Blueprint: Retire with Robinhood?; Starbucks pioneers NFT rewards at scale; Walmart's proprietary BNPL bet

Hi Fintech Futurists —

You are the best, today’s agenda below.

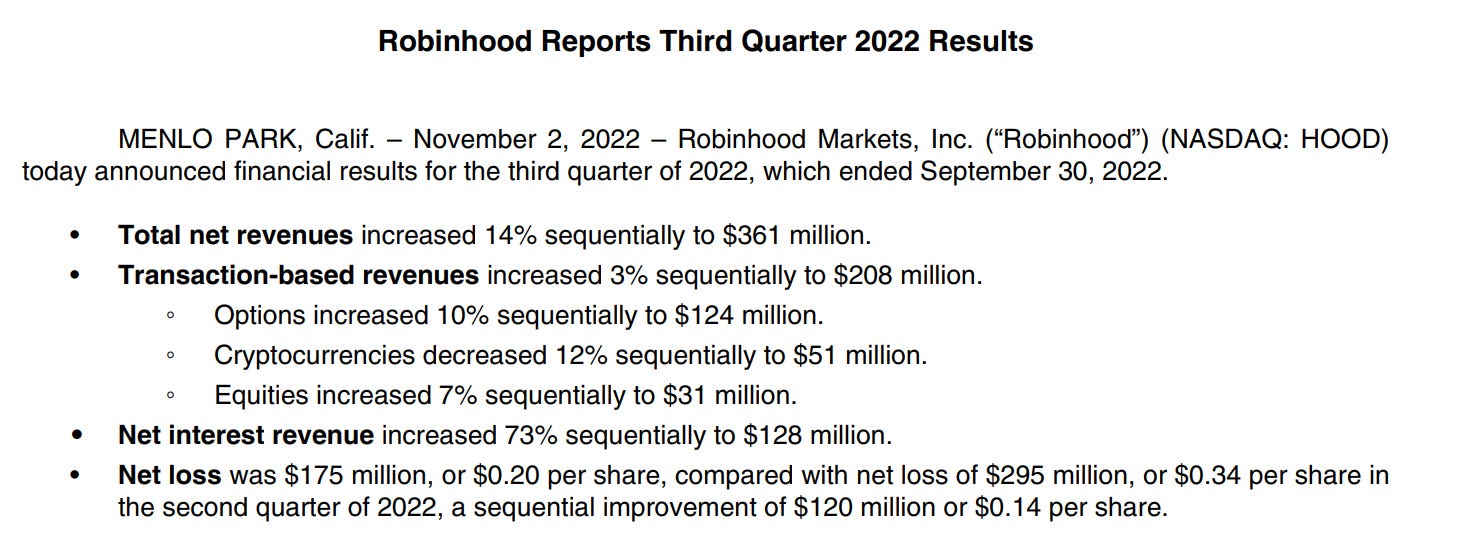

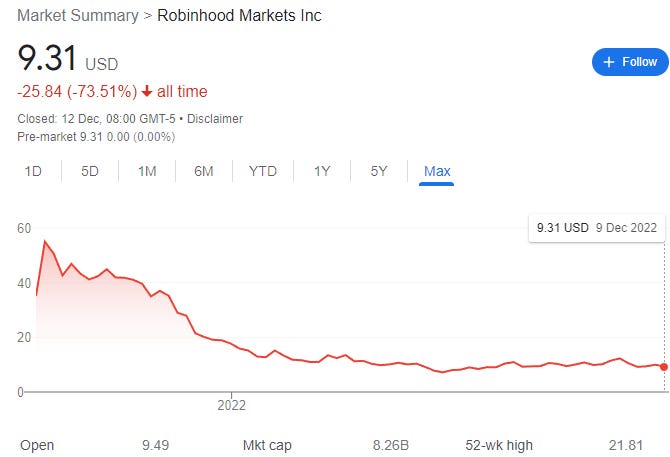

INVESTING: Robinhood banks on retirement to slow user attrition(link here)

NFT: Starbucks Sees 'Unprecedented Interest' as Polygon NFT Rewards Platform Launches (link here)

BNPL: Walmart-backed fintech startup plans to launch its own buy now, pay later loans (link here)

LONG TAKE: What's wrong with $12B Credit Suisse, but right with $8B Wise (link here)

PODCAST CONVERSATION: The emerging problems in banking-as-a-service, with Lex Sokolin and Will Beeson (link here)

Here’s that handy upgrade button to access the Long Takes — a rigorous view on the future of our industry. Level up your Fintech and DeFi knowledge. 👇👇👇

In Partnership

New customers = business growth.

