Long Take: Goldman is trying to build a Fintech powerhouse, and this is how they should do it

Hi Fintech futurists --

This week, we put on the Goldman hat and go shopping for companies. We buy a little bit of Folio and sell some Motif. We look at Personal Capital and the $1 billion it wants for its $12 billion of assets. We examine the private markets with Addepar / iCapital and SharesPost / Forge, and then move over to the banking sector. Should we buy Wells Fargo, as rumored, or some digital wallet apps? Read on for how to acquire a best-in-class Fintech.

These opinions are personal and do not reflect the views of any other parties. They certainly are not financial advice. Thanks for reading and let me know your thoughts here!

You can get more content like this in your Inbox for $3 per week -- the humble price of a delicious Fintech coffee. For exclusive analysis parsing over a dozen frontier technology developments every week, become a Blueprint member below.

Long Take

Wealthtech is one fire, they say now. I am not sure if it is on fire, like doing really well, or like it's just burning down.

There are, all of a sudden, a lot of deals being done across financial technology. Maybe not all of a sudden. Maybe the global pandemic and economic collapse has something to do with it. But there is one layer of observation deeper here. Many of the companies being sold were started between 2005 and 2015. That feels like a venture bet coming to fruition, or founders looking at the likely market environment for the next 10 years, and saying -- no more of the same old. Take the check, be safe.

Here's the alternative:

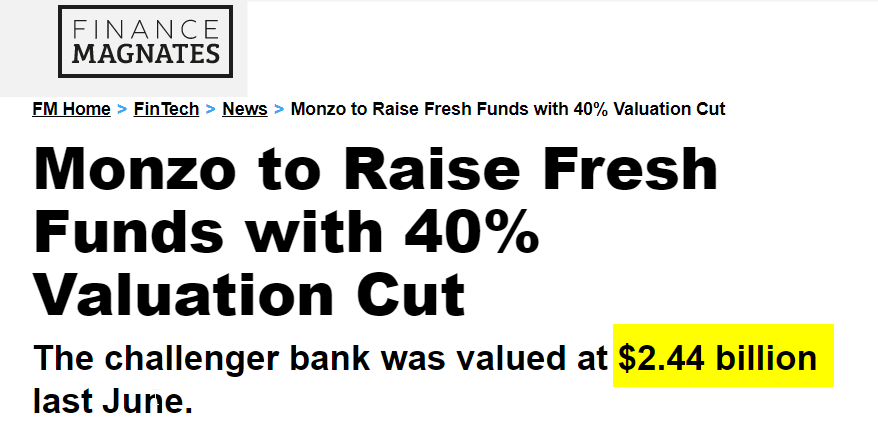

Monzo is still a unicorn, but a billion of equity is appropriately wiped out. Assuming their per user enterprise value was $1,000, $500 is still about ... 5-10x too high relative to customer lifetime value. But I digress.

Let's use Goldman Sachs as our case study and our frame of mind. Why? Because apparently, Goldman Sachs is considering buying up Wells Fargo, PNC, or US Bancorp to accelerate its transformation into a consumer banking brand.

In this missive, we are all the CEO of Goldman Sachs. We have the world's best investment bank and institutional capital markets business, but something doesn't feel right. The world is changing, prices are collapsing, and people are going on about mobile apps and cryptocurrencies.

The Digital Investing Game

Goldman has a plugged in venture capital arm, and was an investor in Motif, Kensho, Circle, among many others. Capital markets and private wealth bets come naturally to the company. With the $700mm+ purchase of United Capital last year, the Goldman's consumer arm added a footprint of mass-affluent and lower AUM high net worth investors (e.g., $1-5mm per client). It felt like a weird move, because companies like United Capital tend to be open architecture, allowing lots of low cost managers to be on the platform. Goldman, however, is incentivized to sell its own large-scale alternative products and proprietary ETFs. The acquisition set the company up to better understand the Registered Investment Advisor (RIA) landscape in the US, and the move to a distributed, localized footprint.

Last week we also learned that Goldman is buying Folio Financial, a niche RIA custodian with $10 billion of assets and 160 employees. In a very strange PR plot twist, this completes the related series of transactions involving Motif Investing. It appears that Motif, which again was partly owned by Goldman, sold its clients to Folio and then its IP and team to Schwab. Then Goldman bought Folio, perhaps learning about the company during the Motif due diligence and being surprised by how future thinking the trading, fractional shares, and direct indexing architecture looks like.

