Blueprint: $4.5B valuation for insurtech broker platform wefox; Mexican paytech unicorn Stori 100% credit approvals and 100%+ APRs; Cred Protocols' machine learning Aave default scores

Hi Fintech Futurists —

You are the best, today’s agenda below.

INSURTECH: wefox raises $400 million at $4.5 billion valuation (link here)

DEFI: Cred Protocol: Building a decentralized credit score (link here)

CREDIT: Mexican fintech startup Stori reaches unicorn status with $50M equity raise (link here)

Long Take: What can the Web3 economy learn from eCommerce and paytech? (link here)

Podcast Conversation: The strategy behind Revolut's merchant acquiring and paytech growth, with Simon Taylor, Head of Strategy & Content at Sardine.ai (link here)

In Case You Missed it: Top 10 Fintech Blueprint Articles Last Month (link here)

To go deeper into these topics, including a weekly Long Take, a Web3 digest, and annotated podcast transcripts, click subscribe and explore the additional benefits that come with a premium membership.

Short Takes

INSURTECH: wefox raises $400 million at $4.5 billion valuation (link here)

wefox, a German insurtech firm, raised $400MM in equity and debt at a $4.5B valuation, a 50% increase from its $3B post-money valuation in 2021. The round was led by Mubadala Investment Company and joined by Horizons Ventures, OMERs Ventures, Target Global, and Eurazeo. This is a very chunky raise for a company in a space in duress, so we naturally pay attention.

Founded in 2015, wefox provides insurance products via 3,000 in-house and external advisors, unlike the direct-to-consumer path most fintech competitors usually take. This model works by engaging third-party brokers to use wefox to help advise customers, which in turn has helped the insurtech scale quickly while reducing the cost of acquiring users as brokers, agents and partners are responsible for distribution.

The company’s revenue last year was $320MM, and in the first four months of 2022 the firm has generated over $200MM in revenue, or $800MM ARR coming from 2 million customers. Meanwhile in the insurtech market, Policygenius and Next Insurance are cutting between 17-25% of their workforces. Root, Hippo and Lemonade are also all down this year and since IPO.

The magic counter-cyclical magic sauce for wefox seems to be (1) focusing on lead generation into insurance advisors, (2) have fully digital processes targeting 80% of client needs, (3) offer attractive and hassle free switching subsidies for consumers looking to exit a prior relationship. Seems like an arbitrage between traditional and digital workflows.

DEFI: Cred Protocol: Building a decentralized credit score (link here)

This is very cool. Cred Protocol has launched a machine-learning based credit score using historical borrowing data from top DeFi protocols. The model currently analyses the behaviour and attributes of Aave v2 users to predict the likelihood of liquidation of a loan. Based on this historical data, the results have been predictive about whether a loan will be eligible for liquidation within the next 90 days.

The algorithm ingests health factor and collateral / debt composition data from Aave v2 accounts every 15 minutes. Health factor (HF) is a core statistic for maintaining Aave protocol solvency — when this figure drops below 1, the user is eligible for liquidation (e.g., the supplied collateral is not sufficient to cover the outstanding borrowed balance). Another user can then repay the debt, and receive a corresponding amount of their collateral and an incentivisation bonus in return.

Cred Protocol developed their ML-based classifier using the historical dataset of HFs alongside data on account age, interactions with the Aave protocol, types of assets being borrowed and used as collateral by an account, and aggregations of the time series of historical HF — a dataset of 360MM observations. It has since been able to determine with a high probability the propensity of eligibility for liquidations.

You can see the purple wiggly line (tree-based ML score algo) above strongly outperform the red random walk. Initially the model has been tested with historical borrowing activity solely from Aave V2, but can also incorporate datasets from other protocols like Compound and MakerDAO for the same addresses.