But the easier it is for users to become customers, the more risk and fraud you may face.

Register for this online event on 12/13 to learn how top Fintech companies like Square and Brex use Persona, an identity solution offering configurable infrastructure for KYC, AML, KYB, and more, to assess risk for different customers and configure their identity verification methods to match.

👉 Register to join the discussion tomorrow

Fintech Meetup Delivers Results! Fintech’s BIG new event is Fintech Meetup - it’s the best place to find new deals, partnerships and business opportunities (Q1 is only 3 weeks away!) We use powerful technology to connect everyone across every use case - join 30,000+ double opt-in meetings! Plus 200+ sponsors, 250+ speakers, exhibit hall, & more! At the Aria, Las Vegas March 19-22.

Short Takes

INVESTING: Robinhood banks on retirement to slow user attrition (link here)

Robinhood opened up the waitlist for Robinhood Retirement, an individual retirement account (IRA) offering a 1% match on investments. Anyone with an existing Robinhood account or with the ability to create a Robinhood account can join the waitlist. An IRA is a self-directed account, rather one offered by an employer — Robinhood claims that it is targeting gig economy workers, i.e., those who do not have a full-time job or employer-sponsored 410(k) plan to start saving for retirement. Maybe all the day-traders that rage quit the workforce during the pandemic?

The retirement account boasts Robinhood signature price of “free” — no fees to maintain the account, zero commissions and no account minimums, with the only fees being subject to their fee schedule. Customers will be able to choose between investing in stocks and ETFs using a traditional IRA or Roth IRA, with the help of in-app recommendations. They will also be able to leverage the newly launched stock lending capabilities in app to earn interest on their savings — remember that margin generates fees for Robinhood, and also that leverage is dangerous.

Robinhood has been struggling, like most fintechs recently. In August, it cut 23% of the workforce, three months after cutting 9% , impacting around 1,000 employees in total. The firm was also fined $30MM by a NY financial regulator for their crypto trading services in the same month, lost 1.8MM monthly active users in Q3 dropping to 12.2MM, and the SEC threatened to ban payment for order flow, which is how Robinhood makes most of its money.

Brokerage is good when markets are up, and terrible when markets are down. The smart move is to diversify revenues prior to a bearish turn and the recession.

👑 See related coverage 👑

NFT: Starbucks Sees 'Unprecedented Interest' as Polygon NFT Rewards Platform Launches (link here)

One of the first large scale commercial applications of NFTs has come from Starbucks, which had previously pioneered digital wallets and contactless payments. The coffee chain launched Starbucks Odyssey, a Web3-based reward platform on Polygon, to beta testers last Thursday, with additional testers being on-ramped in January 2023 before the wider rollout. Starbucks Odyssey draws on the current rewards program, where users can earn points for in-store purchases, and adds features like participation in quizzes and other digital experiences to earn digital points, which can then be used to redeem “Journey Stamps”, tokenised collectible Polygon NFTs.

Collected NFTs can be used to unlock exclusive events or experiences, like a trip to the company’s coffee farm in Costa Rica, drink-making classes, or general local events. The effect is to incentivize and gamify the shopping experience with Starbucks, thereby increasing customer loyalty and spending. For those strictly interested in collectibles, they will be able to buy stamps with their credit cards or trade with other users on a secondary marketplace, powered by Nifty Gateway. A portion of funds from NFT sales will reportedly be donated to charitable causes.

| Insider Intelligence")

We are excited to see NFTs become more deeply integrated into commerce, with company loyalty and rewards programs as a first step. Leveraging these schemes can help improve user stickiness not just for Starbucks, but for many large shopping brands. Starbucks was exactly the champion needed for contactless payments adoption. Secondly, Polygon is becoming the de facto chain for reward schemes, partnering with Meta on Instagram NFT minting, Reddit for their NFT avatars that have amassed over 3 million users, and Nike’s .Swoosh Web3 platform.

