Short Takes: China bans Bitcoin (again!) & surveils Ant Group lender; $36 trillion custodian State Street's $3.5B deal; NFT royalty model and crypto Twitter tips are here

Good morning Fintech Futurists —

The world is changing, and so are we! Starting this week, the Monday piece will re-focus on short analysis of the top 3 developments followed by a list of key links, and summaries of deeper analysis and podcast sessions. This remains free.

Long Takes are moving to Wednesday. Over the next 2 weeks, everyone will get everything to see the new structure. Afterwards, the longer analyses are going to be premium-only. For paid members, there is nothing you need to do. For free subscribers, check out your options here.

If this causes a financial burden but you rely on the research — apply to join the Ambassadors program that we are building here. This will allow access in exchange for active ongoing social sharing and community conversation. 10 Spots to start.

And with that, our agenda for today is:

CHINA TECH: Ant Group microcredit service Huabei feeds vast credit data to China’s central bank (link here) and China Cracks Down Harder on Cryptocurrency With New Ban (link here)

NFTs & CRYPTO: Every Time Someone Streams 3lau’s Next Song, Fans Will Get Paid (link here) and Twitter accelerates again with Bitcoin tips, NFTs, recorded Spaces, creator fund and more (link here)

INCUMBENT M&A: State Street’s $3.5 billion acquisition of Brown Brothers Harriman Investor Services makes it the biggest US custodian with $36T+ in assets (link here)

RESEARCH: Unlocking Demand-side growth with Square's payment network and Goldman's GreenSky acquisition (link here)

PODCAST: What's next in Web3? Tachyon Accelerator's MD Gabriel Anderson on early stage in NFTs, DeFi, & Crypto (link here)

In Partnership:

Attention Web3, creator economy, metaverse, and fintech founders! Check this out.

Launch House is a private community focused on connecting and supporting top entrepreneurs. We believe that the future belongs to those who take action and launch. That progress happens when great people work together to empower the underdog. Join the next cohort of the 4-week the Founder Residency here.

Fintech Meetup is the easiest way to meet new partners and customers! Meet fintechs including Agora Services, Atomic, BillGo, BlueSnap, FISPAN, Synctera (and hundreds more!), banks including JP Morgan and Goldman Sachs, Investors, Networks, Processors, Solution Providers, Credit Unions & CUSOs, Community Banks and many, many more! Special startup rate available. Get tickets here.

Short Takes

CHINA TECH: Ant Group microcredit service Huabei feeds vast credit data to China’s central bank (link here) and China Cracks Down Harder on Cryptocurrency With New Ban (link here)

Recent news relating to China’s tech regulation read to us like an exercise in control. You control things that bother you, things that are counter to how you want the world to be. If you start controlling things that are trivial, it means they must bother you a lot, and reveal a certain fragility about your grip. Perhaps the same can be said of American regulation.

