Blueprint: ConsenSys raises @ $7B; Japan's neobank Kyash gets $40MM+; $17B Anchor protocol on Avalanche

Blueprint: ConsenSys raises @ $7B; Japan's neobank Kyash gets $40MM+; $17B Anchor protocol on Avalanche

Gm Fintech Futurists — our agenda for today is below.

WEB3: Ethereum Software Company ConsenSys Doubles Valuation To $7 Billion In Four Months Amid Market Turbulence (link here)

NEOBANK: Block backs Japanese fintech startup Kyash in $41.2M round (link here)

DEFI: Avalanche Adopts Anchor Protocol (link here)

LONG TAKE: What Layer 1 protocols must learn from the Telecom crash (link here)

PODCAST: Embedding crypto assets into fintech footprints, with Zero Hash CEO Edward Woodford (link here)

To go deeper and support our analysis, check out the premium features below.

Visit our carefully curated Sponsors:

Don’t miss out on 30,000+ meetings with thousands of participants from leading Fintechs like Alloy, BlockFi, Cash App, Checkout.com, Feedzai, NIUM, Pipe, Socure, Stripe & Upstart, Banks like Bank of America, Barclays, Citibank, J.P. Morgan & USBank, Investors like Bain Capital Ventures, Commerce Ventures, General Atlantic, 175+ Credit Unions, Networks and many others! Virtual, March 22-24.

👉 Get your ticket now!

Short Takes

WEB3: ConsenSys Doubles Valuation To $7 Billion (link here)

Web3 tech company ConsenSys raised $450MM in Series D funding at a $7 billion valuation. Parafi Capital led the round, and were joined by new investors like SoftBank Vision Fund 2 and Microsoft. This round doubled the previous Series C valuation of $3.2B from four months ago. We think this valuation is (1) catching up to the operating performance of the company’s underlying assets, such as MetaMask, while (2) also retaining a premium on private, rather than public, crypto and fintech companies.

ConsenSys suggested it will convert a meaningful portion of the funds raised into ETH, thereby committing to one of the largest corporate and DAO treasury positions in the space to crypto-native assets. It then plans to stake that ETH to earn yield, leveraging its institutional Codefi Staking software for the purpose.

There’s currently about $30 billion, give or take, of staked Ethereum, which is generating 4-5% interest rates. It is locked into the proof of stake chain, but will be liquid after the merge. If similar interest rates can persist, this will make ETH a potentially viable candidate for treasuries in traditional industry as well, whereas BTC holdings rely entirely on capital gains for appreciation.

As it relates to the operating performance of the company, ConsenSys has transitioned from its early days as an investment and venture studio to a product core driven by MetaMask (leading non-custodial wallet) and Infura (developer enablement). Each is integrated into multiple blockchain networks and globally deployed. At the same time, competition from projects like Alchemy and Phantom wallet have increased the pressure to perform and the requirement for capital.

The news also brought attention to ConsenSys’ ongoing projects around a MetaMask token. Airdrops are currently getting a bad reputation, so we understand *why* the company is walking softly.

Interested in sponsoring?

We work with select companies to deliver brand awareness to our 100,000+ digital finance audience. See our prior partners here, and reach out here with interest.

NEOBANK: Block backs Japanese fintech startup Kyash in $41.2M round (link here)

Neobanks have benefitted from the move to digital during the pandemic, spurred by an increase in cashless payments and online support becoming default behaviours. However, Japan has been notoriously slow in going cashless, which has led to slower adoption of neobanks. Yet, Japan is the world’s third-largest economy globally and there is a large market ready to be won over — as you can see in the chart below.

To that end, let’s take a look at one of the leading neobanks in the industry. Tokyo-based Kyash raised $41MM in Series D funding for their mobile financial and banking application. The round included investments from Block, Japan Post Investment Corporation, Altos Ventures, and others. Overall, it brings Kyash’s total funding to $108MM since being founded in 2015.

Kyash is a mobile banking app offering remittances, ATM withdrawals and payments, with a few standout features. These include increased flexibility by providing the option of virtual and physical pre-paid debit cards, and the ability to make offline payments. It also holds 2 financial licenses: for prepaid debit cards, and fund transfers. The fintech is focused on the direct channel business, which suggests a need for a large marketing budget to be spent on customer acquisition. Once a company gets to this stage, it usually blitzscales into a leadership position — whether or not there’s profitability.

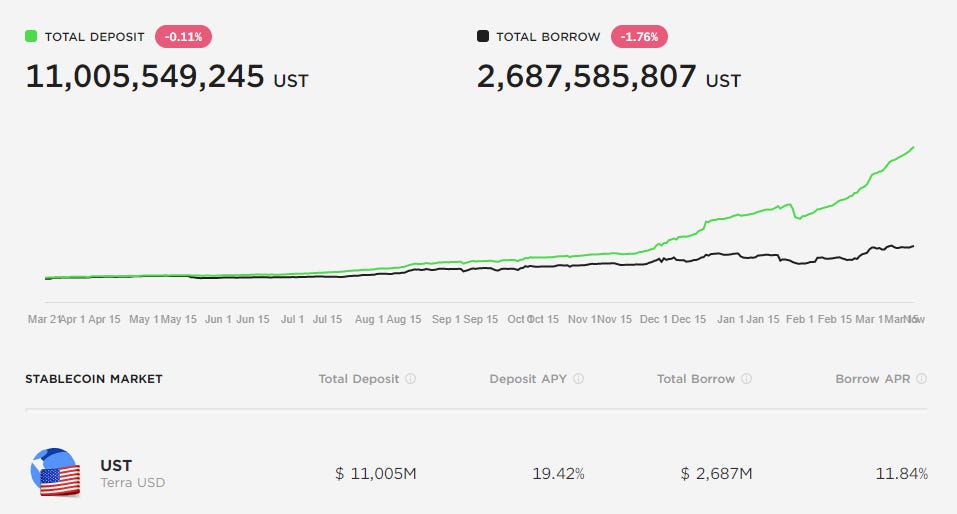

DEFI: Avalanche Adopts Anchor Protocol (link here)

