Long Take: Launching our AI indexes, and reflecting on the Web3 AI mega-merger

How SingularityNET, Fetch.ai, and Ocean Protocol aim to reshape the Web3 AI landscape.

Gm Fintech Futurists —

Quick reminder about the upcoming change in our publishing schedule and price plan.

We will publish Monday and Thursday, and premium is priced at $12/mo or $99/year. To accelerate the transition, we are offering an $89 annual subscription before the end of March. Grab the deal before it is gone.

Thanks for your attention and support, and a full open Long Take is below.

Today we are diving into the following topics:

Summary: The recent news that SingularityNET, Fetch.ai, and Ocean Protocol are merging their tokens to form a mega project in the Web3 AI space marks a significant development, reflecting the sector's response to the dominance of big tech AI companies like OpenAI and Anthropic. With Web3 AI gaining momentum, underscored by the growth of ecosystems like Bittensor and initiatives within the Polygon and NEAR communities, this consolidation aims to create a project capable of competing with leading tech giants. Additionally, we introduce a systematic approach to tracking market movements through indices focused on Western AI, Eastern AI, and Decentralized AI, revealing significant performance disparities among them. This analysis underscores the dynamic landscape of AI development and investment, with Web3 AI showing remarkable speculative growth compared to its Western and Eastern counterparts.

Topics: SingularityNET, Fetch.ai, Ocean Protocol, OpenAI, Anthropic, Stability AI, Inflection AI, Bittensor, Morpheus, Polygon, NEAR, NVIDIA, Microsoft, Alphabet, Meta, UI Path, IBM, Alibaba, Baidu, Iflytek, CloudWalk, SenseTime, Fourth Paradigm

If you got value from this article, let us know your thoughts! And to recommend new topics and companies for coverage, leave a note below.

In Partnership

Generative Ventures invests in the machine economy — the financial activity settled on blockchain protocols and accelerated by the machine labor of generative AI.

Long Take

Catalyst

The news just hit that three of the top AI projects in Web3 — SingluarityNET ($2.6B fully diluted value), Fetch.ai ($3.7B), and Ocean Protocol ($2B)— are working on merging their tokens to create a mega project together.

We find this fascinating for a number of reasons.

First, the big tech AI companies, like OpenAI and Anthropic, continue to get incredible usage, technical progress, and higher valuations. Their war chests are growing, and their software is being integrated into all the Web2 footprints, e.g., Microsoft and Google. Some of the lagging early leaders, for example, Stability AI and Inflection AI, are in chaos. It doesn’t pay to be in the middle of the pack when all the returns concentrate at the top.

That said, the Web3 AI space is also booming. We have articulated this before in an investment thesis. But more importantly, there are a number of talent ecosystems now developing around large funding pools. The first and most obvious is Bittensor, the $12B hyper-structure meant to incentivize multiple subnets of different models competing for machine labor (i.e., inference work). Another is Morpheus, being built on top of ETH rewards from staking into their validator. Others will come from the Polygon community, NEAR, and other protocol founders. The prize pie is simply too large.

Therefore the consolidation of SingularityNET, Fetch.ai, and Ocean Protocol makes sense as an attempt to create a large enough counterweight. We expect there aren’t that many spots for these mega projects — probably 5 spots total, with the top 2 spots eating the majority of investment capital. The same is true for the big tech plays, with valuations likely at 10-100x of where we are today in Web3.

Token-based mergers are notoriously difficult. The base template is to create exchange ratios from each of the tokens to a new token, and set up a smart contract that allows people to convert their holdings. Unlike a traditional merger, where the underlying stocks are custodied and can be dragged along, here the assets are non-custodial, and therefore you will inevitably have a whole bunch of orphan tokens.

We’ve written in more detail on this topic before here:

It will be tough to pull this off, but that said, it is fantastic to see the decentralized alternatives thinking about how to compete with more traditional AI companies.

Benchmarks

Let’s systemize our approach to tracking these markets outside of anecdotes.