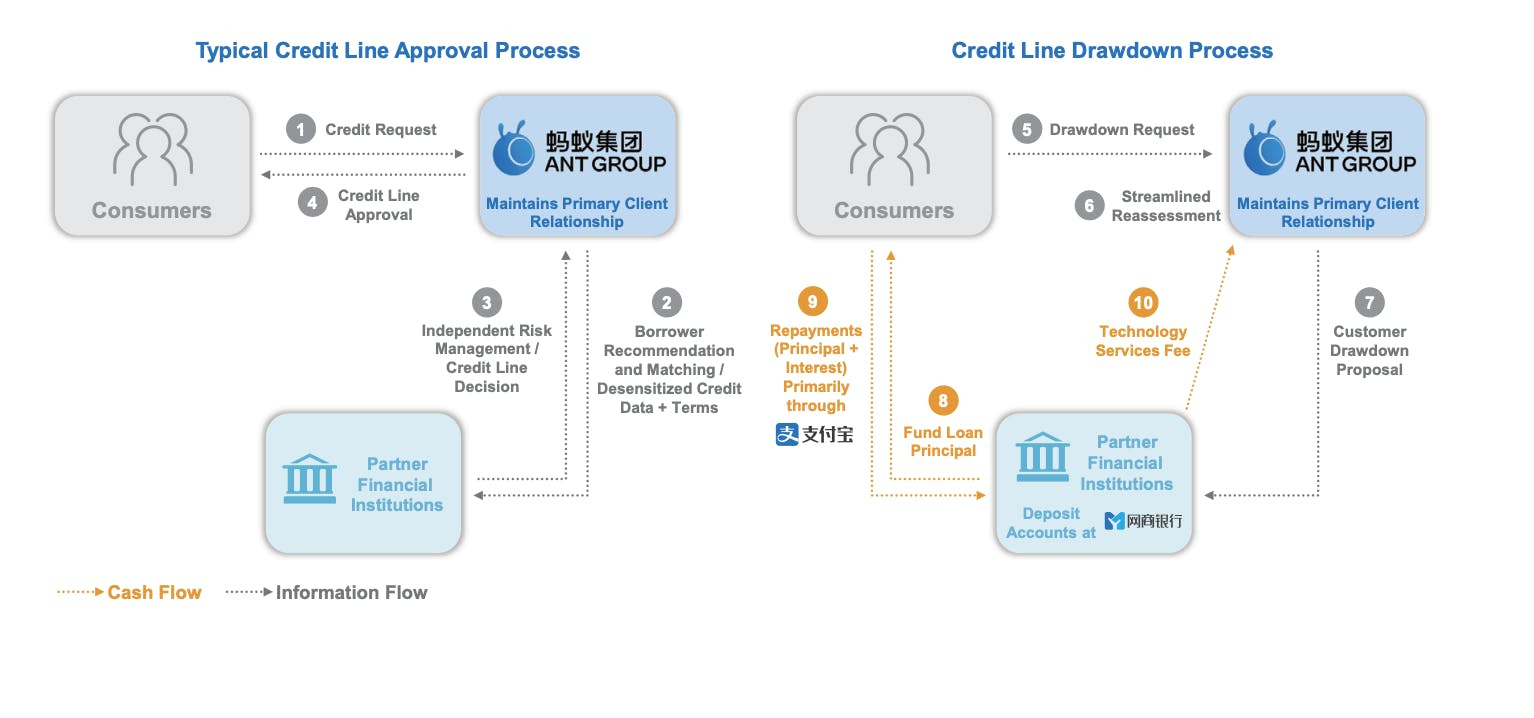

With that said — Huabei, the small loans service owned by the Ant Group, is now feeding its consumer credit data into a database run by the People's Bank of China, as the nations ups the presence of regulatory oversight. The information passed across on a monthly basis includes the dates accounts were set up, amount and usage of credit line, and status of repayments. The US government is trying to do the same thing for “tax purposes” in the infrastructure bill, but at least there is resistance.

This move is in line with the mandatory data-sharing agreement setup by China's credit investigation industry regulation, whereby Ant Consumer Finance is required to follow the same rules as a traditional bank. To put the data into context, (1) about 500 million people have borrowed from either Huabei or Jiebei in the twelve months to June last year, (2) total payment volumes on Alipay reached US$18.3 trillion in that same period, and (3) Huebai and Jiebei account for 39% of Alipay's revenue last year. All in all, the move is an expected one as part of the post-Ant-IPO-shenanigans.

But wait, there’s more! China’s central bank also extended its earlier anti-crypto stance, which focused on mining, to apply to all crypto currency services provision. This includes trading, staking, and for banks and exchanges to facilitate transactions. Sounds scary! The reaction from the industry so far has largely been (1) to point to the fact that Chinese bans of crypto tend to drive up crypto prices, and (2) that we may see an influx of funds to DeFi services that are censorship resistant as money moves out of centralized exchanges to onchain destinations.

Our key takeaways is to follow these developments as spotlights — something to pay attention to because it is important to important people — but to draw our own conclusions on fundamentals. There’s fat macro risk caused by Evergrande and the meltdown of property-backed commercial paper markets, putting 1-3% of GDP at play. There’s impact on USDT and the systemic correlation from that to the rest of the crypto markets. This stuff is a powder keg, but it’s not on fire yet.

NFTs: Every Time Someone Streams 3lau’s Next Song, Fans Will Get Paid (link here) and Twitter accelerates again with Bitcoin tips, NFTs, recorded Spaces, creator fund and more (link here)

Royal, a blockchain-powered marketplace founded by 3lau, was created by DJ/producer 3lau to utilise an NFT based model for songs. Songs will be put up as for-sale items, letting users buy songs and earn returns on their sales. As an example, 3lau is giving away 50% of streaming rights to his new song "Worst Case" to 333 fans. In turn, this provides the consumer with a new investable asset class, i.e., royalties, and also incentivises them to stream and advertise the music more. Fans become investors.

Royal raised $16 million this August, and has more than 2,000 artists interested in listing since its announcement, with 200 of these having 500,000+ monthly listeners, many in the millions, and a couple with 20 million plus. Check out our Long Take on the tokenization of royalties using NFTs, and the current state of play.

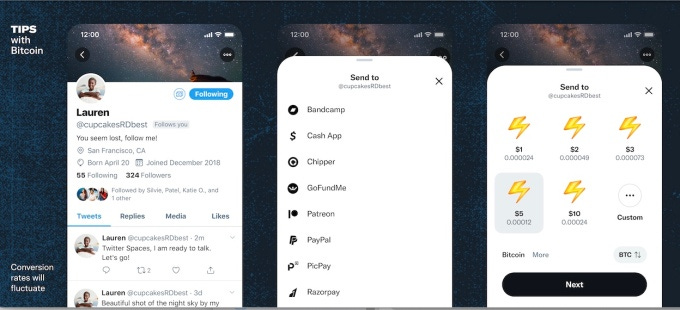

We also point to Twitter’s recent integration of Bitcoin tips into its core payment chassis around social media profiles as adjacent news.

