Analysis: The Fintech Blueprint AI & Robotics Report Q1 2026

This 121 page report maps 95 companies across AI infrastructure, foundation models, robotics, agents, and decentralized networks

Gm Fintech Architects —

Today we are excited to launch the latest update to our AI & Robotics Encyclopedia.

")

This 121 page report maps 95 companies across AI infrastructure, foundation models, robotics, agents, and decentralized networks, with quarterly financial tracking from industrial foundations through end-state machine coordination. A material update on our initiation report last year.

Today’s Long Take will highlight the primary takeaways from the research.

For Premium subscribers, we will provide a download link at the bottom of this article. For Free subscribers, don’t hesitate to upgrade at around $100/year to access the report, or grab it here for a one time $149 price.

We look at Public equities, private companies, and protocol tokens, each analyzed through platform economics, competitive positioning, and financial fundamentals. Here are the key categories:

PUBLIC (~40 companies) NVIDIA, CoreWeave, Alphabet, Palantir, Oracle, Snowflake, Adobe, Shopify, Salesforce, Coinbase, Baidu, Alibaba, Tencent, and more. Infrastructure outperforms application in the SaaSpocalypse, while Chinese AI re-rates on DeepSeek momentum.

PRIVATE (~30 companies) OpenAI, Anthropic, Mistral, Scale AI, Databricks, Figure AI, Anduril, Harvey, Cognition, Hugging Face. The humanoid eruption, revenue traction vs. platform bets, and the IPO pipeline.

TOKEN (~25 protocols) TAO, NEAR, ETH, SOL, HNT, RENDER, GRT, FET, FIL, and more. The value capture paradox deepens, Ethereum’s settlement thesis tested by L2 margin extraction, DePIN economics remain broken, governance fragility persists.

It’s a massive piece of work, and gives a full value chain walk through of the machine economy and where things are growing, and where they are shrinking.

But before we dive in, an aside on Anthropic SPVs, and private market fragility.

The SPV Market

Before we dive into the meat of today’s newsletter, I want to point out an extremely important indicator for everyone to watch. The global economy is pinned to the AI narrative, and the AI narrative is pinned to continued investment, which is all resting on the availability of capital and belief in the future.

In turn, those two things hang on:

