Analysis: Why Robinhood spent $300MM on TradePMR, a $40B RIA custodian

Trade PMR deal sets Robinhood up to scale RIA market share.

Gm Fintech Architects —

Today we are diving into the following topics:

Summary: We explore the evolution of Fintech, from its pioneering days to its current mature stage. Robinhood’s $300 million acquisition of Trade PMR, a custodian with $40 billion in assets under custody, highlights a shift in focus from retail innovation to scaling and infrastructure dominance. This deal positions Robinhood to target a $10 trillion market in RIA custody by addressing operational complexities and leveraging proprietary software for growth. The transition from "Commandos" to "Infantry" in the Fintech lifecycle underscores the industry's maturity, as firms like Robinhood and Revolut expand into traditional services like custody, banking, and mortgages.

Topics: Robinhood, Trade PMR, Schwab, BNY Mellon, Altruist, Apex, Coinbase, Virtu, Jump Trading, Revolut

To support this writing and access our full archive of newsletters, analyses, and guides to building in the Fintech & DeFi industries, see subscription options below.

Reminder — this week is your chance to get 25% off our annual plans. This opens up access to writing like the below, as well as our entire archive.

Bluesky

There’s been a migration of of users from X / Twitter to Bluesky. At 2 million daily actives, the site is now about the same size as Meta’s Threads, which had used the Instagram social graph to boot things up. To be fair, about 100 million people in the US still use Twitter daily. All these things are far larger than Farcaster, the biggest Web3 social network, at 50,000 DAUs.

One of the reasons is political — the left is leaving Twitter in response to Musk’s general atmosphere.

But there are other reasons too, like a smooth onboarding experience and a different type of content. Unlike the super-optimized algorithmic drivel that we usually see on social media, BlueSky can serve up deep intellectual and academic content from researchers in economics and artificial intelligence. It has been a breath of fresh air to learn something when you open up the app, rather than feel FOMO about some investment or rage-bait from a lowest common denominator troll.

All this to say, follow me on Bluesky and bootstrap your profile with 👉 some fun economics and AI starter packs. I will still be on X and LinkedIn, but Bluesky allows you to play a new character — I plan to be a more thoughtful one.

Long Take

Execution

We sometimes take the controversial position that innovation in Fintech is dead, and that the frontier of finance has moved into Crypto and AI.

It’s of course not true, but a play on words. Let’s unpack it.

There is a narrow way to define Fintech, and there is a broad way. The broad way is to say that all things people do, all our human ideas, are a “technology” — language, fire, wheels, books, faxes, the Internet, large language models, blockchains are all technology. And wherever they touch finance, that’s “Financial Technology”. To that end, whether we look at electronic trading venues, large card networks, digital lending, portfolio management systems, or DeFi protocols, they are all within the definition.

The narrow way — and more productive path — is to point at Fintech within its Web2 context.

In the middle 2000s, social media applications and cloud providers began distributing content digitally inside walled gardens and created an Attention Economy with which we are familiar today, ruled by attention algorithms. The financial user experience left the bank branch and traveled to the website, the mobile phone, and then into embedded API interfaces for developers. In this story, financial technology followed the evolution of how content was delivered to people in the Internet age. It was primarily centered around retail distribution.

And so, that narrow Fintech view is mostly done as an innovation trend. If your bet is to just launch a mobile bank better than Wells Fargo, the time has passed. If your bet is to use an AI chatbot to sell people branded stablecoin deposits, then game on!

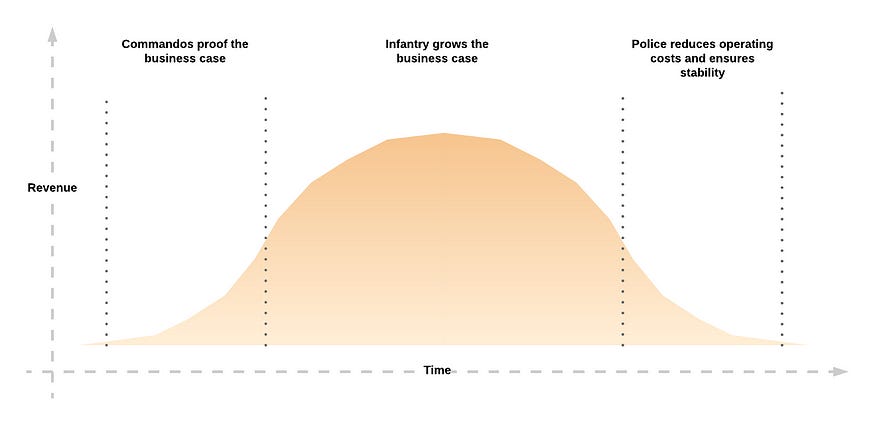

Of course, that’s wrong too. What we really mean to say is that the risk profile of Web2 Fintech has changed dramatically. It is no longer the frontier. This reminds us of the fantastic segmentation for building companies — the Commandos, the Infantry, and the Police — from Accidental Empires by Robert X. Cringley.

The Commandos are the ones fighting uphill to gather new ground. They launch Bitcoin and disappear. They create Revolut and struggle with money laundering problems until they can get licenses. They make trading free and collapse revenue pools, only to be saved by Covid and interest rate hikes. They try to build Synapse and blow things up. Most die in the trenches.

Then you’ve got the Infantry. Once new land has been taken, the Infantry starts to establish operations and build the cities. They create management structures, focus on profitability, and try to go public. New business lines are launched, but they look a lot like old company business lines, and the company starts to resemble those it disrupted.

The last stage is the Police. If you have worked with a Compliance team, or are a Compliance officer, this is where the company attempts to prioritize risk management and sustainability. In the early days of American banking, going out West and setting up a local bank didn’t require compliance with federal regulations. It required having someone to defend your gold vault from bank robbers.

Those commandos are gone, and now we have the CFPB, who want to supervise the world. At least until DOGE dismantles the entire structure.

The traditional financial services industry is largely in the Police stage. If you know, you know.

The fintech industry was the frontier Commandos in 2010, but is now largely filled with Infantry, scaling up the existing winners into large public companies. In many places, the Police are starting to show up.

And that’s a good thing! It means Fintech has won.

Let’s take a look at an applied example of this in action.

Robinhood’s $300MM Acquisition

Robinhood just acquired an RIA custody business, Trade PMR.

It’s a throwback for us to the AdvisorEngine days, a company Lex had co-founded in 2014. Imagine a time when wealthtech was hot and anything was possible!

The relevant industry here is independent financial advisors, or “Registered Investment Advisors” as they are called in the US. These are entities licensed to provide financial advice to individual clients, and are usually a small business composed of financial advisors with their own books. Most RIAs sell financial products, like asset allocations of funds, and require an infrastructure provider in the form of a custodian (to hold the assets) and broker/dealer (to transact in assets). Those tend to be the same firm, the largest of which are Schwab and BNY Mellon with trillions in assets each.

Emerging players include Altruist and Apex.

The price tag for the TradePMR acquisition is $300 million.

The company has $40 billion in assets under custody and serves 350 RIAs, which is a little over $100 million per RIA. This is generally considered to be a small RIA — there are about 15,000 such entities in the US, so you can see that Trade PMR has a fairly low share market share by number of firms — about 2%. By assets, $40 billion should be evaluated against a $6 trillion market size — about .05% market share.