Long Take: The Law of Unintended Consequences via Wells Fargo, Divergence Ventures, DeFi designs, and the Federal Reserve

Long Take: The Law of Unintended Consequences via Wells Fargo, Divergence Ventures, DeFi designs, and the Federal Reserve

Gm Fintech Architects —

Today we are diving into the following topics:

Summary: We focus on the law of unintended consequences, and how making rules often creates the opposite outcome from the desired results. The analysis starts with the Cobra effect, and then extends to a discussion of the Wells Fargo account scandal, dYdX trading farming, Divergence Ventures executing Sybil attacks, and Federal Reserve insider trading. We touch on the concepts of credit underwriting and token economies, and leave the reader with a question about rules vs. principles.

Topics: Microeconomics, token design, fraud, compliance, banking, decentralized finance, venture capital, insider trading

Tags: Wells Fargo, dYdX, Divergence Ventures, Sybil Attack, Federal Reserve, SoFi, MoneyLion, Compound

If you got value from this article, please share it. Long Takes are now premium only, and we need your help to spread the word about how awesome they are!

Long Take

The Law of Unintended Consequences

Economists enjoy a simple, clearly defined model. A model where people are rational actors, and where the system in which they interact is reduced to clear deterministic functions. A model where everything makes sense!

This is why economists are pretty much always wrong.

The law of unintended consequences comes into play when a rule or policy generates an impact that is quite contrary to the initial goal, and often is in contradiction with it. Here’s a fun example from Wikipedia:

The British government, concerned about the number of venomous cobra snakes in Delhi, offered a bounty for every dead cobra. This was a successful strategy as large numbers of snakes were killed for the reward. Eventually, enterprising people began breeding cobras for the income. When the government became aware of this, they scrapped the reward program, causing the cobra breeders to set the now-worthless snakes free. As a result, the wild cobra population further increased. The apparent solution for the problem made the situation even worse, becoming known as the Cobra effect.

There are countless other examples. They reveal a disconnect between (1) the rules people make in order to accomplish some goal, and (2) the actual causal patterns from that rule, and the many ways that different actors attempt to game and manipulate the system, as well as the various externalities that loop back on each other and amplify completely unexpected outcomes.

In economics, we often say “all else being equal” when proposing an explanation or trying to run a regression.

But all else is neither equal nor static. Rather, systems are “dynamical”, implying an progression over time between states, and “complex”, suggesting that there are many interdependent causal components creating random-seeming outcomes. Imagine a jungle and its plants and animals as an example. Change just one small thing, and the equilibrium of the whole thing is thrown off balance.

Just Trying to Run a Business

Imagine you are working at Wells Fargo in 2010, and have the fantastic idea that selling more products to existing customers is easier than selling single products to new customers. So you start thinking about incentives, and thinking yourself very smart. After a while, you design a compensation plan that “aligns” bonuses to the number of products that a customer uses. The customers are sticker and more loyal, revenue per customer is higher, and all the McKinsey industry metrics look better.

So far so good. You also remember that most customers use branches, and that you have a lot of staff in those branches still. What if branch staff got paid more if they persuaded customers to use more products? Go where your customers are, they said!

It works! Revenues are going up and we are all cross-selling. After a while though, results begin to level off. So you exert some additional pressure, squeezing what you can from the machine. And then you exert some more, and some more. It still works! The numbers keep going up.

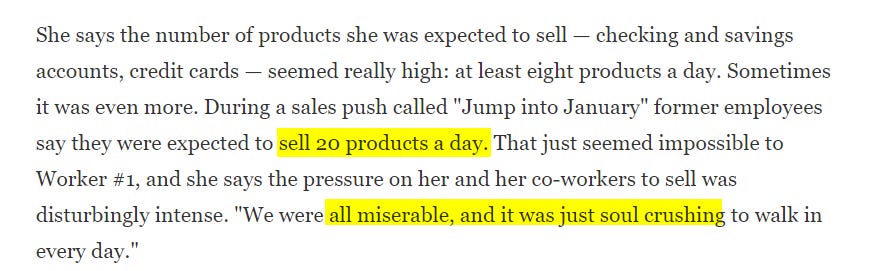

Until the other shoe drops. Many of us are familar with what actually happened in the Wells Fargo account fraud scandal. The pressure from the top made everyone go insane, trying to adapt to the hamster wheel of financial model expectations. Branch personnel cracked, and began to fabricate accounts in order to hit sales quota.

