Analysis: Mastercard Buys BVNK for $1.8B as Stripe Launches Machine Payments Protocol

Are you tired of AI robots winning yet?

Gm Fintech Architects —

Today we are diving into the following topics:

Summary: We examine Mastercard’s $1.8B acquisition of BVNK, Stripe’s launch of the Machine Payments Protocol (MPP), and Visa’s push into command-line commerce. Mastercard’s move secures stablecoin orchestration infrastructure handling $30B in volume, positioning it against a future where even 5% of its $9T+ payment flows migrate on-chain. Stripe, meanwhile, is embedding itself at the protocol layer with MPP, enabling agent-native transactions across fiat and crypto rails via simple APIs, potentially owning the metering layer of AI-driven commerce. These developments reflect a broader rewrite of the financial stack, from fiat-to-crypto bridges to programmable, agent-driven payments, where infrastructure players race to control the flow of machine-native transactions. Ultimately, finance is not leading this shift but following it, as AI-driven economic activity reshapes how value is created, moved, and monetized.

Topics: Mastercard, BVNK, Stripe, Visa, Tempo, Google, Coinbase, Morgan Stanley, ZeroHash, Bridge, m0, Rain, LayerZero, Lightspark, Nevermined, Don Gossen, Browserbase, PostalForm, Polygon, Binance

To support this writing and access our full archive of newsletters, analyses, and guides to building in the Fintech & DeFi industries, see subscription options below.

🤖🏦🧭 Our Ecosystem:

Generative Ventures | AI Research | Robot Money | Linkedin & Twitter | Sponsors

Long Take

Too Much Agentic Finance

You must be tired of all this AI finance everywhere. Press releases and announcements are going nuts this week! We just wrote about Ramp and Stripe earlier in the week, and now there’s no choice but to write on this again.

The following in particular stick out as important:

What you are seeing is a consequence of a big change upstream in the mountain. A boulder has moved, unblocking the flow of water down into the rivers. We sit by the rivers, watching debris flow by.

That change is AI as an economic actor. That’s all. Finance follows.

About five years ago, we would have been writing about Crypto and DeFi all the time.

Readers would get frustrated and say, “Why is this Fintech newsletter all about tokens”? And the reason was that blockchains unblocked a giant boulder in the mountain called “digital asset scarcity”. Therefore, the most important thing going on was the consequences of this.

In 2010-2015, we would have been talking about mobile apps and websites that now house financial products: neobanks, roboadvisors, and payments processors. Why? Because the boulder in the mountain was the Internet itself, cloud-based software, and the change in consumer behavior as smartphones became ubiquitous.

Change starts upstream and flows down. This is why we highlight financial AI rails again today. So let’s get into it.

Mastercard and BVNK

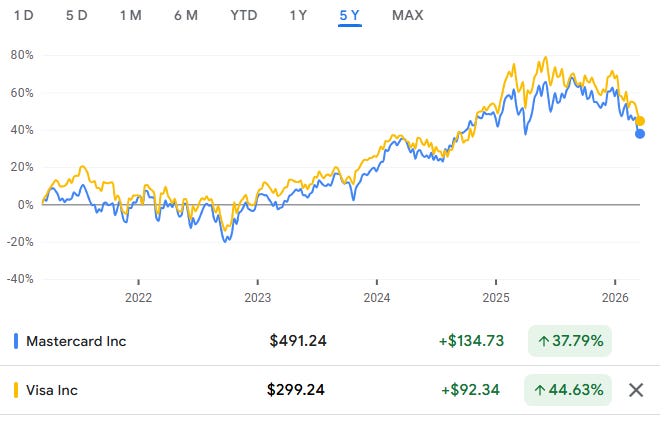

Mastercard is working hard to match Visa's public perception around stablecoins and crypto. Both payment networks have been battling it out to remain the aggregator of aggregators. From a performance perspective, the companies are neck and neck, effectively representing the entire market for payments:

The firm was set to acquire ZeroHash last year — a core crypto infrastructure provider — but the target decided to go independent and raise $250MM at a $1.5B valuation instead alongside Morgan Stanley.

