Analysis: Architect and the $11 Trillion AI Capital Markets

The next frontier in AI may not be better models, but better financial markets for compute

Gm Fintech Architects —

Today we are diving into the following topics:

Summary: We examine the emergence of capital markets built specifically for AI infrastructure rather than AI applications, arguing that GPUs, compute capacity, and inference have become financial assets in their own right. We discuss how an estimated $11T will be invested in AI infrastructure between 2024 and 2029, including roughly $7T financed by debt, creating demand for hedging, derivatives, and new financial markets. We highlight Architect’s launch of ComputeConnect, a regulated exchange linking GPU derivatives with physical compute delivery, as an example of crypto-native market structures expanding into AI infrastructure. Financial markets around AI infrastructure could become as important as the AI applications themselves by bringing price discovery, liquidity, and risk management to the largest technology investment cycle in history.

Topics: Architect, Compute Index, ComputeConnect, NVIDIA, CoreWeave, Blackstone, Oracle, SpaceX, Meta, Hyperliquid, Anthropic, OpenAI, Ornn, Andreessen Horowitz, Brett Harrison.

To support this writing and access our full archive of newsletters, analyses, and guides to building in the Fintech & DeFi industries, see subscription options below.

🤖🏦🧭 Our Ecosystem:

Generative Ventures | AI Research | Robot Money | Linkedin & Twitter | Sponsors

🚀 Lex is actively meeting teams building machine-native financial companies. If that’s you, reach out here.

🤖 AI & Robotics Industry Encyclopedia: In this 100+ page report, we collate all the meaningful companies across public quities, private equity, and digital assets related to the machine economy. 👉Learn more here

🦄 In partnership with InterPrivate, we just launched a $200MM SPAC looking for targets in fintech, digital assets, and AI infrastructure. If you are a late-stage founder or have an idea to discuss, reply directly to this email.

Long Take

AI for Finance or Finance for AI

There are many intersections between AI and financial services.

One easy way to segment the categorization is to think about (1) AI that lives within financial services as a business or a function, and (2) finance that works at the behest and is custom-built for AI.

In Category 1, the examples are pedestrian and well-known by now — adding AI into underwriting, deploying OCR on documents, integrating larger models to prevent fraud, extending customer service.

Much more is going on in getting AI to do the business of running a financial company, such as organizing workflow or writing code. We talk about this as financial harnesses, meaning a chassis by which LLMs can be your colleagues in the finance profession. This is more akin to being a functional contributor inside of an organization, than about some sub-process of a manufacturing process.

In Category 2, we look to add financial features to an AI-first world. One of these has been commerce and payments infrastructure for agents. Whether or not this category is able to hold water is yet to be determined. However, the combination of stablecoins on various chains, payment processors, and commerce enablers has chased down the potential blue ocean with abandon. Even the large tech companies have shipped various agentic identity protocols to bootstrap our imagination.

It all feels a bit ahead of demand.

One area we haven’t spent as much time on, but is equally large, is the effect of AI on capital markets. And I don’t mean how good an AI agent is at arbing this or that — such a product is squarely in category 1. From the venture side, I have seen dozens of companies building AI-first roboadvisors, neobanks, and neobrokers and calling them by cooler names. That’s not what I mean.

Rather, AI needs capital markets for its own assets.

In the past, we wrote about this as a warning. In particular, we amplified the story that:

There’s huge spend on GPUs to train models and provide inference

Many people think that will never be profitable

It’s true, validated by our machine economy research, that money is concentrating in components, chips, datacenters and applications are not yet catching up

To fight each other, hyperscalers have spent down all their cash and raised debt

That debt is circular between NVIDIA and its customers

Companies are staying private longer to avoid public market scrutiny and to access less informed / cheaper capital to keep this going, and everyone is monetizing via secondary SPVs instead of public equity

Private equity firms like Blackstone are neck deep in GPU built out credit risk

It was a good article! We wrote about this a lot last year. But really, nobody cared.