Not like, a couple of accounts. More like, 3.5 million accounts. And the practices to open these accounts became appalling — from taking control of customers’ account pins, to moving legitimate money into accounts without consent, to selling insurance products that people didn’t actually buy. People might have had their credit ratings damaged as well by not paying annual fees on accounts they never really opened.

All in, Wells Fargo has to pay $3 billion in damages across fines and lawsuits. Ha! That’s about right for fintech — $1,000 valuation per account. The judge must be a venture scout at SoftBank.

It is easy to be glib and place the blame on “bad people”. Surely the branch staff were doing a bad thing willfully? Maybe, but clearly they wouldn’t be doing that thing if there wasn’t a policy forcing them to cross-sell beyond the edge of reason. As we know, individuals become very compliant to social consensus, even when that social consensus deserves moral outrage (see the Milgram experiments).

Surely the management was doing a bad thing setting this evil policy? Maybe. But also maybe they were stuck on the hamster wheel of quarterly earnings for the capital markets, which pushed them to generate untenable assumptions in spreadsheets, and a sort of willful blindness to the irrationality of what they were asking at a macro level. Surely capitalism is bad for creating hedonic and financial hamster-wheels that melt our minds and sense of independent self? Maybe, but also Netflix is great. Have you seen Squid Games?

The main point here is that (1) a simple rule of wanting cross-selling, backed by good evidence, (2) was leveraged to a very large scale through the organization, and (3) led to a whole bunch of externalities and unintended consequences. And the reason it did so is because the rule doesn’t control the outcome. There’s an equilibrium for the amount of bank products people get, and it is driven not *only* by how well the branch tries to sell you things, but by what you actually need from the branch.

And more generally, over-indexing into trying to optimize some particular metric creates perverse incentives and weird unwanted outcomes. For wealth management, we can talk about the fiduciary rule, and how it attempts to align incentives. For venture capital, we can talk about over-optimizing for valuations over business performance. For public companies, there’s next quarter profitability killing innovation. For health insurance, it’s the loss ratio encouraging less payouts. And so on and so forth.

Think this is all in the past? Every B2C fintech these days is set up like Wells Fargo, trying to convert people from trading to banking, from lending to investing, and from payments to crypto. Beware young Padawan of all that glitters.

Proof of Use and Proof of Community

You didn’t think we’d get away with a write up on incentives without talking about crypto? The Wells Fargo cross-sell rule is child’s play compared to the next level system engineering happening in Web3.

A simple example is yield farming. First a reminder on PayPal — the original paytech company offered new customers a $20 sign-up and referral fee, which later decreased to $5, and phased out all together, with PayPal spending over $50 million on the program. This was a marketing expense in order to acquire customers and grow the enterprise value of the company for shareholders. There was little overlap between consumer benefit and owner benefit.

Yield farming was truly kickstarted by Compound (our interview with Robert here), by paying lenders and borrowers for financial activity with the tokens of the protocol. The more you borrow, the more you get paid in the value accrual mechanism of the venue where you borrow. The approach spread to market making and asset management, and is a staple for bootstrapping decentralized financial networks now. It is a strategy that is far more supercharged than what PayPal did because the consumer benefits from their own use, and the use of the community, through financial exposure.

