Long Take: Deciphering Solana's remarkable 700% rise, and why Ethereum lags behind

The best and the worst

Gm Fintech Architects —

Today we are diving into the following topics:

Summary: We explore the contrasting dynamics in the financial technology sector, highlighting the volatility and potential in various areas. We note the F-Prime Fintech index's remarkable 100%+ increase this year, despite the financial challenges faced by many public companies. Our discussion delves into relative crypto valuation — Bitcoin and Ethereum have seen substantial recoveries from their previous losses, while Solana has surged by 700% year to date. We also examine the challenges within the Ethereum ecosystem, especially concerning its Layer 2 protocols and the impact on ETH's value. Additionally, we express caution over the authenticity of activities in the DeFi space, especially regarding token farming and airdrops.

Topics: capital markets, cryptocurrency, protocol design, F-Prime Fintech, Dave, Adyen, Bonk, Ordi, Solana, Ethereum, Bitcoin, Optimism, Arbitrum, Polygon, Binance Chain, Avalanche, Blur, Galxe, Base, LooksRare, Wormhole, Crypto Punks.

If you got value from this article, let us know your thoughts! And to recommend new topics and companies for coverage, leave a note below.

Long Take

The Knife’s Edge

The financial world seems divided along polarities.

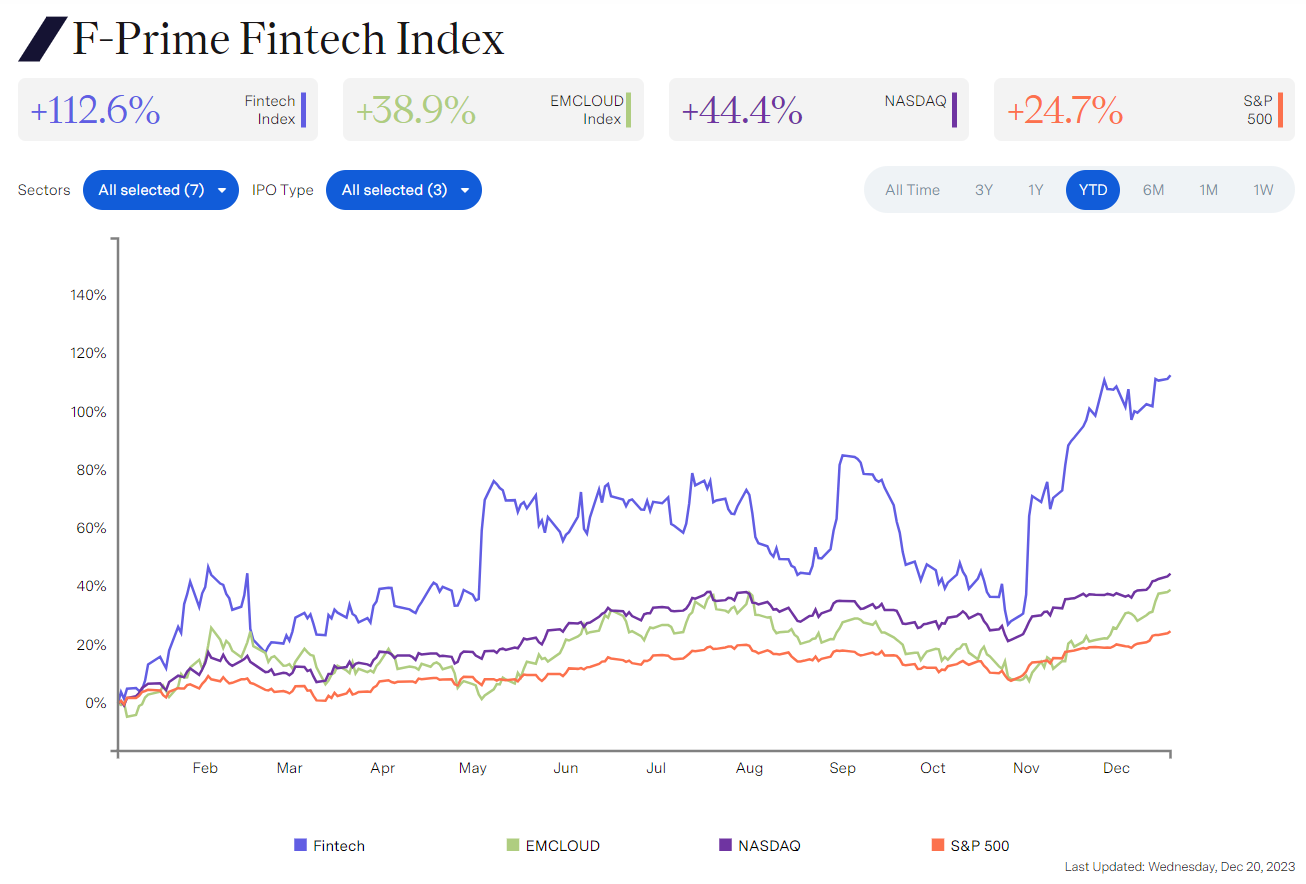

Fintech companies are forever dead and all the IPOs of the past several years are terrible, but also revenues are growing and companies are reaching profitability. See Dave, Adyen. The F-Prime Fintech index is over 100% up this year, even as many public companies bleed out money.

Interest rates have peaked and we have entered a new risk-on regime that chases big tech AI investment, but also interest rates will be higher for longer and funding will remain expensive.

Crypto is too difficult for the next billion users to use and has had its reputation ruined, but also multiple billion dollar memecoins (e.g., Bonk, Ordi) are being minted on every single network and Solana phones are being sold out to arbitrageurs.

These binary outcomes generate immense volatility and risk, and hide within them a high upside. But it is also easy to reason yourself into a corner that is incorrect for the particular moment in the cycle, which could last for years. One mistake is to be so rigorous as to miss human nature. Another is to be too full of animal spirits.

We are spending time talking with both early stage entrepreneurs and institutional money managers. The builders are optimistic, and some are ecstatic. The bull market has come, and capital gains and user influx is here again! On the other hand, the money managers and LPs are reticent, still talking about FTX and regulation.

It feels like being pulled by ropes in different direction.

Value Accrual

Of all the dichotomies, the one most fresh on our minds is between Ethereum and Solana.

Our DeFi readers may be familiar and interested in this topic, while our Fintech and traditional finance readers may find it too far in the weeds. However, there is a fundamental insight in what we are seeing play out that goes to building ecosystems, and figuring out how value flows between market venues. So we encourage the non-crypto natives to consider this battle as similar to the one between mobile operating systems iOS and Android, or browsers Internet Explorer and Chrome.

Here’s the context.

Since the peak of the crypto cycle, Bitcoin has fallen 70% and recovered to a loss of 35%, ETH has fallen 80% and recovered to a loss of 55%, and Solana has fallen 95% and recovered to a loss of 70%.

However, when you look at the number for just this year, while Bitcoin increased 160% and ETH increased 86%, Solana is up 700% year to date. One could say that this is just the law of small numbers — the Solana market capitalization was smaller relative to the others and its losses where bigger, so to reach the same heights as in years past requires more increase.

But that’s not fair, nor helpful. These protocols are not just empty narratives, driven by market makers that manipulate prices. They are too big — at $700B, $250B and $30B — for that jazz. Further, there are *reasons* why prices move around, even in inefficient markets. For Bitcoin, the clearing of the bad actor risk and the broad de-leveraging, as well as the promise of the BTC ETF has catalyzed capital entry into the asset. On the ground, inscription activity of both NFTs and fungible tokens has led to the potential of Bitcoin as a programmable chain.