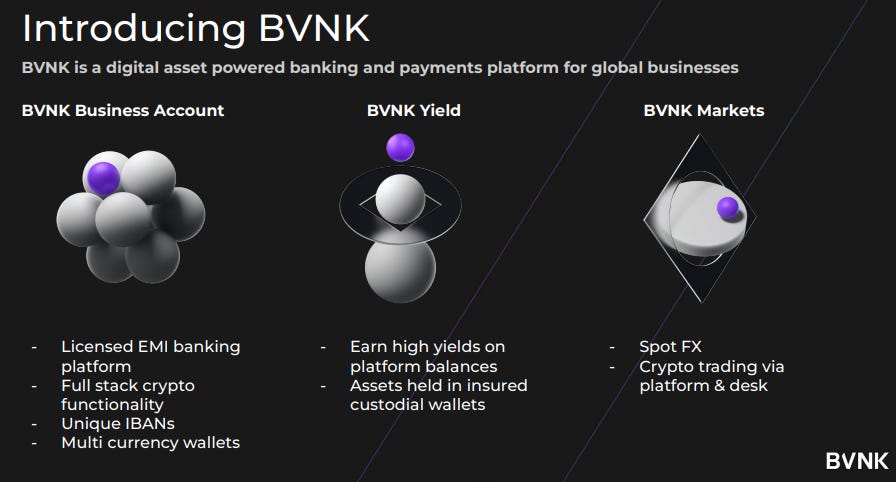

At the same time, BVNK was in talks with Coinbase to be acquired for $2B, but the deal fell apart. Now, Mastercard will buy BVNK for up to $1.8B, including $300 million in contingent payments tied to performance metrics.

The last known private valuation for BVNK was around $750 million, so Mastercard paid roughly 2.4x the last private round valuation at the top end. The firm generated $30 billion of transaction volume and, at a take rate of around 10-40 bps, would earn $50-150MM of annualized revenue, implying anywhere between a 15-50x revenue multiple.

The strategic fit is obvious — all payment rails need stablecoin infrastructure.

To deepen the strategic takeaway, we highlight in full and with permission, the opinion on the transaction from Luca Prosperi, founder and CEO of m0, the innovative first mover in institutional stablecoin issuance infrastructure. As disclosure, Lex is an angel investor in m0.

Mastercard just paid $1.8B for BVNK — estimated 45x annualized revenue. The largest stablecoin acquisition in history. I don't care about the pricing personally. I care about what this means.

Following Stripe's acquisition of Bridge a little over a year ago, this is the second major acquisition NOT of a stablecoin issuer, but of a so-called orchestrator. A company that moves tokens, not one that manufactures them. I have argued for years that stablecoins (terrible name) are pieces of infrastructure, not payment products. Infrastructure — the kind that rewires how money is created, moved, and settled at the system level.

BVNK's infrastructure focuses on the translation layer between legacy finance / fiat and on-chain rails: $30B in volume, 25+ licenses, 370+ enterprise clients. It's in this messy, fragmented connector layer that vast yet dispersed profit centers exist. And you know — your margin is somebody else's opportunity.

Analysts have been looking at revenue and revenue multiples for this transaction, but I think this is misleading. True, BVNK's blended take rate on the flows they intermediate is c. 13 bps. But that number hides three very different businesses. FX-premium corridors (NGN, ARS, KES) at 50-150 bps, dollar-to-dollar on/off-ramp at 5-15 bps, stable-to-stable orchestration at 1-5 bps.

The reason why the revenue multiple is irrelevant is that most probably the business footprint will change dramatically over the next few years, with new players eating into the lucrative FX weekend premium in EMs, and more volume moving into the on-chain-to-on-chain corridor where a multitude of different tokens, applications, and computing/ consensus environments will emerge. More environments means more connectors.

Mastercard processes $9T+ a year. If even 5% of those volumes migrates to novel rails this decade — and it will — they need to own that pipe or get routed through someone else's. At least part of the $1.8B is (cheap) insurance against irrelevance in the fastest-growing settlement layer in finance.

Digital value settlement is no longer the purview of crypto-native niche projects. First came the two major issuers building their own messaging and acceptance networks, then the mobile checkout giants, now the card networks. Alongside those a new crop of digital money infrastructure company like BVNK, Bridge (focusing on fiat translation), Rain (building around core card competences), Layer Zero (extending their reach from messaging products), and M0 (starting from on-chain issuance expertise).

It's all part of the same thing: efficient value representation and value movement. Every year, a new piece of the puzzle gets connected. Fiat-to-fiat, crypto-to-card, blockchain-to-blockchain. The money creation and money movement layers are blurring. Next comes money programmability. Then the application layer. The financial stack has been rewritten under our eyes.

That takeaway is as good as it gets.

Stripe, Visa, and the Machine Payments Protocol

In the same week, Stripe and Visa both announced products and protocols aimed at AI agent payments. Stripe’s Machine Payments Protocol stole the spotlight from the associated announcement that Tempo, Stripe’s proprietary EVM payments chain, is live as well.