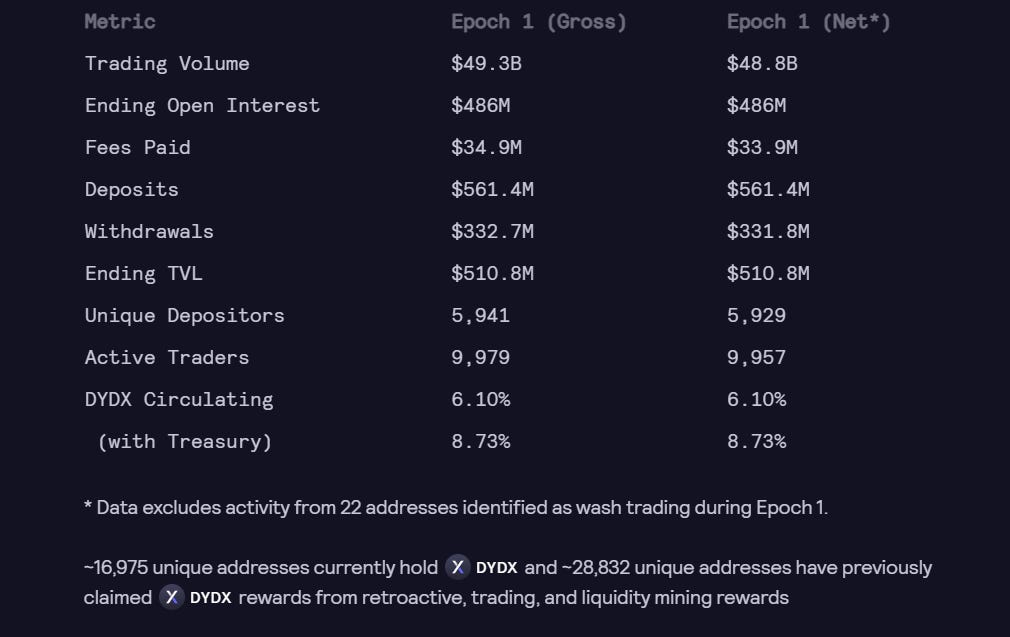

The aligned incentive is that there is a reward for overcoming ennui — the desire to do nothing — as well as by compensating someone for taking on an early technology and operating risk. But of course, there are also perverse incentives. You might not need that loan or that trade, but you get paid to make it. Take a look at the incredible August 2021 metrics for dYdX, a decentralized derivatives protocol that recently did more volume than Coinbase.

One catalyst for the growth is Chinese investors looking for non-custodial venues for trading, and given that dYdX is onchain and is performant via a Layer 2 solution, it is in a fantastic position to serve traders interested in derivatives. Another catalyst is that trading on the protocol yields a reward in the form of the dYdX token, which now has a marketcap of $1.3B (or $20B+ fully diluted). This is a strong example of a token catalyzing people to perform the type of activity that the venue wants — more trading.

You don’t need a Wells Fargo suited boss yelling at sales people to sell more derivatives. Customers are doing this themselves with clear intent and purpose.

The underlying principle with token distributions is that they should align with the community of the protocol that they serve, such that the community can financially benefit from their use and promotion of the protocol. From the perspective of the instrument itself, it is important to demonstrate that the token is one that generates some type of utility, meaning it has a particular use within the software, and that users are using that token for its intended function, rather than merely for speculation.

Thus, professional traders getting excited about trading rewards feels a lot better than bank customers tricked into trading through corporate policy.

However, there are unintended consequences here too. Communities now know that they may get rewarded for participation. They anticipate valuable rewards embedded in the usage of various protocols. This in turn incentivizes pre-emptive farming of protocols, in case there are future reward distributions based on prior activity. If you know that I know, and I know that you know, what DeFi are we all going to farm?

This explains the recent controversy with Divergence Ventures, which essentially executed Sybil attacks on the Ribbon Finance protocol. That means that it created a whole bunch of accounts with some particular activity to increase the surface area of a potential area of token distribution (i.e., an airdrop).