While skeptics of blockchains continue to obsess about financial crises, digital objects are being minted at scale in Web3 and used within retail experiences.

Interested in Sponsorship?

To learn more about how to support the Fintech Blueprint and reach our 150,000+ Substack and LinkedIn audience of builders and investors, learn more below or contact us here.

BNPL: Walmart-backed fintech startup plans to launch its own buy now, pay later loans (link here)

Walmart has a partnership with BNPL provider Affirm. But that isn’t preventing the retailer from launching its affiliated BNPL start-up, One, into production next year. One is a majority-owned by Walmart BNPL service that will serve Walmart, as well as other retailers, by helping consumers to pay off their bill with monthly payments, including interest. With cost of living increasing, many people unfortunately have to turn to debt.

We’ve covered how the BNPL market has become increasingly saturated for some time — currently Affirm, PayPal, Klarna, and AfterPay each have their own versions of consumer underwriting, and Apple recently announced Apple Pay Later. Despite their popularity, BNPL models are yet to become profitable when they are a company’s only product. For Walmart and Apple, however, who generate profits through deep commercial activity, using credit as a loss-leader to drive transaction volume, may be the right trade-off.

Walmart has always had a financial offering attached to its retail presence, but it had not all been modernized. But it has steadily been increasing its exposure to fintech: (1) working with Ribbit Capital, one of the key investment firms behind Robinhood, to create and back an all-in one-app for consumers to manage their money, and (2) acquiring One and Even for an undisclosed amount this year to help facilitate this, with the two companies adopting the One branding. Walmart is the largest private employer and grocer in the US, and there is a enormous customer base that trusts the brands and would adopt its fintech products. This makes Walmart a credible threat to smaller fintech players going after the same demographic.

👑 See related coverage 👑

Long Take: What's wrong with $12B Credit Suisse, but right with $8B Wise (link here)

Credit Suisse has been in the news about its failing investment banking division and need to raise capital.

We use that as a jumping off point to explore the scale of such a business, and the damage that can be done in bundling capital markets into wealth and private banking. As a comparison, we look at the result of Wise and SoFi. Wise has held value despite a bad fintech SPAC / IPO market and we explore the reasons why. Similarly, SoFi has struggled, and we show how its growth strategy is less in favor during a risk-off environment. Also, some GPT-3 prompts for your pleasure.

Podcast Conversation: The emerging problems in banking-as-a-service, with Lex Sokolin and Will Beeson (link here)

In this conversation, we chat with Will Beeson, who currently works at Standard Chartered Ventures.

Previously, Will was the Co-Founder & Chief Product Officer at digital bank BELLA, as well as, a Principal at Rebank, a fintech advisory firm. Will’s banking entrepreneurship streak doesn’t end there, he co-founded Allica, a digital bank for businesses in the UK. After starting his career at Citigroup in New York, Will spent nearly a decade in Europe working with and managing financial services companies prior to launching Allica. Will holds a BA from Amherst College (USA) and is a Chartered Financial Analyst (CFA) Charterholder.

Rest of the Best

Here are the rest of the updates hitting radar.

PAYTECH: Tonik acquires TendoPay, enters employee benefits market

BAAS: SBM Bank India, building BaaS platform, seeks funding at $200 million valuation

NEOBANK: Monzo chief says UK digital bank will turn a profit in 2023

LENDING: JG Wentworth Acquires Fintech Lending Platform from Stilt Inc.

CONSUMER: Ocho wants to rethink (and rebrand) personal finance for business owners

ROBOADVISOR: 401(k) Robo-Adviser Blooom Shuts Services, Sells Tech to Morgan Stanley

AI: Akros Technologies, an AI-powered asset management platform, raises funding from Z Holdings

INSURTECH: Insurer-backed BeeHero raises $42 million

Shape your Future

Wondering what’s shaping the future of Fintech and DeFi? At the Fintech Blueprint, we go down the rabbit hole in the DeFi and Fintech industries to help you make better investment decisions, innovate, and compete in the industry.

Read our Disclaimer here — this newsletter does not provide investment advice and represents solely the views and opinions of FINTECH BLUEPRINT LTD.

Want to discuss? Stop by our Discord and reach out here with questions