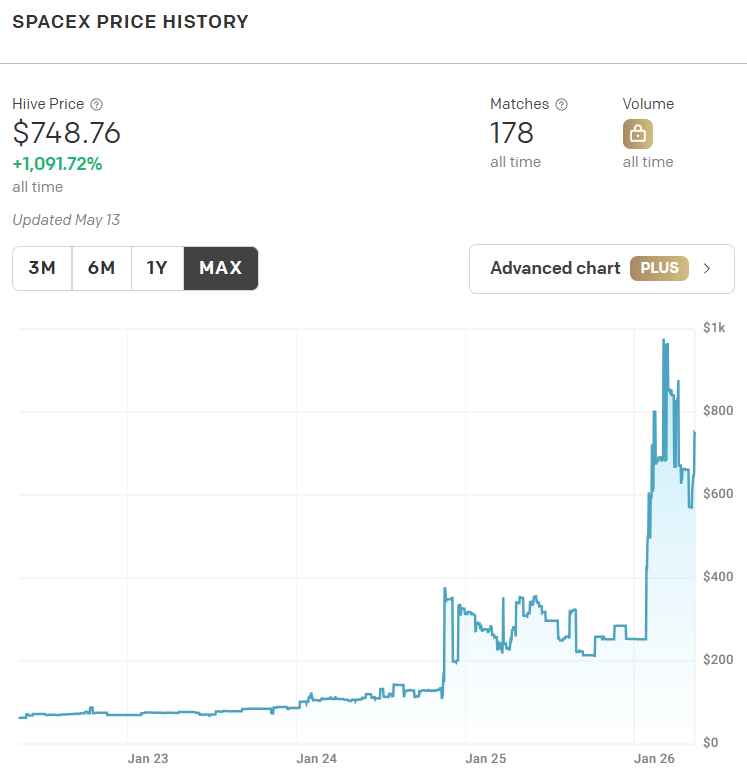

SpaceX IPO performance, hitting $1.5-2 trillion in marketcap

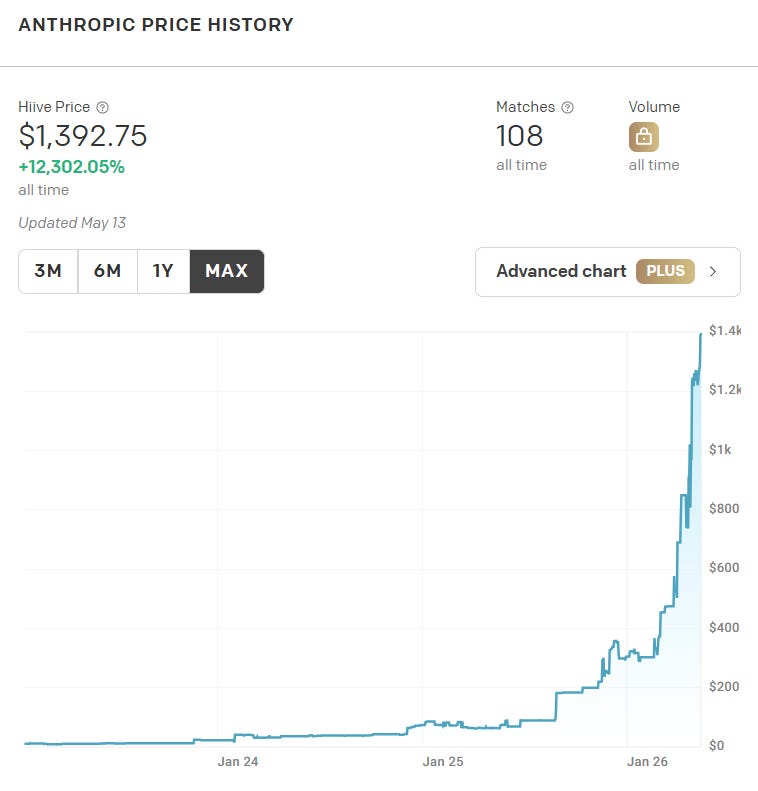

Anthropic SPV secondary markets, currently floating around $1 trillion in valuation on $30B of ARR

If these two things fall apart, we are likely to see a massive risk-off unwind, with downstream implications of hundreds of billions in GPU-backed debt at Blackstone, institutional and sovereign exposure to AI Labs equity, and the overall health of the private markets.

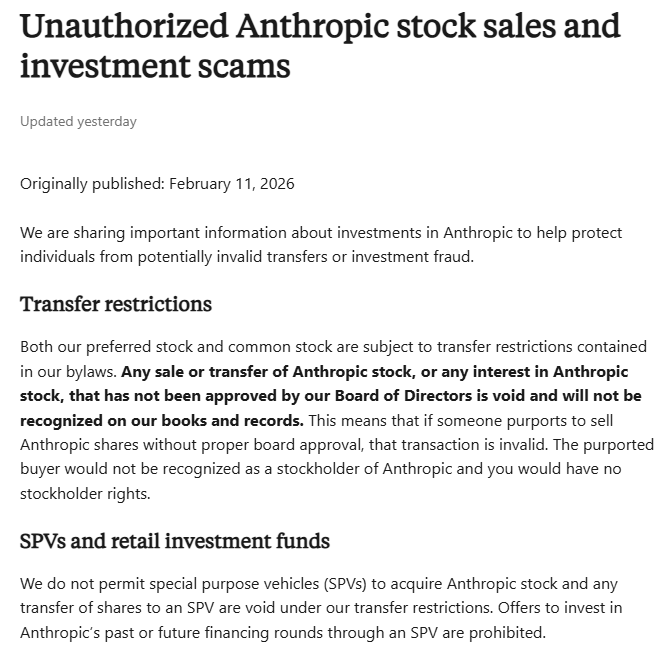

In recent days, Anthropic SPV fever hit its highest temperature and the firm responded with a legal disclaimer suggesting that all SPV-related trading is effectively illegal unless authorized explicitly by the Board of Directors.

The Anthropic transfer-restriction notice reads like a rug pull to anyone invested in these deals.

Gabriel Shapiro, the attorney who flagged it, points at the operative word: “void.” Voidable transfers can be ratified in Delaware; void transfers, in theory, never existed. Equitable defenses collapse, original sellers can keep the cash and the shares, and chains of secondary trades become transactions that never happened on the books.

That’s the nuclear option.

Thomas Braziel of 117 Partners thinks the courts will not buy Anthropic’s position. The SPV ecosystem did not appear overnight; it developed in public, with platforms, prices, and a steady flow of internal emails at every issuer that watched and chose not to enforce. The company let a shadow SPV market run in public for years and protested only after valuations crossed a trillion. The deeper problem is regulatory arbitrage around Section 12(g): private companies hold holders-of-record counts low to avoid public-company disclosure while letting public-company-scale capital trade through SPVs.

Hari Raghavan, who has spent a decade inside these deals, supplies the mechanics that explain both readings. No fund can lead a $10 billion check off its balance sheet, never mind $50 billion, so capital has to come from family offices, RIAs, and endowments — through SPVs. Banning SPVs while raising back-to-back $13B / $40B / $50B rounds asks the market to do something the math will not allow. The bulletin is a primary-round problem dressed up as a secondary-market one. The word “secondary” never appears in it.

So is this the apocalypse? According to the derivatives trading at Hyperliquid, it’s a mere blip in the story.

Long Take: Three Machines, One Quarter

Q1 2026 Machine Economy Update

Who is winning the AI race?