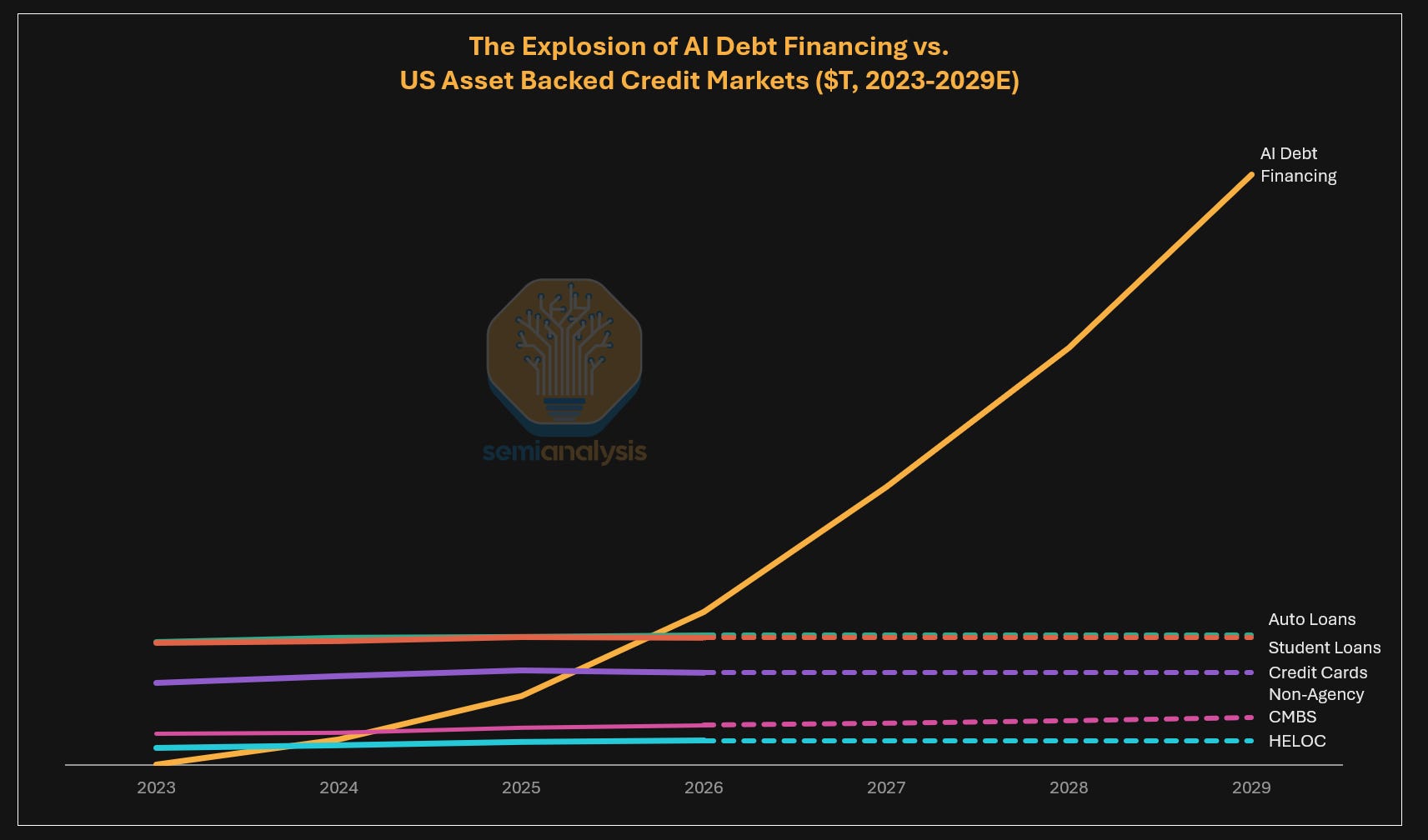

If anything, this stuff reads a bit quaint compared to the monster numbers everyone is putting up today. Semianalysis projects $11 trillion in spending on AI infrastructure between 2024 and 2029, of which $7 trillion is financed by debt.

That seems pretty wild, unless you believe this is existential, humanity-survives-WW3 type stuff. Which is of course how it is being sold straight into our 401ks. And it is also how an enormous amount of liquidity, meaning proceeds from investment rounds, are going into AI companies and venture more generally.

Michael Burry has been adamant about trying to time the short on the AI bubble. While the fundamental story may be there, and the zeitgeist is emerging, so far no real luck. Everything is still going up! To me, it feels like the top of Softbank’s investment in WeWork, when everyone just said OK, this stuff is 50x revenues. Fine.

And as the numbers go up, financial markets begin to form around them.

We are at an interesting intersection of technologies, because some of these products from crypto are now at the heart of the AI markets in ways people don’t see.