A simple example is this – imagine you have 100 users with 1 account each, and you want to reward them within a $10,000 budget. Each user gets $100. Now let’s say one of the users knows that the reward mechanism is based on the number of accounts at some particular dates, and goes on to create another 100 accounts for a total of 200 accounts, of which they own 101. Now, the $10,000 is sent to 200 accounts with $50 each, and our enterprising player receives roughly $5,000 of the total, instead of the native $100. It pays to create these accounts, and this has became an explicit strategy for a number of crypto investors.

We shouldn’t think of this as a primarily ethical failure, in the same way the Wells Fargo branch personnel aren’t singularly to blame. Rather, it is a system design issue, largely by well-meaning parties trying to get productive financial activity to occur. If you know that rewards will be distributed for having an account, you make lots of accounts.

In some way, this starts to veer into a discussion of insider trading problems, and how fuzzy those gray lines can become. Insider trading is obviously illegal because it harms investors who do not have insider information, and this has been written into law. But how about public information that someone received immediately after it hits the wires, because they work at Goldman Sachs and have a Bloomberg terminal, vs. someone who received it much later because they don’t have a Bloomberg subscription. And let’s that the access to information correlates with income and education level, and is in fact an income-class driven feature. At what point is what fair and to whom?

Generally, you want insiders to have maximal information about their project or business to operate it well. It just so happens, however – as an unintended consequence -- that the value of such information may be worth more to them as applied to public or crypto market speculation than actual operating performance. Such a consequence arises because capital markets exist alongside employment markets. As a result, insiders may be incentivized to misuse the information, rather than benefit the community. We might have a lot less problems with insider trading if we could drag-along with them – it perhaps would generate better decision making for everyone.

Take for example the recent coverage of Fed officials who performed some multi-million dollar portfolio rebalancing based on their insider knowledge of interest rate announcements. The moral outrage is coming from the view that these individuals made large systemic decisions that impact their community and country, and then used the derived implications of those decisions to benefit themselves in investment activity. If they had instead contributed those gains to the public good or rebalanced some large communal DAO treasury, they may be perceived as heroes of the public good, rather than disconnected arcane money priests.

Key Takeaways

A final word on credit worthiness, identity and underwriting.

Once you start seeing how our rules create things we don’t want, rather than the things we do, the pattern becomes apparent in all sorts of places. We know that account farming is a thing we don’t want, and instead we want a single view of the person, just like dYdX or Ribbon doesn’t want to reward accounts but entities instead. One way to do that is to focus on volume or asset based metrics. Volume can still be spoofed through wash trading, but assets are assets. This is why Proof-of-Stake relies on committed capital as the metric for rewards, and why most DAO voting is done with straight voting rather than approaches that subsidize small holders.

Now take credit underwriting. In trying to get the best view of underwriting risk, in order to be able to profitably take on a risk, banks require the full financial view of a person. This creates the need to summarize a fragmented financial experience into a single coherent picture, therefore leading to at least one concept of *identity*.

And yet, this very grouping can end up being a tool of financial disenfranchisement, because the ability to cohere your stuff into a single package and the ability to pay off a loan are quite different things. And further, access to services that allow one to neatly package a credit history, well organized bank accounts, and so on, again pre-suppose a certain selection bias that may be rooted in cultural and social reasons.

The unintended consequence of these precedents are fintechs like MoneyLion, Current, GoHenry, Step, that have a value proposition of a “credit builder” bundle that reformats customers into the type of shape that mainstream financial engines require. In turn, some of these companies overcharge for their services, doing more to prevent their customers from financial access, rather than helping them get there.

Is this a thing that is fixable? Or are we doomed to make rules that spit out side-effects befuddling our attempts at a sane world? One concept we leave to the reader is to focus on (a) principles rather than (b) strictly specified rules. Such an approach both gives us more responsibility, and asks more of us all, especially thinking about the concept of a true public good.

More? More!

Another friendly reminder to share this post so that others can learn:

Want to chat? Stop by our (pretty empty right now until you join) Discord!

What did we miss? Reach out here anytime.