Folio was a thought leader since the late 1990, but never got the explosive traction of firms like Fidelity, Schwab, or Pershing in the advisor space despite having more interesting ideas. The deal closed for less than $500 million -- I would guesstimate a range of around $100 to $150 million, much of which would go to the core operating team. Here's a screenshot:

Goldman has plenty of roboadvisor front-ends to put on top of these engines and make them more attractive to normal human beings. From Marcus to Honest Dollar to Clarity Money, they have been building and buying up interfaces left and right. Folio is for broker/dealer infrastructure and trading tech, not for making clients fall in love with design.

So we now have a custodian chassis with a good engine, an advisor footprint with retail financial planning software, and lots of banking products. What's missing is an actual large digital investing footprint. Remember how Morgan Stanley bought eTrade to compete with Bank of America Merrill Lynch and is Merrill Edge brokerage platform? You are forgiven for not remembering all my favorite Fintech minutiae. Here's a reminder.

Goldman could look at Personal Capital, which is reportedly for sale. I spoke earlier in the week with RIABiz about the potential auction for the company, which is looking for about $1 billion on $12 billion of assets and around $100 million in revenue. I think Betterment broke even at around $20 billion AuM, or $50 millon of cost, though that's not confimed. So the first takeaway is that Personal Capital's "hybrid advisor" cost base is unsurprisingly more expensive than a more digital roboadvisor. The other reason Personal Capital is likely an expensive infrastructure to run is they do data aggregation for 2.4 million people -- an expensive check to cut to Yodlee or Plaid.

Having raised $300+ million is also challenging for Personal Capital, because they need an expensive exit. Users are still priced at a premium, but I don't know what financial institution is currently willing to pay $400 per lead (see the Monzo numbers again). Similarly, the Personal Capital ADV shows 25,000 discretionary clients, which would translate to a cost of $40,000 per client. Ouch! More simply, if RIAs sell for 2% of assets, then $12 billion yields a $240 million valuation, which is below the venture funding they've raised. While there are some real gems of an asset there (the reporting, aggregation, and enabled planning parts of the machine), Goldman already has these assets elsewhere with Folio and United. If a sum-of-the-parts approach is available, I maybe would bid for just the 2.4 million people using data aggregation, and offer $100 million ($40 per lead).

This is all just foreplay.

What I would do as Goldman is lever up and buy Schwab. Goldman has a market cap of about $60 billion, and Schwab is now at $40 billion. Unlike Goldman, Schwab has a real consumer footprint with a relatable, non-alienating brand, and deep consumer technology. While Folio has $10B+ in AUM, Schwab has over $3 trillion. Yes, such a transaction would permanently transform Goldman out of the luxury finance business into the plumbing of the mainstream financial economy. But building a small Marcus version of Schwab and hoping it scales up in a winner-take-all-market is a strategic mistake that has already cost the firm billions.

The Private Capital Game

Goldman is deep in hedge funds and private equity. But putting capital to work and owning the technology network on which the money travels are very different things.

Two recent transactions come to mind: Sharespost / Forge and Addepar / iCapital. After raising over $100 million, Forge figured out a way to close a transaction with its older rival, Sharespost. Both companies create a marketplace for private equity interests. So, if you wanted to buy WeWork shares from an employee (I kid!), their websites would facilitate a transaction without running afoul of regulations. I find the deal a bit of a headscratcher, other than to say that a company founded in 2009 may be a bit tired, and wanting to cash out to a company founded in 2014. Regardless, the end-result is not a bad marketplace and infrastructure, including the requisite regulatory licenses, to support secondary capital markets activity in private equity. And if I am Goldman, acquiring this bundle would be a cheap way to get around $50 million of revenue and some good pipes.

The Addepar / iCapital deal is also interesting. Reminder -- Addepar is a technology to report on the performance of alternative assets, like private equity and hedge funds, while iCapital is a way for advisors to actually invest in them. All the nice stuff I said about Folio and Personal Capital really only applies to equities, mutual funds, and ETFs.

Much of the funding for both iCapital and Artivest has come from private equity firms, like KKR, Blackstone, Carlyle, and the private equity arms of the investment banks. iCapital just raised a $150 million round from PingAn, and seems to have gotten a large club buying into the platform. KKR is converting its Artivest equity into iCapital equity as part of the transaction. That signals that the PE shops realized the benefit of a single network, rather than a splintered network, and pushed to combine distribution channels.

The key issue here is BlackRock, which owns a meaningul portion of iCapital. But the world's largest asset manager chose to cancel its option to take over the business, signaling that it is either too expensive or there are better things to do with life than fret over leveraged buyouts. Either way, our massive Goldman/Schwab conglomerate can be the white knight and pick up an easy $40 billion of alternatives coverage.

