Analysis: Stripe bids $53B for PayPal; and the DeFi Post-Mortem

A funeral, a simulation, and the Phoenix

Gm Fintech Architects —

Let me vent please.

I don’t believe all that I write today, but I have to say it anyway. One year, it’s a post celebrating BTC at $100K. A poem to bubbles!

Another year, everything is dead.

Are we not tired of the songs, constantly changing their tune? I don’t know the truth, but I know I have to sing them.

Today we are diving into the following topics:

Stripe, PayPal, and Digital Commerce: We examine reports that Stripe, Advent International, and other investors are pursuing a $53B take-private acquisition of PayPal, highlighting the changing economics of digital payments. We compare Stripe, PayPal, Visa, Mastercard, and Adyen, arguing that payment networks continue to compound value through their dominant position in the transaction stack while payment processors increasingly compete on growth and execution.

The DeFi Post-Mortem: We revisit the original promise of decentralized finance and ask why a movement that aimed to rebuild global financial infrastructure has struggled to achieve mainstream adoption. We argue that DeFi’s contraction from roughly $180B to $80B reflects structural issues—including poor incentives, weak governance, hacks, and speculation—rather than a failure of programmable finance itself.

Topics: Stripe, PayPal, Advent International, Block, Visa, Mastercard, Adyen, Tempo, Venmo, Braintree, Google Pay, Apple Pay, Tether, Circle, Ethereum, Ant Financial, Set Protocol, Yearn, Aave, Compound, Bitcoin, Zapper, Zerion, Axie Infinity, Base, Solana, Pump.fun, Robinhood, Kelsier Ventures, Binance, BitGet, Hyperliquid

Thanks as always for your time and attention,

Lex

To support this writing and access our full archive of newsletters, analyses, and guides to building in the Fintech & DeFi industries, see subscription options below.

🤖🏦🧭 Our Ecosystem:

Generative Ventures | AI Research | Robot Money | Linkedin & Twitter | Sponsors

🚀 Lex is actively meeting teams building machine-native financial companies. If that’s you, reach out here.

🤖 AI & Robotics Industry Encyclopedia: In this 100+ page report, we collate all the meaningful companies across public quities, private equity, and digital assets related to the machine economy. 👉Learn more here

🦄 In partnership with InterPrivate, we just launched a $200MM SPAC looking for targets in fintech, digital assets, and AI infrastructure. If you are a late-stage founder or have an idea to discuss, reply directly to this email.

Stripe, Paypal, and Digital Commerce

We are going to do this as a quick hit.

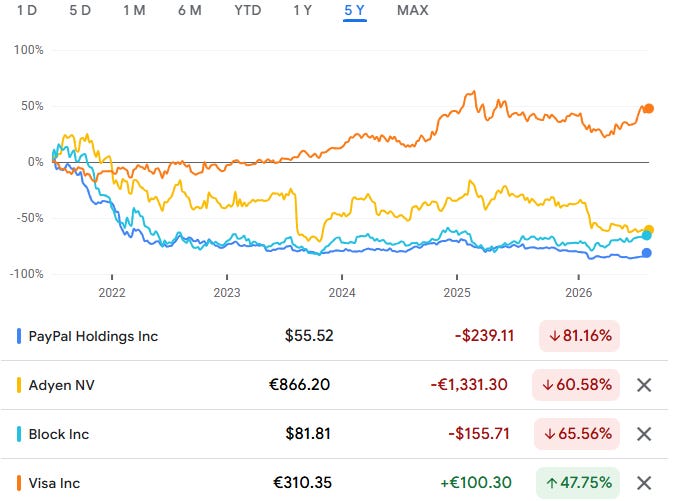

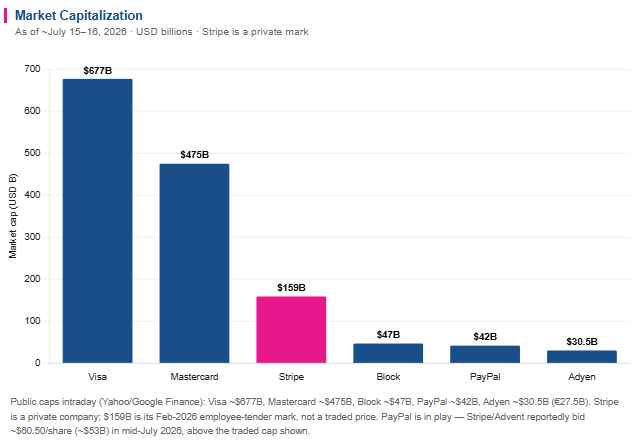

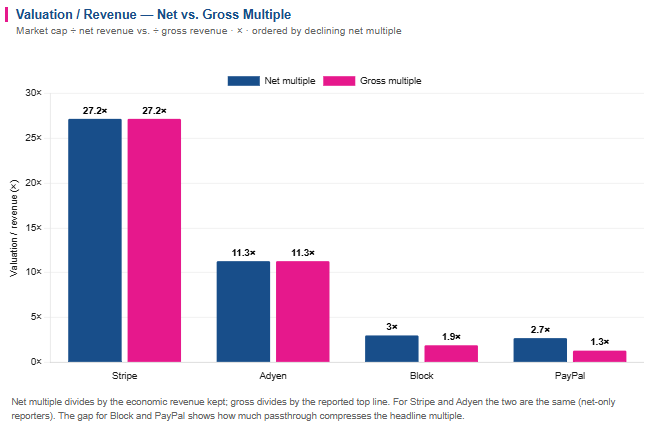

Payments giant Stripe and private equity firm Advent International, as well as some other potential participants like Block, are making a bid to take PayPal private. PayPal is a $50B public company, which is a far cry from its $360B heyday. For comparison, the card networks, Mastercard and Visa, are both around $500B in market capitalization. Adyen, a Stripe competitor, floats around $35B.

