Wealthfront's $1 Billion of Cash in Two Months, plus 14 short takes on top developments

Hi Fintech futurists — I’ve missed you!

Hoping you are still enjoying Autonomous NEXT. I’ve got an itch to write though, and this newsletter will be my new weekly missive. I plan to relax a bit with the style, and take less of an industrial institutional investor approach. Check out a few editions, make sure to whitelist the email address, and stick around if you like it.

If you are not interested, and I am just bothering you with unwanted email — my sincere apologies, you can unsubscribe easily here or give me feedback here.

The latest short takes on the Fintech bundles, Crypto and Blockchain, Artificial Intelligence, and Augmented and Virtual Reality are below, and a longer take on how to make sense of a roboadvisor pretending to be a bank.

Long Take: Wealthfront's $1 Billion of Cash in Two Months

In news of cross-selling financial products across categories, roboadvisor Wealthfront has gathered a nifty $1 billion of deposit assets for its 2.29% interest-yielding non-bank cash account. Given that the firm has a little over $10 billion in managed investment assets, charges somewhere between 0 and 25 bps on those assets, and took years of wiggly pivoting to get to the current stage, it is fair to consider this influx a big win in terms of client traction. It is also $22 million of annual interest payments. A couple of things come to mind that are worth pulling apart.

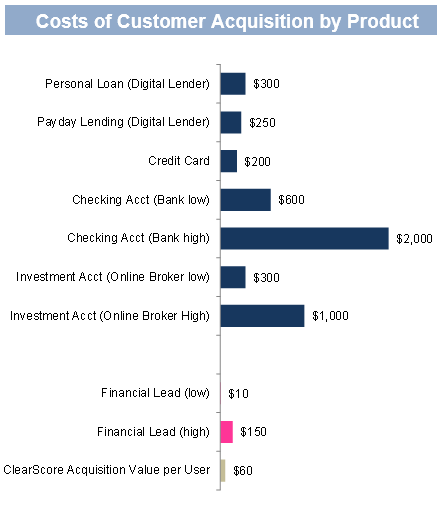

At a high level, the target market has expanded several times over. People are much more comfortable doing finance on their phones, instead of at a branch. Further, Wealthfront, and the rest of the roboadvisors, have developed brands that some people may at least recognize. That is better than coming out of nowhere. Third, the product itself is easier to sell than long-term wealth management. Getting a high interest rate on idle cash is a less risky proposition than delegating investments on your whole portfolio. I've also recently come across a report from mobile marketing platform company Liftoff, and there are some truly surprising stats about customer acquisition. Conversion is now way easier than in 2010.

You read that right. It costs $5-10 to get a person to install your app on their phone. Mobile is way better than a web app. For example, if you look at Google Ads, a click to your website will cost $5-20 depending on the search term (like "investment advice"). Then, once you get the prospect to your website, at best 5-10% will convert into trying the free product; and at worst than number is less than 1%. That leads to customer acquisition costs around $50 to $300, which is consistent with my findings at Autonomous NEXT.

If you look at American data and focus on activated financial product (rather than the installs), the cost is still around $50. User engagement and retention don't really matter, since you already have people's money and are likely earning fees or subscription. So yes, the market has shifted.

As a second large issue, it is worth asking whether the US is experiencing an online banking renaissance? The answer is "Yes". Much of the mobile banking revolution has been led by the Europeans -- see Revolut, Monzo, N26 and others. Those companies solved local pain points around FX to make people switch their secondary banking account to digital products. In the US, interest on cash is really the primary vector for competition, and it has been used by banks as a customer acquisition strategy for decades. In this case, online startups are venture funded and are open to taking losses on these accounts in order to acquire more customers -- see Chime, MoneyLion, and others. If anything, the question is why it took so long to launch the thing at all!

So what could the economics around this product look like, and who really wins? If you are a bank, deposits are a profitable arbitrage since you make more in interest through your lending activities than the cost of borrowing. The Federal Reserve rate is 2.50%, so anything less than this amount is a great deal for any bank. Such a bank may lend out at 5.00%, have cost of capital of 3.00%, and make 200 basis points. An investment advisor would kill to make 200 basis points on assets under management. True, a bank's loan book might blow up and hurt their returns, but that's when the government bails you out!

I do not know if Wealthfront is making or losing money on this product. One thought experiment is that at $1 billion in deposits, they gain 1 million of $1,000 accounts. Let's assume that 50% of that is net new (i.e., 500k accounts), and that they literally just pay out $20 million per year out of pocket, and thereafter the cross-sell into wealth management pays for itself. This would imply a $40 customer acquisition cost, which is spectacular! Or better yet, as some commentators imply, Wealthfront could be making money from this product -- getting about 20-50 basis points from the banks at which these deposits actually sit. An additional $2-5 million of revenue from 2 months of lead generation ain't bad either.