One strategy is to define an index of publicly traded assets. Of course, this will exclude some of the best companies in this space, who have chosen to stay private (e.g., OpenAI, Mistral, Huawei).

Given the limited data accessible to us, we will make these benchmarks (1) equal-weighted and (2) composed of 6 positions each. Other approaches would rely on volume or marketcap weights, but let’s keep it simple. There are three ecosystems we are interested in: (1) Western AI, (2) Eastern AI, and (3) Decentralized AI. For each, we want to take a sampling of the different parts of the value chain.

Here is a very high-level metaphor of the AI value chain.

Underneath it all is the robot body, built from the hardware of data centers, computational networks, and GPU cards. On top of this, we have the sum of all human knowledge and experience, scraped as data from the Internet and organized into latent spaces by mathematics, tagging, and reinforcement. Further above, the robot mind exhibits machine intelligence, hallucinating — or perhaps merely rendering — the work products of content, language, image, and decision using different models and algorithms. Finally, frameworks for objective-seeking package this unorganized mind into agents that behave like individuals, rather than a chaotic Borganism. These agents take actions in the real world, which can be formatted as regular applications that people encounter on their phones and websites.

Such a metaphor can help us get started. It maps imprecisely but helpfully to the real industry value chain. So let’s take a look at our Western AI index positions first.

NVIDIA. $2,250B marketcap. Nvidia is the hardware body of nearly all AI, building the chips on which the robots process.

Microsoft. $3,100B. Its products include the cloud, numerous applications, and models, deployed across the entire stack.

Alphabet. $1,860B. The company’s acquisition of DeepMind positioned it to build powerful models, but of course Google is also invested heavily in applications.

Meta. $1,250B. Strong in building open source models, with large bets on the Metaverse and Identity. This is a natural AI agent play.

UI Path. $12B. We include the much smaller company, with its history in robotic process automation, for exposure to industry and AI agents.

IBM. $170B. The enterprise version of minds, bodies, and agents.

Over the last year, NVIDIA has led in performance, generating 3.5x returns — deeply surprising given the enormous size of the company. Meta’s recovery is second at 2.5x, but ahead of MSFT, UI Path, and IBM. The overall index puts us at 2x during the last year.

Now let’s do the same for Web3 AI. Given the previously discussed merger of protocols, we will start with 8 positions, 2 of which will be consolidated going forward.

Bittensor. $12B fully diluted marketcap. The project creates cryptoeconomic incentives for model operations and competition.

Render. $5.9B. A decentralized GPU network, one of many that has come to market, but likely the most highly valued.

Fetch.ai. $3.7B. Platform to build AI apps and services, which maps to actions in our metaphor.

SingularityNET. $2.6B. Decentralized model network, crowd-sourcing the machine mind.

Ocean Protocol. $2B. A project focused on data and its usage in AI, analogous to the senses and training needed for a mind to operate.

Akash Network. $2B. Decentralized compute network for renting and providing computational capacity.

OriginTrail. $600MM. We include this to highlight applications around tagging provenance and anchoring them onchain, one of the key ideas in Web3 AI.

Olas. $2.5B. A network for building and deploying decentralized AI agents.

This is a bit hard to read, so let’s try a log view.

You can see the power of an early project becoming one of the main assets in the space, evidenced by Olas growing into a $2.5B valuation from nearly nothing at $0.15 to over $4.00 per token, generating 30x returns. Singularity, Fetch, and Ocean — the assets that are merging — have lagged the rest of the comps this year. We think this is due to their already large size, as well as their vintage. New things are unknown and have not stalled out yet, and thus are afforded higher growth by the crowd.

A comparison of the two indexes shows that an equal investment in each would double your money in Western AI, while multiplying it by 11x in Web3 AI. This is a function of much more profound speculative pressure and investing in smaller companies. If we remove Bittensor and Olas from the calculation, Web3 AI still delivers an 8x multiple.

Can this performance be replicated going forward? Hard to say. But it is the space we are watching most closely.

