-risk innovation. As a result, there’s a bifurcation between funds that have invested in the AI champions — increasingly only the mega funds — and vertical specialists who are not seeing liquidity. The result is widely overpriced seed rounds and consensus bets.

Given the existence of a whole bunch of high-quality companies (on fundamentals), the IPO window constraints, and the need for investors to exit, I think this is a moment when the SPAC structure adds a lot of value.

SPAC Sponsors and Market

The way a SPAC works is in roughly in these steps:

A sponsor team brings a vehicle to market through an IPO process with an investment bank. The vehicle has 2 years to find a deal, and retains a trust of some amount of capital (e.g., $200MM) that can be committed to the deal.

The team either (a) finds a target and agrees on a transaction with the company, or (b) is unable to find a deal within the timeline and returns money to investors

If there is a deal, trust investors may redeem (i.e., withdraw their money) if they do not like the deal, or for other reasons. The company and sponsor team usually raise a PIPE in addition to the trust capital to cover any gaps.

InterPrivate is a repeat SPAC sponsor, which means this is the 5th vehicle from the company. The platform’s edge is a co-sponsor network — independent sponsors, family offices, founders, and PE/VC firms — that widens the funnel and adds operating leverage and domain expertise, with the ability to support transactions with PIPE (private investment in public equity) capital from family-office LPs.

In the prior SPAC cycle, it had launched several successful searches, like Aeva — a 4D LiDAR-on-a-chip company founded by ex-Apple executives. Aeva closed a $1.8B merger in March 2021 and raised a $120MM PIPE, and a $200MM follow-on thereafter. InterPrivate also backed Microvast / Tuscan, a next-gen EV battery technology, which did a $3B merger in July 2021 and raised a $483M PIPE.

It had also run vehicles where the market timing didn’t work, and the capital was returned to investors.

Timing matters a lot.

The IPO window is open, until it is closed shut for years to come.

Market View

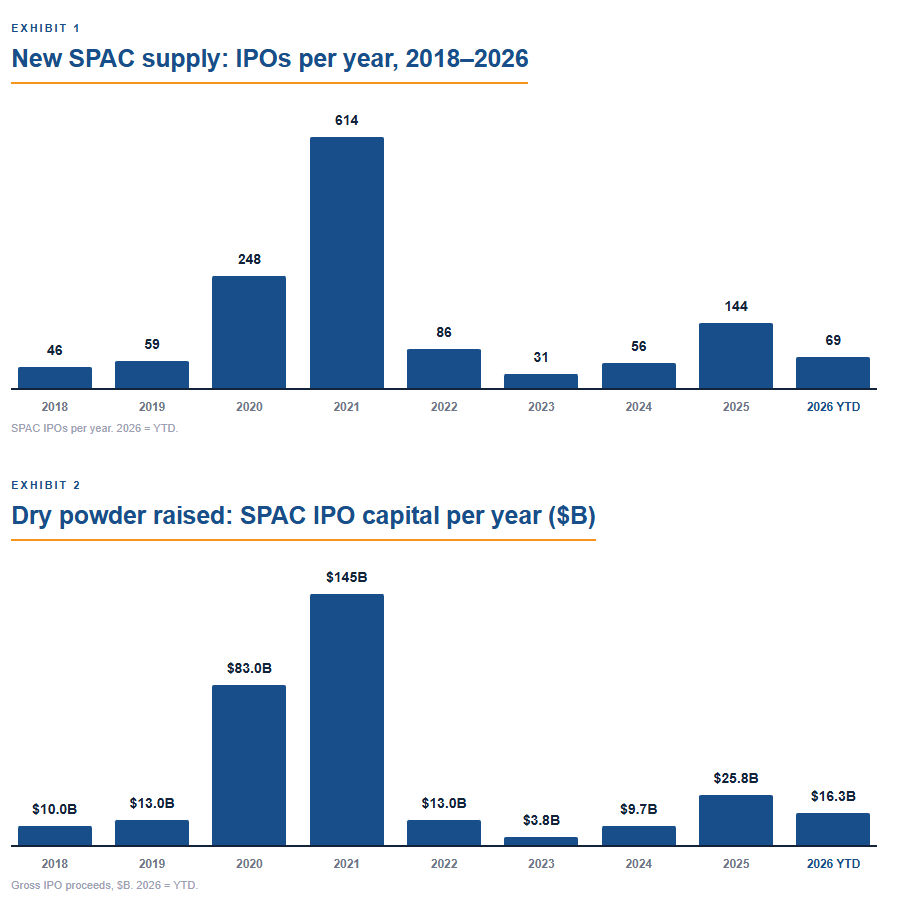

The last SPAC boom had come in 2020 and 2021, when nearly 800 vehicles were raised after the growth of digital adoption during COVID. Neobank and neobroker metrics were through the roof, as people stayed home and became chronically online.

