Blueprint: First Republic collapses into JPM after $100B outflow; Kakao Pay buying US brokerage Siebert; NFT-backed lending by Blur

Blueprint: First Republic collapses into JPM after $100B outflow; Kakao Pay buying US brokerage Siebert; NFT-backed lending by Blur

Who's next? You decide.

Hi Fintech Futurists —

You’re the best, today’s agenda below.

BANKING: How Jamie Dimon swooped on the remains of First Republic (link here)

NFT: You Can Now Use Your JPEGs to Borrow Ethereum on NFT Marketplace Blur (link here)

PAYTECH: Korean fintech Kakao Pay to acquire majority stake in US brokerage firm Siebert (link here)

LONG TAKE: Combining AI agents, like AutoGPT, with Web3 chains will create self-driving money (link here)

PODCAST CONVERSATION: Combining AI agents, like AutoGPT, with Web3 chains will create self-driving money (link here)

To support this writing and access our full archive of newsletters, analyses, and guides to building in the Fintech & DeFi industries, subscribe below.

In Partnership

Join us at Fintech Nexus USA — we will be there. The event brings together top minds in fintech to cover topics like digital banking, fraud, blockchain, embedded finance, fintech investing, and more. 5,000 attendees will engage in 20,000+ double opt-in meetings this May 10-11 in NYC. It’s the can’t-miss event of the year!

👉Use promo code “FinBlue” and get 15% off today

Short Takes

BANKING: How Jamie Dimon swooped on the remains of First Republic (link here)

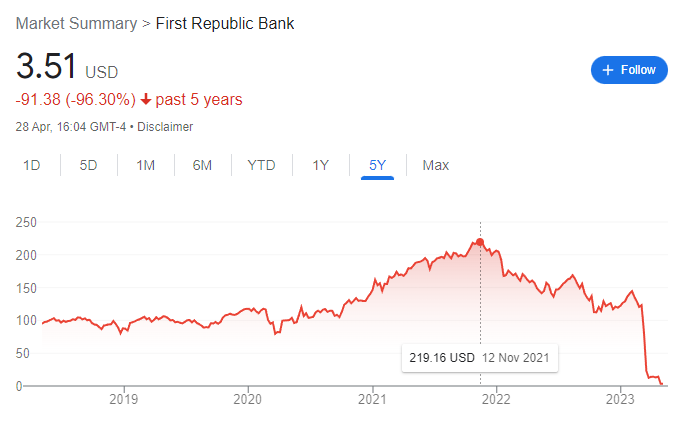

The banking industry saw wild pressure in March, as Silicon Valley Bank, Signature Bank and even Credit Suisse collapsed. The first domino to fall was Silvergate after its voluntary liquidation. But the dominoes keep falling — JP Morgan is now buying First Republic, after initially playing the role of advisor, then depositor, and finally buyer.

JPMC has taken over all deposits, while securing a loss-sharing agreement with federal regulators to minimise the impact of any problematic loans held by First Republic. This marks the third major US bank failure in the past two months, and it is the largest bank to be impacted since Washington Mutual in 2008.

The transaction will see First Republic shareholders left with nothing. On Monday, its share price dropped 43% before trading was halted. To secure the deposits, which JPM assumed, the big bank will be backing $25B of the $30B initially. A further $11B will be paid to US Federal Deposit Insurance Corp (FDIC) as a part of the deal. FDIC on the other hand will pay out $13B from its Deposit Insurance Fund.

JPMC already held over 10% of the US total bank deposits. Analysts estimate that JPMC’s market share would notch up another 3% after the deal.

All this is a reminder that monopoly power allows the very biggest banks, who have an intrinsic too-big-to-fail backstop, to capitalize on the failures of regional or niche banks for significant gain. UBS, for instance, will break banking industry record profits in Q2 with the acquisition of Credit Suisse (to be fair not a regional bank), receiving a projected $57B gain on the $3B they bought Credit Suisse for. But if you look at the deposit base in the US, there’s increasing concentration to the very top.

Should money be a utility like the post office? Is it already?

👑Related Coverage👑

NFT: You Can Now Use Your JPEGs to Borrow Ethereum on NFT Marketplace Blur (link here)

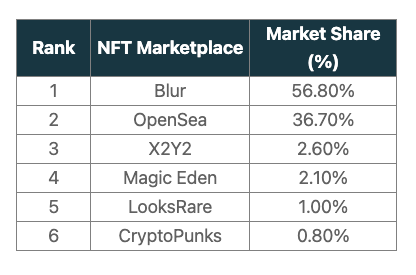

Blur has had an incredible rise to the top of the NFT market over the past 6 months. Spurred by its token launch, airdrop, and user experience, it is now the leading NFT marketplace with 57% market share, knocking OpenSea down to 37% and leaving very little for third place X2Y2 (2.6%).

Despite the market share, Blur has less traders than OpenSea (3k vs 27k), although those traders are have much more daily volume ($23MM today for Blur vs $8MM for OpenSea). This has arguably been part of Blur’s success — attracting advanced NFT traders that control the volume through product features that cater to their trading behaviors. After all, marketplaces make their money from a basis point fee on trades. Some of the volume could be wash-trading, but unlikely all of it.

The project has just introduced Blend (i.e., Blur Lend) — a peer-to-peer perpetual lending protocol that allows users to use their NFTs to take out loans. The product is a fit for their target market, advanced NFT traders with significant NFT holdings. Blend allows them to leverage these assets for liquidity or continued trading, which in turns sustains activity on the platform. There are currently no fees for borrowers or lenders currently, but the DAO can vote to change this paramater after 180 days.

