Long Take: Consolidation logic for fintechs and SPACs, starting with Acorns and GoHenry

Gm Fintech Architects —

Today we are diving into the Acorns acquisition of GoHenry, and the rationales for consolidation in the neobanking and micro-investing industry.

If you got value from this article, let us know your thoughts! And to recommend new topics and companies for coverage, leave a note below.

Long Take

Consolidation

There is a simple dynamic that is playing out in the public and private fintech markets. Many companies have to go out of business.

Nobody wants to fail. Investor capital has been put at risk, through various stages of maturity. Seed investors bet on the team and vision. Mid stage venture investors bet on user acquisition and charts of exponential engagement growth. Public investors bet on SPAC vehicles and the Amazonian story of “profit later”. Late stage public investors bet on technology and productivity growth.

When you shrink the pie by making money more expensive, capital leaves risky assets. Companies that were fine to be profitable later are, all of a sudden, on a life line lasting 6 months or less. To survive to the next milestone, they need more capital from investors, but investors don’t want to give it to them. Or, they will give it to them at a 95% valuation haircut, which wipes out all founders and senior management, who quit for jobs with a better paycheck.

We get no pleasure from the below chart, other than maybe wagging our fingers at SoftBank and Tiger for blitz-scaling fintech valuations past the point of any sense:

A while back we suggested that a reasonable private equity roll-up strategy just may be to buy up all of the SPAC / IPO discounted fintechs and consolidate them. While your revenue base is likely too small, and the egos of the entrepreneurs too large, the install base of users is just right.

If you want to review the eligible candidates, here are the key pieces of writing we did on the topic:

This strategy is now probably 70% less expensive than when we proposed it last.

Why do companies need to consolidate? The public narrative will state things like growth, improved products, stronger teams. Of course the entrepreneurs have to stress the positive side of the equation — getting more revenue out of customers. But the other side of the “synergy” coin is to cut costs.

Let’s say you have 2 neobanks, each with 1 million users, of which 100,000 pay $10 per year. In the abstract, you could consolidate these two footprints into a single brand, integrate the products to use the same technology, and remove 40% of the combined team to save costs. Why do you need to do that last part? Because there is limited runway and the capital markets are not affording you either an IPO nor operating capital at a valuation you like.

It sucks. But also, maybe mark-to-market.

Micro-investing Consolidation

In related news, Acorns, the American micro-investing company that rounds up your change into fractional portfolios, is acquiring GoHenry, the European money account for kids. We like them both.

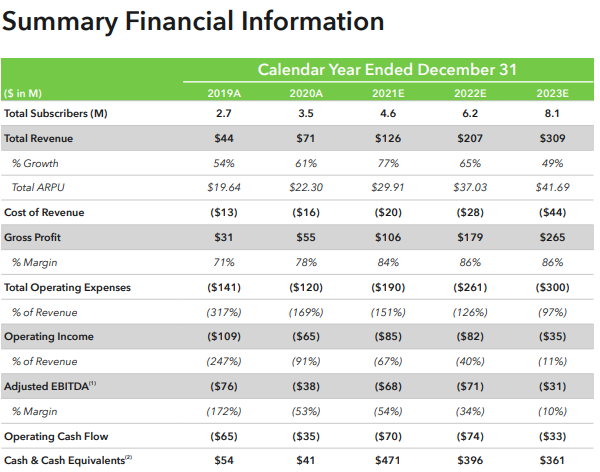

Acorns puts up impressive numbers — $2B private valuation last year, 10 million “all time customers”, who have invested $15 billion. The product has expanded from micro-investing to retirement, college savings, and banking services. It is difficult to know what those words mean, so we’ll refer to the 2021 SPAC deck, which showed a number of key metrics and projections.

Let’s assume that the current subscribers in Acorns is about 5 million, rather than its earlier more optimistic Covid-era projections. This would suggest an ARR of $150MM-200MM or so, and a burn of about $80MM. Having raised $300MM last year, the company has four more years in the pocket.

The real question — in all retail neobank and roboadvisor situations — is about charts like the above. Can the bridge to more revenue per user be built? We know that in 2023 consumer sub-prime underwriting, crypto accounts, and interchange are unlikely to be enough.

This, in turn, makes the user footprint look more like an email list than a financial services business. As a reminder, with some fraud, those can be good exits (we kid, Jamie!)

Ok, let’s look at GoHenry.

The company targets younger users with a money account that can be managed by the family. It falls into the family of offerings like Step, which are meant to capture financial interest early on in a person’s life. Given the stickiness of banking, being the early primary bank is a meaningful position to establish for a customer acquisition strategy.