What you can see starting to form is a different shape for social media, its creative output, and the economics derived from that. Our social networks remain important, and perhaps some existing platforms like Twitter or some of the music labels will continue on. Yet consumers are being turned into owners and capitalists by the manufacturers of culture — perhaps in response to the downsides of the “gig economy”, and the subscription model over-indexing of the last decade from Silicon Valley. We think this is an economic dialectic.

M&A: State Street’s $3.5 billion acquisition of Brown Brothers Harriman Investor Services makes it the biggest US custodian with $36T+ in assets (link here)

State Street will soon be the biggest US custody financial institution after completing a $3.5 billion acquisition of Brown Brothers Harriman Investor Providers (BBH). The move pushes BNY Mellon and JP Morgan Chase off the top of the AUC pedestal. With the acquisition comes $5.3 trillion in assets under custody at BBH, bringing State Street's total to $36 trillion.

Adding to that, BBH supposedly brings with it a "best-in-class fintech asset", which integrates a variety of vendor solutions around trade management and collateral management, operational FX, corporate actions, reconciliation, IBOR, and of NAV validation. The service will be added to State Street's knowledge service, Alpha, once the deal completes in the next 12 months.

Presents At Citi's 2020 Financial Technology Conference - Slideshow (NYSE:STT) | Seeking Alpha")

We can see that consolidation is the primary lever of growth when you are operating at this scale. State Street and its competitors aren’t afraid to drop a few billion on horisontal M&A activity, with a prior transaction of $2.6 billion for Charles River Development. That also implies a correlation with a price war around custody services. A deeper take on M&A strategy across company stage and risk tolerance can be found here.

Rest of the Best

Here are the rest of the updates hitting our radar:

BNPL: Zip enters India with $50 million investment in ZestMoney (link here)

INCUMBENTS: JPMorgan adds to tech acquisitions with college platform Frank (link here)

INCUMBENTS: JPMorgan Chase to replace US retail core with Thought Machine's Vault (link here)

DEFI: Crypto custodian Cobo raises $40 million to expand DeFi-as-a-service (link here)

NFT: From Ethereum to Solana and Back: Wormhole Lets You Send Your NFTs Across Blockchains (link here)

NFT: Andre Cronje’s New NFT Marketplace Is a Vampire Attack Suicide Pact (link here)

MACHINE LEARNING: Ocrolus lands $80M at a $500M+ valuation to automate document processing for fintechs and banks (link here)

MACHINE LEARNING: Artificial Intelligence in Financial Services 2.0 (link here)

Blueprint Updates

Analysis: Unlocking Demand-side growth with Square's payment network and Goldman's GreenSky acquisition (link here)

We answered the following question in the Long Take last week —

Why are fintechs moving up market to commerce and demand generation, and is that changing the structure of fintech competition?

Square upgraded Cash App into a payment processing powerhouse, completing the loop between the consumer and merchant side of the house. Goldman Sachs acquired GreenSky, adding a lending business at the point of intent. We need to connect these symptoms into a framework explaining the increasing integration between commerce and finance, and the increasing role that demand generation plays. That in turn explains how the attention and creator economies interconnect with financial services.

Podcast Conversation: What's next in Web3? Tachyon Accelerator's MD Gabriel Anderson on early stage in NFTs, DeFi, & Crypto (link here)

We tackled the following question in the podcast last week —

What's next in Web3?

")

In this conversation, we chat with Gabriel Anderson – Managing Director at Tachyon, Head of Market Strategy & Business Intelligence at ConsenSys Labs. Gabriel talks about the best projects he has seen so far that combine NFTs with other elements of DeFi and crypto, and what he’d like to see more of in the future.

We talk about the evolution of Web1.0 to Web 2.0 and finally Web3.0, and building and scaling communities in Web 3.0, and what makes them successful, along with the role of community managers. Gabriel shares some predictions about where the crypto space is headed.

“…the next piece in the stack with web3.0, crypto, crypto-economics is introducing internet money, native internet money. So, we went from these bland pages of information to these rich media and rich ecosystem experiences with web two. And now we're just layering in native internet money and money is just a mechanism, a means of transferring value and coordinating human beings. So, I mean, ultimately, I think where this is all going, and I don't know how down far into the rabbit hole we want to get here, but ultimately, we're going to enable all new coordination mechanisms because we'll have native internet incentive mechanisms.”

More? More!

If you want to go deeper in Fintech & DeFi, upgrade to a premium Blueprint subscription below. Our value prop is simple: experienced judgment, accurate vision. If you knew the shape of the tomorrow, what would you do today?

Want to chat? Stop by our (pretty empty right now until you join) Discord!

What did we miss? Reach out here anytime.