Long Take: Comparing MetaMask's Snappy Transition to a Developer Platform with Apple, Ant Financial, and ChatGPT

Can wallets be market venues or developer ecosystems?

Gm Fintech Architects —

Today we are diving into the following topics:

Summary: MetaMask, the Web3 wallet developed by Consensys, has introduced a feature called "Snaps" which enables third-party developers to create extensions enhancing the wallet's functionalities. The extensions can be categorized into three groups: connecting to blockchains that were previously unsupported by MetaMask, enhancing security by advising users on the safety of transactions, and improving the wallet's usability by incorporating messaging and communication features. Contrary to traditional applications where multiple financial accounts are tied to a single identity, the Web3 space utilizes financial identity to link various media and information channels, transitioning the wallet into a platform that is more secure, interconnected, and social. We highlights the issues around platform and network models, resembling the open architecture that has powered the success of platforms like Apple.

Topics: MetaMask, Apple, TD Ameritrade, Starling Bank, ChatGPT, Google, network effects, big tech, Web3, crypto wallets

If you got value from this article, let us know your thoughts! And to recommend new topics and companies for coverage, leave a note below.

Letter from Our Readers

Before we hop into the main topics today, we want to recognize a fantastic response we got to a recent podcast with Caitlin Long about the banking system.

Tom Abraham of Shadwell Advisory wrote a counterpoint to some of the discussion we had in this session. In the spirit of learning, we include it verbatim in the comments. You can see it, split into two sections, here — Part 1 & Part 2. An excerpt:

Banking as a scalable business, e.g. absorbing costs of technology and regulation, has been impeded by these legacies. State chartered banks are an unfortunate artifact of a bygone era that should be abrogated. If we want more services from banks, real-time settlement, APIs to payroll and accounting systems, scale benefits and flexibility, a national banking market is likely to be the most efficacious …

The irony is that most of the customers are from other states and countries shopping for lenient regulatory regimes not fancy technology nor faster transaction payments. Local jobs are created but the scope of business is essentially national. These state charters are more likely to create problems than solve problems.

Long Take

Snappy Snaps

MetaMask, the leading non-custodial Web3 wallet from Consensys, has launched an extensions system called Snaps. It allows third party developers to create extensions of MetaMask functionality, and implement it into the wallet through user choice.

The extensions fit roughly into three categories.

First, connections to blockchains that have historically been outside the scope of MetaMask. Early Consensys largely focused on Ethereum, as did the wallet. Now, it supports EVM chains — those Ethereum Virtual Machine compatible blockchains that can run certain types of computation. However, with Snaps, MetaMask can be used for Bitcoin, Solana, and the Move-based protocols from Facebook’s Diem project.

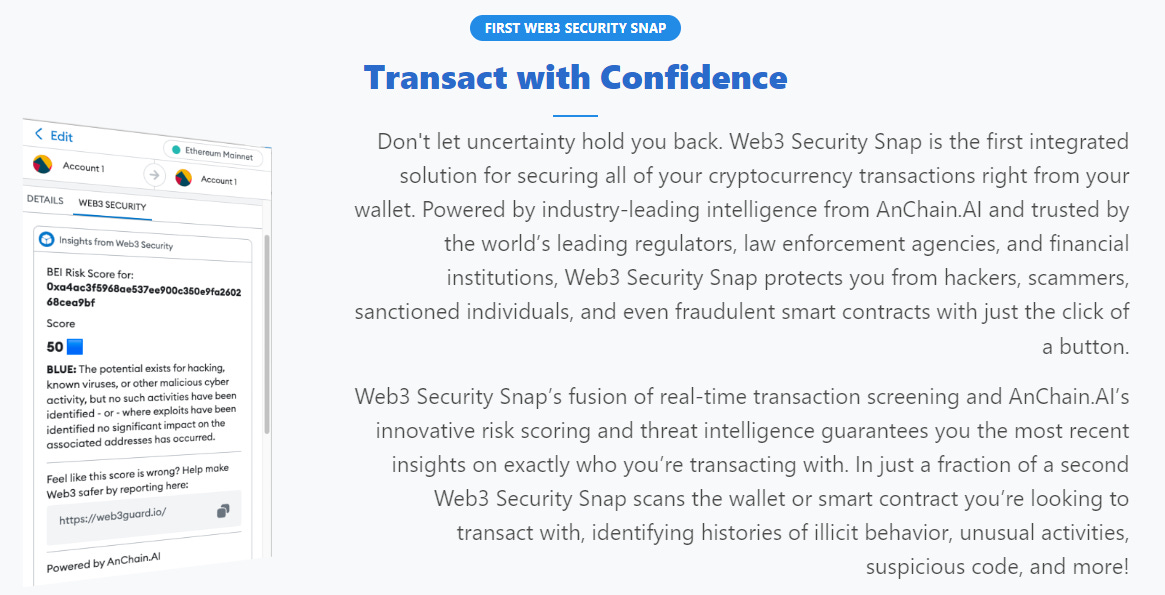

Second, there are a number of security-focused application. When performing a transaction from the wallet, websites will ask you for access to your assets, and to approve various transactions. Many of these will look alien to the average user. These extensions do safety checks and try to advise users about whether the transactions they will perform are wise. Some may simulate transactions using underlying blockchain data and calculate the expected results on your funds.

Companies that do this independent of wallets are features that should eventually be embedded in the wallet. We can see that here.

Finally, there are a number of extensions that focus on extending the usability of the wallet. A few are trying to introduce messaging and communications into the wallet flow. We know that payments and communication are closely linked, whether in an enterprise SWIFT setting or a Whatsapp text messaging setting.

Here’s an example called WalletChat, where your financial identity is also an avatar for communication.

Compare it to the Apple experience.

With Apple Cash | PCMag")

The interesting difference here is that traditional applications build an identity into which you can tie in multiple financial accounts. In Web3, you use your financial identity to connect in multiple media and information streams.

Looking at these initial extensions, it is notable that much of the DeFi and NFT functionality remains embedded in the core of the wallet. There are some exceptions, like Unipass, which enhances the stablecoin-based payment experience by making it simpler. But generally, the wallet can already move money, analyze a portfolio, stake assets, bridge them between chains, swap tokens, and process payments into and out of onchain assets.

The extensions so far are extending the wallet into something that is more secure, more connected, and more social. That’s not the usual direction for a trading app or a neobank, which would try to create a marketplace of various financial products. Rather, it’s a direction for a venue with many users and uses, defended by network effects. Unlike finance, which is an abstraction from the real world, crypto is the actual digital world in your pocket — a concept we’ve discussed below.

Network Effects and Nesting Dolls

The wallet has two form factors. The first is as a plug-in into a browser, like Chrome or Firefox. The second is as a mobile app, downloadable from the app stores of Apple or Google. Both are non-custodial and allow you to sign transactions that permission decentralized applications to interact with your assets and identity.

We say this to contextualize Snaps. The particularly interesting thing about it is the nested nature of ecosystems, platforms, market venues, and addressable markets. There are some tricky insights to parse, so let’s try to pull on the thread.

Let’s say there are 5 billion Internet browser users. Something like 65% of the use Chrome.