Who wouldn’t want to make 20% a year on your USD deposits? Well, make that UST deposits.

xAnchor, the interchain extension of Anchor Protocol, has gone live on the first non-Terra blockchain with Avalanche. Anchor is a DeFi borrowing and lending protocol built on Terra that has gained popularity by enabling users to earn a “fixed” yield of almost 20% on their TerraUSD (UST) stablecoin deposits.

Anchor has a staggering $17B TVL. It has — so far — been able to sustain this fixed yield through over-collateralised borrowing. The deposited collateral is used to earn yield on other DeFi protocols, which is then used to pay out lenders.

This functionality launched in the Avalanche ecosystem, powered by the Wormhole cross-chain bridge, which helps users to bridge UST on the Avalanche blockchain to xAnchor (CrossAnchor). The launch was catalyzed by the Avalanche Rush program, amongst other initiatives, which have been incentivizing developers to utilize UST over other stablecoins. Avalanche’s $14B in value locked is likely to see increased growth from Anchor, as new users rush to higher interest rates in new places. Crypto money printer goes BRRR.

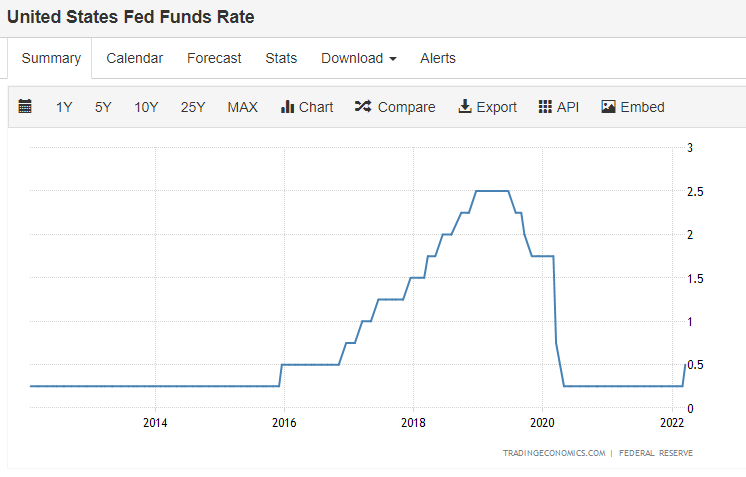

Look, there are no perpetual money machines, and it’s reasonable to question the sustainability of the protocol. But there are also leverage and user acquisition machines, some of which might scale into the trillions. Once at the scale, they will turn down the interest rates to, oh we don’t know, something like this?

Whether you like it or not, money is a meta-game. At least now, it is transparent for everyone else to see.

Rest of the Best

Here are the rest of the updates hitting our radar. Note that DeFi and digital investing now have their own dedicated weekly emails, on Tuesday and Thursday respectively.

PAYMENTS: Ramp Secures $750 Million in Funding to Help Businesses Automate Their Financial Operations

BANKING: ClearBank raises $229 million marking expansion push

NEOBANK: Lunar raises €70 million

PAYTECH: Multiplier raises $60 million

PAYTECH: FinTech NextPay Plans Bill Payments, Other MSME Services

INSURTECH: Policygenius raises $125 million

INSTITUTIONAL: Egypt state banks setting up $85 million fintech innovation fund

What Layer 1 protocols must learn from the Telecom crash (link here)

We analyze the market dynamics around Layer 1 and Layer 2 alternative networks, and get to the root of how growth is being incentivized.

The $290MM Avalanche ecosystem fund for the “Multiverse” is an example of such a strategy. We discuss the manufacturing of decentralized computation, its relationship to builders and users, and the price dynamics that result. Finally, we close with a comparison to traditional marketing programs, corporate venture capital, and the collapse of the Telecom industry after the Internet bubble.

Podcast Conversation: Embedding crypto assets into fintech footprints, with Zero Hash CEO Edward Woodford (link here)

In this conversation, we chat with Edward Woodford, Co-Founder and CEO of Zero Hash. Zero Hash’s mission is to empower innovators by delivering access to the financial system 2.0. Zero Hash provides the complete turnkey solution to allow platforms to launch digital assets and own the client experience, without any regulatory overhead and a light technical lift. Zero Hash’s clients include Neo-banks, broker dealers and payment groups.

More specifically, we touch on CFTC regulated marketplaces for Hemp, launching a digital asset trading business, Embedded finance and API-driven businesses, the US regulatory patchwork for traditional financial service companies vs new banking-as-a-service companies, third-part crypto wallet providers and so so much more!

More? More!

If you want to go deeper in Fintech & DeFi, upgrade to a premium Blueprint subscription below. Our value prop is simple: experienced judgment, accurate vision. If you knew the shape of the tomorrow, what would you do today?