The Banking Game

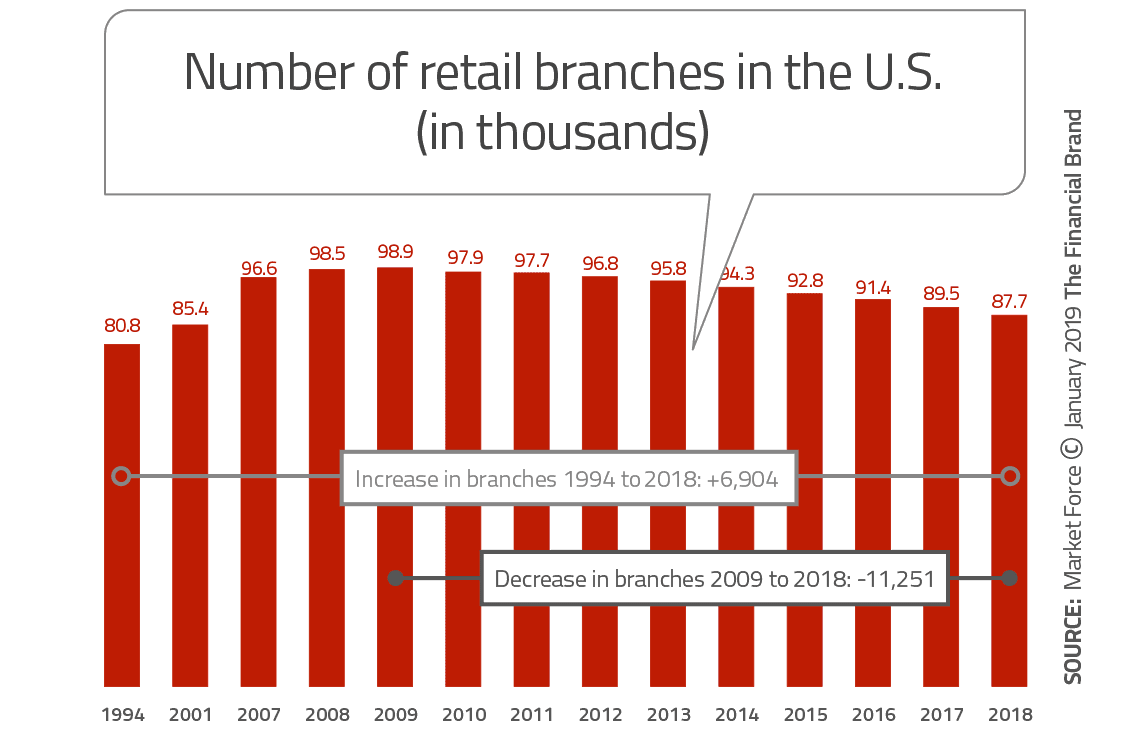

I guess this is where Goldman feels most exposed, not having a fat bank footprint and all. If only we had more bank branches. Oh wait, never mind:

You don't need more branches! People are literally scared of going into branches.

What you need to do instead is make a smart play on what matters in banking. I did a podcast last week with my friend Will Beeson and ARK analyst Max Friedrich, and our conversation spent a lot of time on the difference between a mobile bank and a mobile wallet. This is really key. Depending what experience you put first can determine the difference between success of ultimate failure.

In the COVID world, interest rates will stay at 0% as governments print Market Monetarism-inspired bailouts. This means that bank interest income spreads are going to stay hyper compressed, and lending will be a dangerous game. Companies like OnDeck, which were worth over $1 billion a few years ago are now on sale for $30 million as their loanbooks are written down. Further, as unemployment spikes and fewer people have direct debit income into their bank account (because there is nothing to debit), balances will grow at a lower rate or shrink. Mobile banks, like Monzo, have had the rug pulled out from under their feet. A regulatory license won't save you.

However, mobile payment apps like Venmo or Square Cash, are seeing strong volumes. I imagine some Stripe-powered eCommerce sites are similarly seeing a surge of retail activity. People will continue to shop online and transact digitally, once they are onboarded into these easier transactional experiences. To that end, a payment model may be a better entry point than a deposit-oriented model. Instead of looking at a beauty like Wells Fargo, I would look instead at Square (now $35 billion marketcap) or another modern payment processor that could be leveraged into a bank-like experience. Alternately, one could go shopping for things like OnDeck (small business lending Fintech) or Bancorp (pre-paid card issuer), figuring out better ways to solve balance sheet problems while incorporating higher quality Fintech assets into the footprint.

So there you have it. Goldman Schwab Square. All I ask is my 5% investment banking fee.

Or you could just spend $3 per week to get more of this newsletter.

Amazing essay this week. Very compelling ideas.