We are a big fan of this work for several reasons. First, it provides DeFi protocols with a better tool for determining “credit scores”, helping to underwrite sustainable lending and borrowing. Second, it may lead to undercollateralized lending, which is the product most people actually need, rather than levering up existing positions. Finally, it may provide a predictor of future market exposures ahead of time.

The team have also open sourced a 1-weekly interval version for others to play around with, and has a Credit Score Beta API waitlist open now.

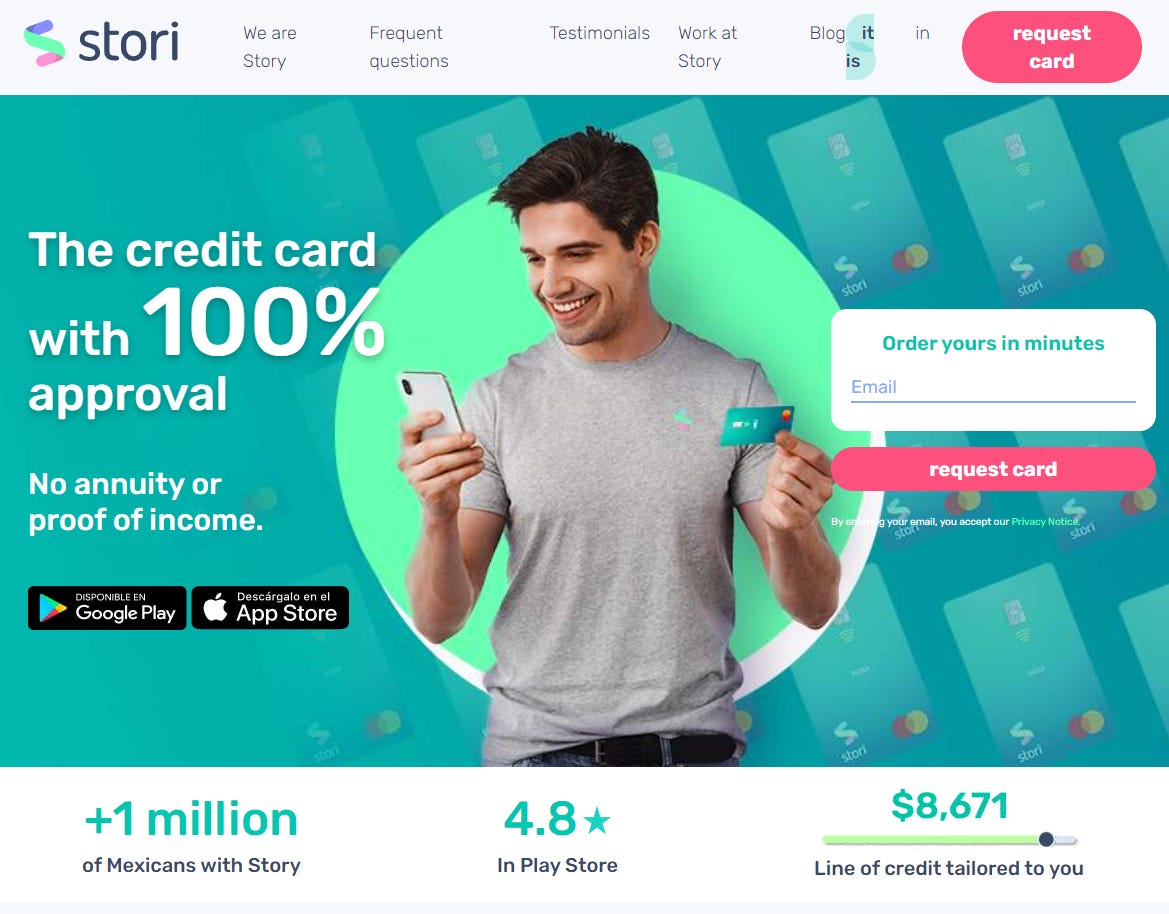

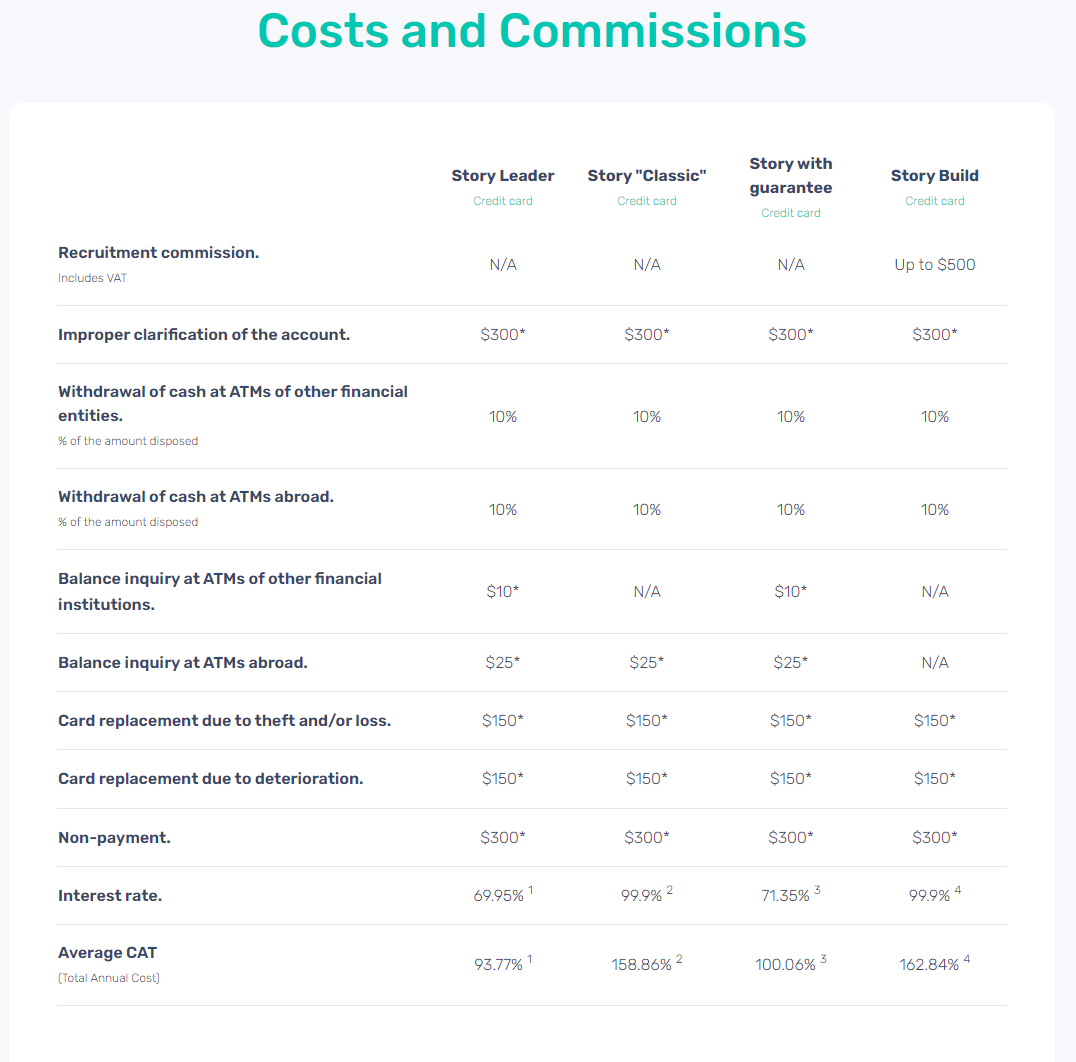

CREDIT: Mexican fintech startup Stori reaches unicorn status with $50M equity raise (link here)

Stori, a credit card for underserved demographics in Mexico, is the latest LatAm unicorn after raising $50MM in equity at a $1.2B valuation, with an additional $100MM in debt financing. This is an extension round of the $125MM in equity and $75MM in debt that Stori raised in September with the valuation up over 25%. Total funds raised by Stori, founded in 2018, now sit at $200MM.