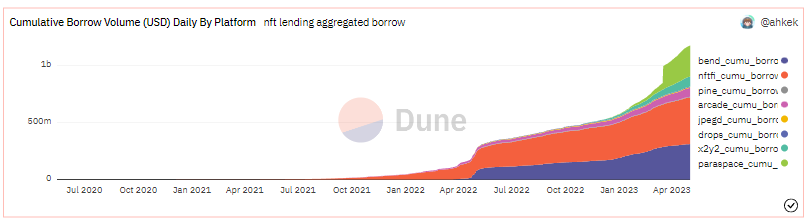

The market opportunity for Blend is there — the NFT lending market is now worth over $1B in collateral. This is largely split between NFTfi, with $406MM in loans, and BendDAO with $308MM. The lending solution deepens its relationship with users, and diversifies the marketplace brand from brokerage/exchange into that of a p2p lending protocol. Given that many think Blur was being opportunistically farmed, having a product that locks in loyalty could be a counter-balance.

All that said, we know that leverage isn’t the long term solution. Rather, it is a financial engineering of an exit from a currently illiquid asset. The lender bets on the crypto market recovering, the borrower is short NFTs and long fungible tokens.

Interested in Sponsorship?

To support the Fintech Blueprint and reach our 170,000+ Substack and LinkedIn audience of builders and investors, learn more below or contact us here.

PAYTECH: Korean fintech Kakao Pay to acquire majority stake in US brokerage firm Siebert (link here)

Kakao Pay is expanding into the US after acquiring a 19.9% stake in Siebert, a NYC brokerage firm, for $17MM. The move is the first in Kakao’s bid to acquire a majority stake (51%) in Siebert following shareholder and regulatory approval.

Kakao Pay is the payments service of Kakao, a leading South Korean messaging and internet firm. Currently, the fintech provides online and offline payments, insurance, credit rating and loan services to 40 million users across South Korea, Japan, Macao, Singapore, China and France. It is one of the successful superapp stories rooted in financial product.

Kakao Pay launched in 2014 and has since risen to become a the leading mobile payment firm within South Korea, competing off comparnies like Samsung Pay and Naver Pay. This investment, Kakao Pay’s first outside of its home market, has two key outcomes. First, it powers US expansion — a market dominated by Apple Pay with 92% of market share, followed by Samsung Pay with 5%, and Google Pay with 3% market share. Given Kakao Pay’s dominance over Samsung Pay in their home geography, perhaps there is a similar opportunity in the US. Second, the acquisition bolsters its securities unit, Kakao Securities, for its offering in Southeast Asia.

The near-term strategy is to combine the Kakao Securities existing mobile trading system with Siebert’s brokerage infrastructure to build an overseas stock trading solution. It’s not obvious whether this is a brokerage play for US customers, or to bring US stocks more cheaply into Asian geographies, or to bring US stock trading infrastructure to fintechs in Asian geographies. We are, however, always interested in the melding together of different parts of financial services into a single experience — in this example, payments and capital markets.

Long Take: Combining AI agents, like AutoGPT, with Web3 chains will create self-driving money (link here)

Prediction is a hard game, but we can learn by articulating our hypotheses and figuring out the real constraints.

We cover how large language models, i.e., LLMs, have evolved recently and their assembly into artificial intelligence agents that can start to do human tasks independently. Robotic process automation is an important industry theme, and LLMs add intelligence into those workflows. However, we dive deeper to think about how self-driving financial agents could be generated on blockchains, and why digital ownership of those software robots is an important destination.

Podcast Conversation: Data aggregation for small businesses across banking, accounting, and commerce, with Codat CTO David Hoare (link here)

In this conversation, we chat with David Hoare, the CTO and co-founder of Codat - a universal API platform that connects small businesses to banks and other financial platforms.

Dave has proven to be an expert in the fields of digitally native platform businesses through his background. Having previously worked as a software engineer at Kriya (formerly MarketFinance) from 2015 to 2017. Kriya was the UK’s first online-only invoice finance provider. It’s grown to become one of the largest invoice finance providers in Europe, having now funded billions of pounds worth of invoices. Additionally, Dave worked as a software engineer at digital publishing company Archant from 2012 to 2014. Dave holds a Bachelor of Arts in Computer Science from the University of Cambridge.

Rest of the Best

Here are the rest of the updates hitting radar.

PAYTECH - Belvo acquires Brazilian company Skilopay to grow its payments offering

PAYTECH - European Payments Initiative to acquire iDeal and Payconiq

CREDIT - Vista Seeks Record $6 Billion Private Credit Deal for Finastra

BANKING - Deutsche Bank invests in Britain with $511 million Numis deal

INVESTING - Super.com targets its $85M equity, debt raise into new savings super app

INFRASTRUCTURE - Financial market infrastructure firm Axoni lands $20m

Shape your Future

Wondering what’s shaping the future of Fintech and DeFi? At the Fintech Blueprint, we go down the rabbit hole in the DeFi and Fintech industries to help you make better investment decisions, innovate, and compete in the industry.

Read our Disclaimer here — this newsletter does not provide investment advice and represents solely the views and opinions of FINTECH BLUEPRINT LTD.

Want to discuss? Stop by our Discord and reach out here with questions.

Later this week, we will share our Short Takes on the latest Web3 and Digital Investing news, reviewing several companies. If you’d like us to look at any specific item, feel free to share your thoughts in the comments below. We will provide our best analysis in response to your requests.