Analysis: Why Agentic Finance is not the Metaverse all over again

Meta shut down metaverse Horizon efforts after $84B in losses, while agentic systems plug into $10B monthly spend and $1.9T of commerce

Gm Fintech Architects —

Today we are diving into the following topics:

Summary: We discuss the divergence between failed “build it and they will come” technology bets like Meta’s metaverse, with $83.6B in cumulative losses and only a few hundred thousand users, and the rapid rise of agentic finance, which builds on existing economic activity. We show that unlike the metaverse, agentic systems are embedded into real workflows, with Ramp processing $10B+ in monthly spend and making 26MM autonomous decisions, and Stripe handling $1.9T in payments while enabling AI-native commerce. We map the emerging full stack of agentic finance, from protocols (ACP, UCP, MPP) to identity (KYA, Visa TAP) and settlement layers like Tempo, highlighting coordinated industry adoption.

Topics: Ramp, Stripe, Visa, Mastercard, Meta, Horizon Worlds, Tempo, Agentic Commerce Protocol, Agentic Commerce Suite, OpenAI, Anthropic, Google, Coinbase, FIS, PayPal, Etsy, URBN, Wix, Squarespace, BigCommerce, Bridge, Microsoft Copilot, ChatGPT, Block, Roblox, Skyfire, Mirakl, commercetools

To support this writing and access our full archive of newsletters, analyses, and guides to building in the Fintech & DeFi industries, see subscription options below.

🤖🏦🧭 Our Ecosystem:

Generative Ventures | AI Research | Robot Money | Linkedin & Twitter | Sponsors

Long Take

Ghost Towns and Gold Rushes

In October 2021, Mark Zuckerberg walked onto a stage and told the world that the future was a place called the metaverse. He renamed his company after it and would spend tens of billions building it. He predicted a billion users within a decade and hundreds of billions in virtual commerce.

And we believed him.

Last month, Meta shut down Horizon Worlds on Quest headsets.

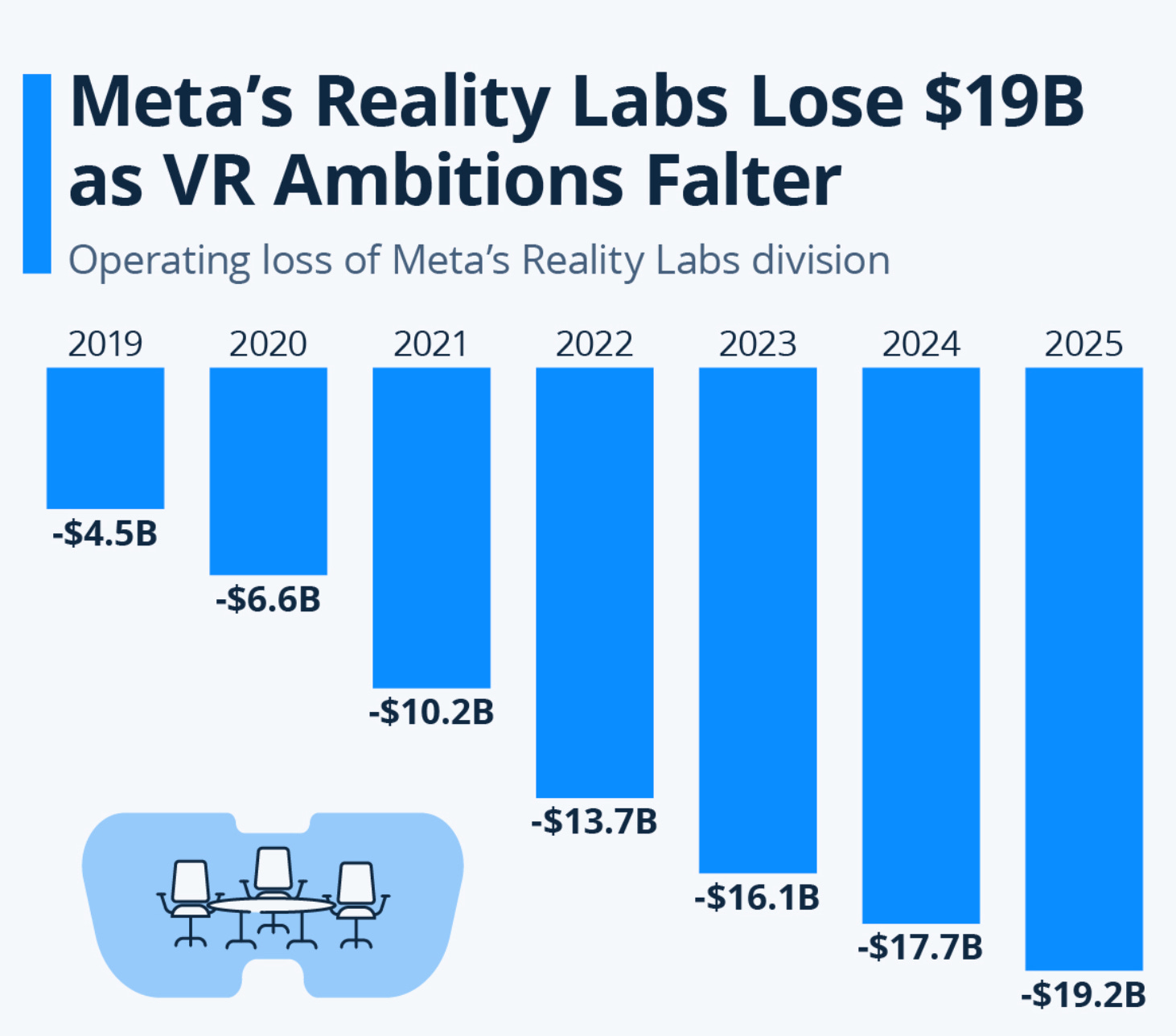

The VR social network that was supposed to justify the company’s new name is being pulled from the Quest store by March 31 and fully removed from VR by June 15. Reality Labs has accumulated over $83.6B in cumulative operating losses since 2020, posting $6.02B in losses in Q4 2025 alone on approximately $955MM in revenue.

The losses have increased every single year: $6.62B in 2020, $10.19B in 2021, $13.71B in 2022, $16.12B in 2023, $17.72B in 2024, and $19.19B in 2025. Over 2,000 Reality Labs employees have been laid off since January. The fitness app Supernatural, acquired for $400MM in 2021, has stopped producing new content and has been wound down.

Horizon Worlds never drew more than a few hundred thousand monthly active users. Roblox, the platform Meta repositioned Horizon to compete with, has more than 150 million daily users without requiring any hardware at all.

The metaverse concept died because user adoption never caught up with the vision. People did not enjoy putting on heavy headsets and staring into nausea-inducing lightbulbs.

But is the story repeating?

Meta now guides for $115B to $135B in 2026 capital expenditure, nearly double the $72B it spent in 2025, with the vast majority directed at AI infrastructure, data centers, and chips. Zuckerberg described 2026 as the year of “advancing personal superintelligence.”

Technology leaders often look out at the horizon, see a plausible future, and then try to brute-force consumer behavior toward it. Sometimes it works. Most of the time, they are building a beautiful hallucination in the desert and waiting for people to show up.

The metaverse was an “if we build it, they will come” bet. It required everyone to strap a computer to their face, create an avatar, and decide that virtual meetings were better than Zoom. It needed many of us to learn what an NFT is, and figure out which digital goods to buy and sell.

This all means getting people to change how they live and what they consume.

Now compare this to what Ramp and Stripe have been building, and what Visa, Mastercard, Google, PayPal, and FIS are all coordinating around at the same time.

Agents are doing the work on behalf of humans, inside systems humans already use. The economic activity already exists. The money is already moving. The agents are just moving it faster, cheaper, and with fewer clicks.

This is the difference between a ghost town and a gold rush.