The fintech first launched its credit card product in Mexico back in January 2020 - amassing 1.4 million customers in the meantime (up 3x in the past year), and is looking to expand to another 100 million customers in LatAm. Customers can get setup without a credit history or having to do any paperwork, and can also pay bills directly from within the app. Currently only 45% of South Americans have a bank account, and even fewer have credit cards, suggesting potential for growth.

Stori has no annual fee for users, instead charging a fee for opening an account, ranging between $0 and $500 pesos, which we assume is the starting underwriting capital for credit. But then there are some other fees …

… like a 100%+ APR and 10% fee for cash withdrawals. As a result, revenue is up 20x in 2021, with the majority of this coming through interest and interchange fees from transactions. We raise a quizzical eyebrow at the idea of a 100% approval rating without proof of income, and then charging all this stuff, but you know, whatever.

Long Take: What can the Web3 economy learn from eCommerce and paytech? (link here)

Today we look at the interface between eCommerce and payments technology, digging into issuers, processors, and acquirers.

Commerce is of particular importance as the thesis about DeFi shifts from a standalone financialization engine, to the banking sector for the Web3 economy. We think through what such an economy may need, and discuss DAOs as an atomic commercial unit organizing labor and building products.

The strategy behind Revolut's merchant acquiring and paytech growth, with Simon Taylor, Head of Strategy & Content at Sardine.ai (link here)

In this conversation, we chat with Simon Taylor, the head of strategy and content at Sardine.ai, which is a modern compliance infrastructure.

Before this, Simon served as the Co-Founder and Blockchain Practice Lead at 11:FS. Simon has been immersed in the technology of financial services for as long as he’s been working and is consistently voted one of the most influential people in Banking, Insurance and Fintech by banks, his peers and a number of industry bodies.

ICYMI: Top 10 Fintech Blueprint Analyses Last Month (link here)

Our latest wrap-up of the Fintech Blueprint newsletter Top 10 Fintech Blueprint Articles Last Month includes our best newsletters released last month including —

Insightful conversations with industry experts like Will Beeson and Meidad Sharon

Long in-depth analysis on the most pressing issues in the industry, like the strategic rationale behind FTX strategy for Robinhood, BlockFi, and Voyager

Recaps of the most relevant developments in DeFi & Fintech that shaped the industry over the last couple of months

The Fintech Blueprint strives to keep you at the forefront of the innovation in the world of financial services by providing deep, comprehensive analysis without shilling or marketing narratives.

Read the Top 10 Fintech Blueprint Articles Last Month to stay caught up with DeFi and Fintech markets.

Rest of the Best

Here are the rest of the updates hitting radar.

PAYTECH: Stripe is the latest fintech to falter, taking a 28% internal valuation cut

PAYTECH: Africa-focused fintech Zazuu raises $2M to scale its cross-border payment marketplace

BANKING: SmartBank raises $20 million

INVESTING: UK Fintech Lightyear Launches in 19 EU Nations, Acquires $25M in Funding

INSURTECH: American Family Insurance streamlines claims operations with Tractable’s AI

Shape your Future

Wondering what’s shaping the future of Fintech and DeFi?

At the Fintech Blueprint, we go down the rabbit hole in the DeFi and Fintech industries to help you make better investment decisions, innovate, and compete in the industry.

Sign up to the Premium Fintech Blueprint newsletter and get access to:

Blueprint Short Takes

Web3 Short Takes

Long Takes on Fintech and Web3

Digital Wealth

Access to the Podcasts with annotated transcripts

Full Access to the Fintech Blueprint Archive

Read our Disclaimer here — this newsletter does not provide investment advice and represents solely the views and opinons of FINTECH BLUEPRINT LTD.

Want to discuss? Stop by our Discord and reach out here with questions