It can be hard to be public. Stripe gets to enjoy its $160B private valuation and a much less critical venture capital investor.

The idea is that a consortium of Stripe and Advent will put together a buy-out package for PayPal’s entire public marketcap with a small premium — about $17B of equity and $36B of debt and other funding, for a total of $53B. It’s unclear why Stripe doesn’t just acquire the company outright, but maybe there are monopoly concerns around such a consolidation. The entity would be run separately, but obviously would be jointly owned. This is a similar playbook to Tempo, as a separate but controlled subsidiary of Stripe, targeting the retail consumer and taking out one of the smaller competitors (Venmo/Braintree legacy).

The numbers are ... pretty hilarious?

Stripe is dwarfed only by Visa and Mastercard. If you look at 5-year stock performance, you can also see that only the card networks retained value while the rest of the payment processing stack bled out.

Why you ask? Because they have very different positions in the value chain.

The networks have full market penetration in a duopoly, and are thus invoked whenever anything new happens anywhere with payments. The only exception is crypto. So whether it’s PayPal, Stripe, or Adyen does not matter to Visa and Mastercard. They grow regardless and therefore are immune to market share fights of the orchestrators above them.

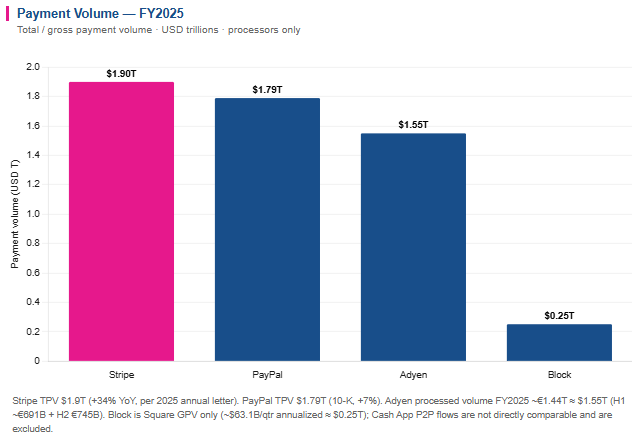

So downstream you have Stripe, PayPal and Adyen with similar-ish $1.5T-$2T volumes, but the rate of change and growth is very different. PayPal is run by professional managers, and its genius cohort — Elon Musk and Peter Thiel — has obviously moved on to run the world and launch space rockets instead.

Stripe, on the other hand, still runs on founder mana and will outperform professional managers any day of the week.

Let’s look at the companies based on high-level fundamentals.

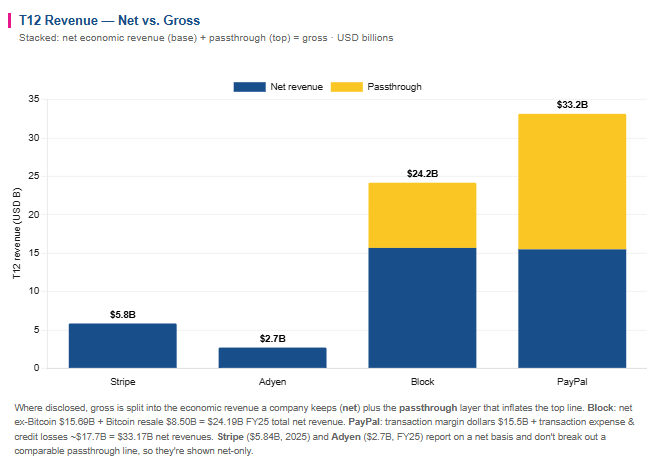

From a revenue perspective, PayPal is the bigger company — $33B in gross revenue, of which $15B is net. But it trades at a 1.2x gross revenue multiple, because it has struggled to grow and is instead being chipped away at by various competitors, from Stripe, to the impenetrable Google Pay and ApplePay. Once a hyperscaler eats a feature, good luck retaining independent market share. And all the payment processing startups that target checkout are effectively eating PayPal’s lunch.

Whereas Stripe continues to grow, and with its $6B of revenue, it gets to trade at 27x revenue, nearly 3 times more than its public counterpart Adyen. This whole thing is a multiples game, and multiples are a derivative of cost of capital, which is dependent on growth assumptions.

It is unclear whether PayPal can do better, but this is not a particularly great outcome.

Maybe Tether and Circle can create a consortium and buy it out for $100B and stuff it full of stablecoins and DeFi lending protocols — this is the only path to the next stage in my view. But thar be dragons too.

Long Take: The DeFi Post-Mortem

I came to this industry as a robo advisor founder watching neobanks, and the conclusion was simple: you cannot build the all-in-one fintech app without a complete refresh of financial infrastructure.

The amount of scotch tape needed to glue together core banking systems to front-ends is just too high.

China had done it — Ant Financial was the first example of a real financial super app — and meanwhile, our own Fintechs were narrow and verticalized.

So seeing financial applications on Ethereum was a breath of fresh air. We suddenly had something modern on which to build programmable money.

Then DeFi summer happened, and the dream became clear.