Finally, let’s look at Eastern AI. The Chinese markets have been impacted by various negative macroeconomic and political factors beyond the scope of our discussion here — from credit issues, to problems in real estate, to the tensions with the US over access to semiconductor technology at the root of AI hardware. Further, many of the Chinese firms we list are part of the state apparatus by design, deploying AI capabilities like facial recognition across the general population. As a result, they are unlikely to be speculative economic champions like NVIDIA or Bittensor.

Nonetheless, here is the Chinese big tech industry working on AI. See this article for deeper detail, which we use as a source.

Alibaba. $1,300B marketcap. Tech mega-firm developing various multi-modal models and exploring AGI, backed by proprietary cloud infrastructure.

Baidu. $280B. Among other products, built a large language model competitive with GPT4, combined with deep learning.

Iflytek. $100B. Specialized in multi-modal and language models.

CloudWalk. $13B. Famous for its facial recognition models.

SenseTime. $23B. Home to a large hardware facility as well as a leading models, partly state owned.

Fourth Paradigm. $30B. Builds enterprise software using generative AI and runs platforms across industries.

You’ll notice fewer consumer-focused companies on this list, such as retail AI agents. Those types of functionalities would likely be built into the larger platforms and centrally controlled. Further, Huawei the Apple/NVIDIA competitor, remains private and is thus off the list.

So how is the financial performance?

Things are not looking great from a wealth creation perspective — the index is down about 35% on the year, and nearly all the companies are down for the year in dollar terms. This is meant to be a block-buster moment for AI, and China leads in academic talent and research papers. From a market perspective, however, we are not seeing success yet.

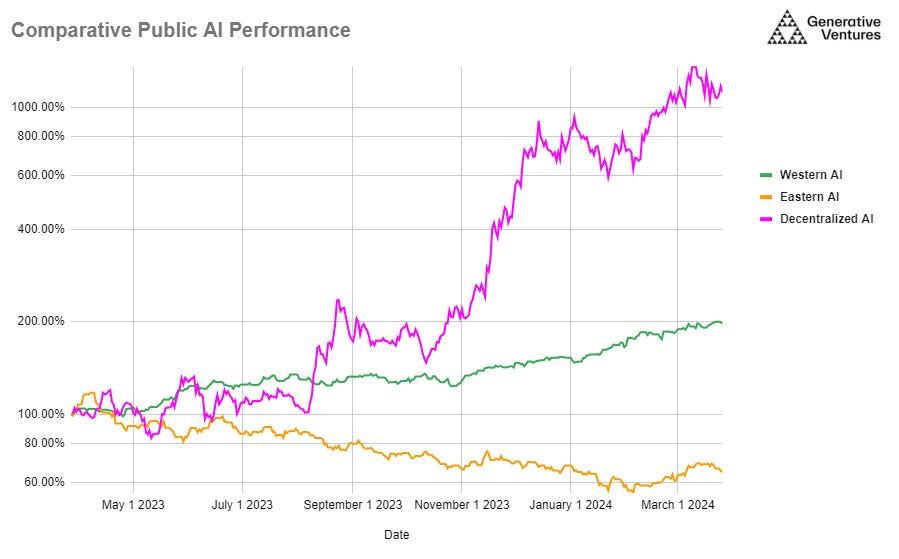

So, what does this look like when we put it all together? The scale requires us to use a log axis again.

While the performance of the last 12 months tells a strong story, we should not look too deeply into it at this point. One could wax philosophical about the exponential growth in self-sovereign software, beating out both hyper-capitalist centralized tech firms, and the state-owned surveillance companies.

But that would probably be the wrong take away. More likely, the performance of these trends is driven by their correlation to macro-economic exposure — crypto recovering with the Bitcoin ETF, NVIDIA powering the OpenAI boom amidst equities recovery and flat rates, and the Chinese companies witnessing the outcome of global political and market pressures.

As time passes, however, we will use this data as a tool to benchmark progress to date in what is likely one of the major technological shifts in all of human history.

Postscript

Read our Disclaimer here — this newsletter does not provide investment advice

Another friendly reminder to share this post so that others can learn: