Long Take: Can Bunq, the $1.9B profitable European neobank, crack US consumer banking?

A bold ambition to win in a market where Goldman Sachs is retreating

Gm Fintech Architects —

Today we are diving into the following topics:

Summary: Following its fresh $111M fundraise, Dutch neobank bunq recently announced plans to expand into the US and UK markets. We benchmark the bank’s strategy against key EU competitors and challenge bunq’s stable valuation of $1.9B during the driest quarter of fintech funding since 2017. In addition, we discuss how bunq plans to extract value from a market where Goldman Sachs has recently begun to retreat consumer banking.

Topics: Neobanks, Funding, Valuations Bunq, Revolut, Goldman Sachs, Monzo, Wise, Starling

Special thanks to Michiel for this fantastic analysis

If you got value from this article, let us know your thoughts! And to recommend new topics and companies for coverage, leave a note below.

Long Take

The bank of “The Free”

Like many other neobanks, bunq launched in the wake of the financial crisis when consumers felt increasingly dissatisfied with the lack of transparency and online experiences offered by traditional banks. The Amsterdam-based company was granted a European banking license in 2014 and found its niche in the frequent traveller and digital nomad demographic, marketing itself as the bank of “The Free”.

Up until 2022, bunq made the majority of its income from subscription fees on its tiered banking products. These range from (1) a free savings account, to (2) a current account, (3) FX transfers and budgeting, and (4) insurance and CO2 offsets. Its mission of radical transparency on fees and charges reminds us of Wise, which indeed powers bunq’s FX transfers.

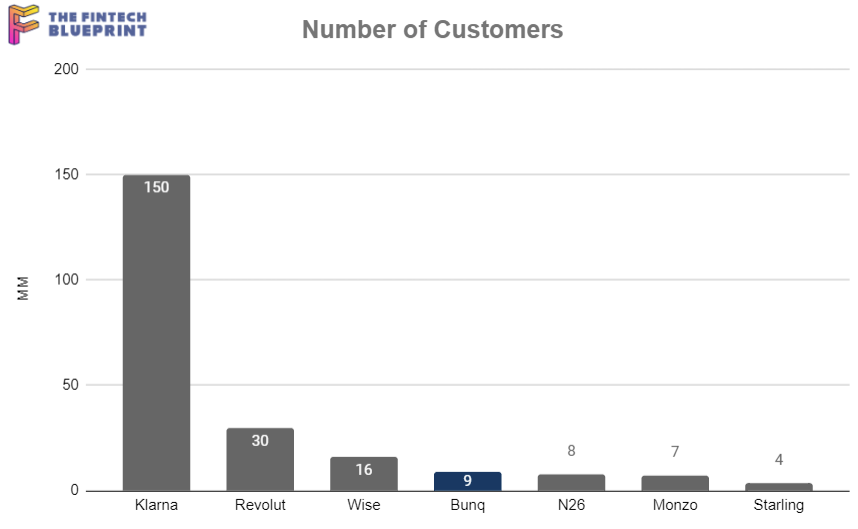

The bank reported $78MM in revenue on the back of heightened interest income in 2022 and turned its first profit in the fourth quarter. Last month, bunq reported a user base of 9 million customers across its EU markets with a combined $4.7B in deposits. This places it as the second largest pure-play neobank by users in Europe — excluding Klarna and Wise which are pure-play lending and payments companies, respectively.

Bunq’s founder, who still retains 90% of the business, personally bankrolled the initial 9 years of the firm’s operation. In July 2021, the firm raised its first external round of $228MM at a $1.9B valuation; or a whopping 128x FY20 revenue. This was significantly above both the 13x average neobank multiple at the time and the broader 25x average multiple for high-growth fintechs. But then again, Revolut raised funding that same year at 180x FY20 revenue.

Bunq’s most recent $111M raise is from existing investors, including its founder, which has likely helped it retain a flat valuation; based on current sales figures, the multiple is a more conservative 24x FY22 revenues. After all, it has had two full financial years to grow since its last round. That’s still high considering the average neobank multiple dropped to 4.6x as fintech funding hit a 6-year low in the second quarter of the year.

So what are investors betting on with bunq? We believe it is a mix of aggressive geographic expansion and revenue growth through M&A.

An M&A growth strategy

In contrast to competitors, bunq’s growth strategy largely consists of M&A for the acquisition of both users and assets. A majority 5.4 million customers joined the bank in 2022 via the acquisition of Tricount, a Belgian group expense management platform (think Splitwise). Similarly, bunq entered the Irish market following the acquisition of business lender Capitalflow, which now makes up the vast majority of its loan book. This strategy has helped keep the bank’s customer acquisition cost below those of competitors.

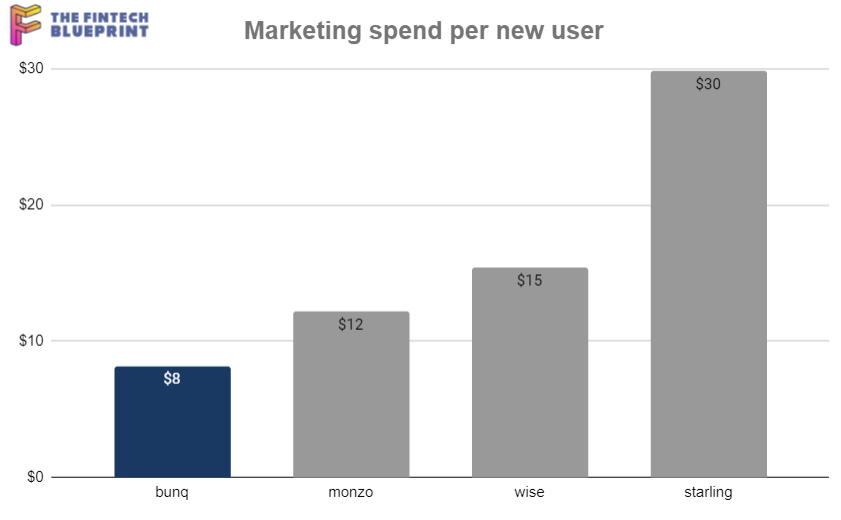

Analyzing marketing spend per new user across European neobanks shows that bunq spent roughly $8 for each new user sign-up in 2022. Wise and Monzo spent between $12-$15 per user in the same period, and Starling spent a larger $30, though for a larger average customer.

Bunq was also early in raising interest rates on its savings account, which resulted in strong deposit growth in 2023. Customers in its domestic Dutch market are offered a 1.6% APY, significantly above the 0.5% offered by the incumbent banks. Last month, the bank reported an increase in customer deposits to $4.7B, up 2.5x since the start of the year. This places bunq’s average deposits per customer comfortably above those of Revolut at $527, but still behind those of other European neobanks.