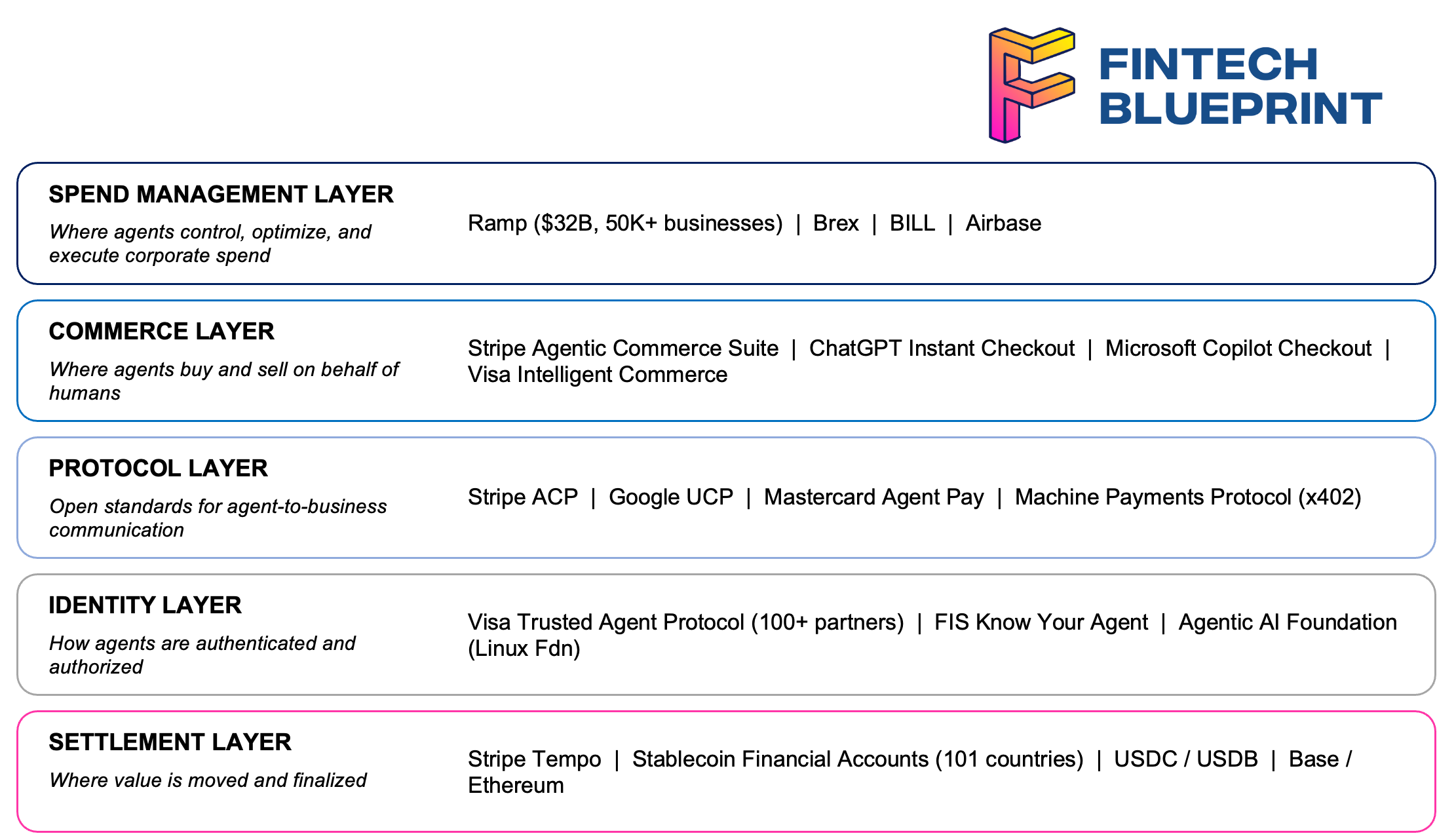

The Full Agentic Finance Stack

What is happening is an industry-wide coordinated buildout of agent financial infrastructure.

Let’s map a few key elements below:

Protocol Layer:

Stripe ACP (open standard, launched Sept 2025 with OpenAI)

Google Universal Commerce Protocol (UCP, launched NRF Jan 2026)

Visa Trusted Agent Protocol (100+ partners, 30+ in sandbox, 20+ agents integrating)

Mastercard Agent Pay (expanding internationally, now live in Hong Kong)

Machine Payments Protocol (x402, for machine-to-machine transactions)

Commerce Layer:

Stripe Agentic Commerce Suite (Etsy, URBN, Coach, Wix, BigCommerce, etc.)

ChatGPT Instant Checkout (powered by Stripe)

Microsoft Copilot Checkout (powered by Stripe)

FIS launched the first offering for banks to conduct commerce with AI agents (January 2026), introducing “Know Your Agent” (KYA) protocols

Spend Management Layer:

Ramp (50,000+ businesses, $1B+ ARR, $32B valuation, Visa integration)

Brex, BILL, and Airbase are in the same competitive space but have not yet demonstrated equivalent agentic capabilities

Settlement Layer:

Stripe Tempo (EVM-based, $500MM seed, Paradigm-backed)

Stablecoin Financial Accounts (Stripe, 101 countries, USDC + USDB)

Identity Layer:

Visa Trusted Agent Protocol

FIS Know Your Agent (KYA)

Agentic AI Foundation (OpenAI, Anthropic, Block, under Linux Foundation)

This is a coordinated infrastructure industry transformation, like the rollout of chip-and-PIN or mobile wallets, but on a much faster timeline

Visa’s research indicates 47% of US shoppers already use AI tools for at least one shopping task. BCG reports 81% of consumers expect to use agentic AI. Visa’s SVP Rubail Birwadker stated plainly that “in 2026, AI agents won’t just assist your shopping, they will complete your purchases”.

While most consumers are not demanding AI financial services, they are massively adopting AI tools in a way that people simply never did with virtual reality headsets.

There are 900 million people using OpenAI tools, and hundreds of millions more engaging with Google Gemini and Anthropic Claude. The market is expanding from labor productivity growth and the resulting economic activity, rather than assuming people want to have digital leisure third spaces.

As a result, large-scale digital finance incumbents have started to react.

Ramp: The Autonomous CFO

Ramp has led the way in adopting an AI-native approach to building its business. Even prior, its progress had been one of the most impressive fintech stories of the decade.