Financial Analysis: Can Affirm beat Klarna in the BNPL market?

A Hail Mary with the Affirm Card and SMB financing

Gm Fintech Architects —

Today we are diving into the following topics:

Summary: Earlier this year we wrote on the ~80% drawdown in valuations of BNPL providers. At the time, we highlighted an uncertain macro environment and increased interest rates as key threats to the sector. Many of the same challenges persist today, yet both Affirm and Klarna exceeded investor expectations in the latest quarter after posting a narrowing loss and growth in revenues and customer spending. Affirm’s share price gained 14% on the news, partially recovering the decline over the past year. This week we take a peek under the hood of the Affirm model, analyzing its performance under higher interest rates and identifying why it trails other BNPL providers. We touch on Affirm’s renewed strategy with the Affirm Card and expansion to the SMB segment, and discuss whether it can win in an increasingly crowded US market.

Topics: Lending, BNPL, Affirm, Klarna, Afterpay, Apple, Banking, Ecommerce

Special thanks to Michiel for this fantastic analysis

If you got value from this article, let us know your thoughts! And to recommend new topics and companies for coverage, leave a note below.

Long Take

Building Affirm

Affirm was founded in 2012 by ex-Paypal founder Max Levchin with the initial aim of building a better credit score. Levchin’s personal experience racking up credit card debt to fund his business in college served as motivation to create a better estimate of an individual’s creditworthiness than the FICO score. He quickly realized that the broader credit card system, like other financial products at the time, suffered from opaque pricing models.

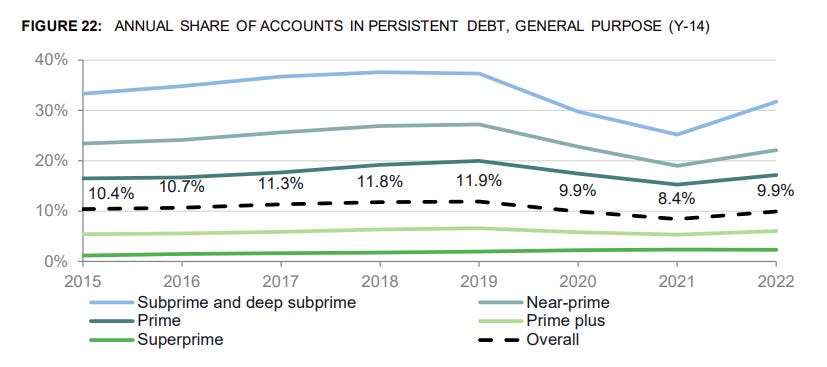

Costs hidden in compounding interest and late fees result in many customers (especially at the subprime levels) ending in “persistent debt” — meaning they owe 50% above the value of the items they originally financed. The share of credit card accounts in persistent debt in the US reached 12% before the pandemic, compared to 10% in 2015. Those with subprime and deep subprime scores comprised the majority of those trapped in persistent debt, arguably in part due to the rates at which credit products are offered to those segments.

Levchin’s solution was to partner with merchants to offer more transparent financing to customers at checkout, with zero late fees and a clear end-date to the payment plan. Like other BNPL providers, the company’s underwriting model achieved a higher acceptance rate by combining traditional credit checks with data from merchant partners and customer spending behavior. In Affirm’s case, the increase in eligible customers it could underwrite offset the lack of late fees.

Affirm originates the loans through third parties, namely Cross River Bank and Celtic Bank. The process consists of Affirm performing the underwriting, the partner bank distributing the loan to the consumer, and Affirm subsequently repurchasing the loan as an “investment”. Affirm keeps some of the loans on its balance sheet, but sells others to retain capital efficiency.

Today, Affirm offers two core loan products: (1) Pay-in-4, which splits the transaction in four bi-weekly 0% APR payments, and (2) Core, which are interest-bearing monthly installment loans. The company serves 17MM active customers across 255K merchants in the US and Canada with annual gross merchandise volume (GMV) of $20B last year.

This BNPL value proposition has gained traction outside of the US as well, with Klarna leading in Europe and Afterpay (acquired by Square) in Australia. In 2022, BNPL accounted for 5% of global e-commerce payments, up from just 1% in 2015. Credit cards meanwhile accounted for 20%, but are expected to fall to 16% by 2026.

Affirm lags competitors in key metrics

Despite sector growth, Affirm has struggled to stay ahead of competitors in most key metrics. In 2022, the firm trailed both Klarna and PayPal in merchants, customers, and GMV. One reason is the company’s focus on the US and Canada markets, where the uptake of BNPL has historically been slower. In Germany, one of Klarna’s largest markets, BNPL made up over 20% of total e-commerce volumes vs. 5% in the US.

Another reason is increased competition from Big Tech and banks. Since Affirm’s launch, the number of BNPL providers has grown to over 200+, with products from Paypal, Apple and incumbents like Citibank and Chase. These providers scale much faster because they have an established footprint in digital wallets and credit cards, which still represent 65% of US online payments. Paypal’s Pay-in-4 product processed $20B in 2022, up 140% YoY, compared to Affirm’s 30% YoY growth. Meanwhile, Chase reported that loans from its BNPL product scaled 3x faster than competitors last year during its investor day in May.

Affirm Financials

These challenges, combined with macro headwinds of the past year, have left a dent in Affirm’s financials. In its fiscal 2023 year-end this June, Affirm reported revenues of $1.6B, +17% YoY, but a growing loss of nearly $1B, up from $0.7B the previous year. Affirm attributes this partly to a larger mix of interest-bearing loans, which charge lower merchant fees. But it is also a result of rising funding costs, which are part of the $580MM in transaction costs recorded last year, up 34% YoY.