Zoom stock soared!

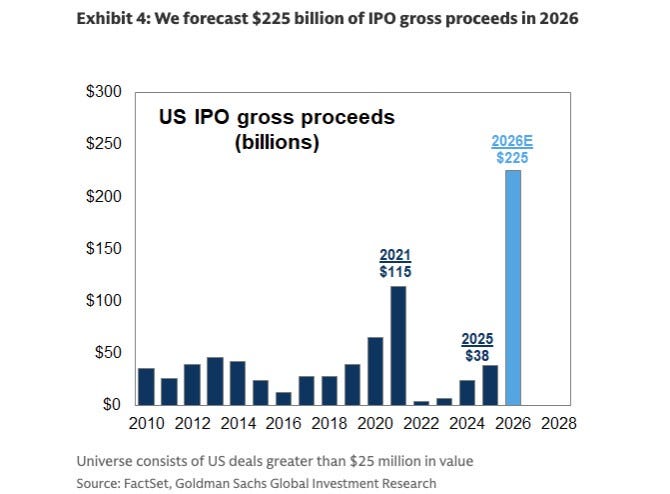

SPAC trust proceeds exceeded $200B in raised capital over those years. For context, that’s less than Goldman Sachs thinks we will IPO in 2026 alone in AI stocks.

However, many companies came to market that were not really ready to be public.

They used SPACs to share overly optimistic projects and bypassed the usual diligence of the going-public process. Many of them were venture capital-style bets, pre-traction and pre-revenue. When the digital shut-in culture of the pandemic years stopped, we saw significant fallout in companies that did not support their prices with fundamentals.

That creates a lesson for this time around — focus on operating excellence and documented growth. Overall capital raised into SPACs has been more limited — $25B in 2025 and $16B in 2026 so far.

There is about $55B of capital looking for deals across all sectors today. Within Fintech, however, we see around $2B in capital across 12 different vehicles.

Many of the vehicles are in the $100-300MM range, and Cantor is underwriting several. It’s a pleasant surprise to see Adam Nash, former Wealthfront CEO, in the mix as well, and we recognize Kraken as a savvy capital markets player that has been very active in the digital asset treasury market last year.

One other notable feature is the warrant size — the smaller the warrant, the cheaper the capital for the company going public.

Below are a few deals that have been announced as targets.

We don’t have full view of the economics on these, but recognize the names.

Securitize is a tokenization platform with a strong partnership with BlackRock. We have talked to the CEO in the past here. They have packaged several billion of RWA money market fund assets onchain together.

Abra is an early crypto wallet / neobank provider. While they were a material player in the <2021 regime, we have heard less about the company recently.

Animoca is a Web3 gaming company with a broad portfolio of assets, having leaned into the metaverse and onchain activity. Our interview with the CEO is here.

This gives a flavor of the company profiles that are now evaluating public markets — market caps in the $1-5B range, revenues likely between $50MM and $250MM, and a history of execution. Not every company is a straight exponential line up and to the right, like Anthropic, but it also makes for a healthier capital market to have a variety of exposures and risks in the market. The alternative right now is to be a buyer of a mega-tech late-stage trillion-dollar AI company.

Of course, SPACs are not for everyone. Many good companies take the straight path to IPO. Others can choose direct listings, token launches, SPVs, or other liquidity options.

SPACs *are* a good fit for companies that want to (1) be public, (2) have a strong counterparty with a clear view on the market, and (3) are dealing with more complex cap table and founder dynamics than usual.

If you think that your company fits the bill, or have an introduction to another potential target, give me a shout by replying to this email or sending a DM!

Excited to hear from you.

🚀 Postscript

Sponsor the Fintech Blueprint and reach over 200,000 professionals.

👉 Reach out here.Check out our AI newsletter, the Future Blueprint, 👉 here.

Read our Disclaimer here — this newsletter does not provide investment advice

SPACs are historically so sketchy, and yet I understand the intellelctual intrigue of finding yet another efficient means for issuers and investors to facilitate a capital exchange.

As an issuer, and also as a potential investor, with whom should I speak to ascertian if this is indeed worth time for me, counsel, and other fellow execs to pursue?