How is the sausage made? Wealthfront itself cannot offer a bank account, because it is an investment entity without a banking license. It is regulated by the SEC, is a broker/dealer, and a Registered Investment Advisor. Banks are regulated by the OCC and are State registered. In fact, there's been a ton of controversy about the Fintech OCC charter, with States resisting federal authority, and companies like SoFi and Square considering the more exotic Industrial Loan Company charter. If Wealthfront just bought a bank, then it would be a bank holding company, subject to capital rules as well. This stuff is important -- how can they offer the cash account?

The short answer is a theme called "bank-as-a-service", related to "Open Banking" in Europe, where deposit accounts and payment products are rented out to channel partners by banking entities. Holding an omnibus account on behalf of a client, sometimes through an intermediary, is essentially a work-around that everyone from Apple to T-Mobile is using. But this is the current vogue in Fintech. Companies like Total Banking Solutions, SynapseFi, Cambr, Mambu and others are offering everything from core banking systems (e.g., Fiserv and FIS) to actual bank accounts for rent. Capital is being separated from distribution.

What Wealthfront has shown is the importance of channels, and the power of a mobile-first solution. While most roboadvisors pivoted into helping financial incumbents make their advisors more efficient, Wealthfront stuck with its "technology-first" B2C approach. In this case, it worked. Adding a simple, easy-to-understand product and hiding the regulatory complexity behind the curtain using modern third-party banking solutions is the way that all these companies should fight for consumer attention and money. Remember, there is no difference between a bank, brokerage, and retirement account for a regular human being. These are arbitrarily defined products, with dividing lines slowly being erased by code.

Short Takes

Allianz Invests in Structured Products Platform Halo. I like this -- structured investment products have not see the revolution in "democratization" that simpler products have, and probably for good reason. But apps like this are a first step. Intersects with tokenization.

Paris based financial data aggregator Bankin raises EUR 20 million. I don't understand why these things are still getting funded, when Mint did it in 2007. But hey, I don't have 3 million users across Europe!

PayPal Eyes Credit To Monetize Venmo. Money movement company to add underwriting, creating fintech bundle. Yep!

Tether's Dubious $850 Million and NY Lawsuit. Some clarity after years of bad information about what's actually backing USDT. Apparently the money was there, until it wasn't, in part because there were no good banks to back crypto companies.

Digital Investment Bank wevest Goes with Stellar Blockchain for Security Tokens. Not that this particular bank matters, but some folks do pick Stellar. Remember than Stellar "bought" Chain a little bit back too.

Gaming Firm Unitopia Raises $5 Million to Create Blockchain Equivalent of Steam. What's interesting here is whether tokens are best used to convey ownership of virtual items, digital real estate, or ownership of the license to play the game. Each type of these approaches have launched.

JPMorgan Expanding Blockchain Project With 220 Banks to Include Payments. Forked off Ethereum and built to defend against Ripple, JPM and its coin seem to be in the copy-and-take-credit game.

Pople's Bank of China to launch the second-generation credit rating system. To quote: "Compared with the first-generation, the second-generation credit rating system covers more information that is not recorded before, including revolving loans, large-sum specialist installments for credit cards, joint-borrowers, companies providing guarantees to individual persons, individual persons providing guarantees to companies, and late repayment information."

Three Ways To Leverage AI And Keep Pace With The Future Of Digital Marketing. A fair intro into the way AI is changing the storefronts of finance.

The Best Chatbot Apps in 2019 — Top 20 Chatbot Apps powered by AI. What I love about this list is how many of the illustrations reference full-blown apps, but the chatbots are the connection that pulls those apps into channels like Telegram.

Alibaba already has a voice assistant way better than Google’s. Apparently Jamie Dimon was humbled by his visit to Ant Financial. Western tech should be humbled by the scale of data and talent the Eastern tech giant can leverage.

Kangaroo, the New York-based provider of smart home products, announced a $10.26m funding round led by Greycroft. Super affordable home monitoring with cheap sensors. Better data has a direct connection to insurance product. Who has the data?

VR’s True Innovation Isn’t Technological, It’s Human. The tech is getting good enough that immersion is strong, and real. To whom in finance will these things connect? Avatars or other Humans?

Uber’s Advanced Technologies Group Raises $1 Billion. Toyota, Softank and DENSO are funding this Uber effort to develop self-driving ride-sharing technology. Think about who provides the insurance and to whom.

Looking for more?

Fully updated website here, and LinkedIn over here.

Find me on Twitter here for Fintech and here for Digital Art.

Want to send me a note? Reach out here anytime.