AI: GPU-Backed Stablecoins blend AI infrastructure with DeFi at 8% APR

Tokenized compute may become a foundation of the AI-powered machine economy.

Hi Fintech Futurists —

Today’s agenda is below.

AI: GPU-Backed Stablecoins Blend AI Infrastructure with DeFi

We explore how GPUs — the backbone of AI infrastructure — are becoming collateral for high-yield stablecoins like USDai, which offers 8-15% APY by backing tokens with revenue from GPU rentals. While this mirrors traditional debt instruments, there are concerns about hardware depreciation, falling rental yields, and borrower risk. Projects like USDai and Aethir are experimenting with tokenizing compute infrastructure, generating millions in revenue, but these models raise regulatory questions under the Howey test and may be inappropriate for retail investors. Despite risks, the financialization of compute is a powerful trend — enabling capital formation, secondary markets, and decentralized infrastructure that underpin a future machine economy.LONG TAKE: Stripe, Circle, and Tether launching their own L1 money chains

PODCAST: Building the $130B global payments platform, with Airwallex’s Ravi Adusumilli

To support this writing and access our full archive of IPO primers, financial analyses, and guides to building in the Fintech & DeFi industries, see subscription options here. Our current price point is only $2/week.

Thanks for your time and attention,

Lex Sokolin

Our Ecosystem: AI Venture Fund | AI Research | Lex Linkedin & Twitter | Sponsors

In Partnership: Mode Mobile

Mode’s EarnPhone reaches 50MM+ users who have earned over $325MM, and that’s before global satellite coverage. With SpaceX eliminating "dead zones" worldwide, Mode's earning technology can now reach billions of people in unbanked and rural populations worldwide.

Their global expansion is well-timed, and you have a chance to invest in their pre-IPO offering. Mode’s recent revenue growth and reserved Nasdaq ticker $MODE puts them one step closer to a potential IPO.

Disclosure:

Mode Mobile recently received their ticker reservation with Nasdaq ($MODE), indicating an intent to IPO in the next 24 months. An intent to IPO is no guarantee that an actual IPO will occur. The Deloitte rankings are based on submitted applications and public company database research, with winners selected based on their fiscal-year revenue growth percentage over a three-year period. In making an investment decision, investors must rely on their own examination of the issuer and the terms of the offering, including the merits and risks involved. Mode Mobile has filed a Form C with the Securities and Exchange Commission in connection with its offering, a copy of which may be obtained via the following link: https://www.sec.gov/Archives/edgar/data/1748441/000164117225025402/ex99.pdf

The GPU-Backed Stablecoin: When Silicon Becomes Collateral

GPU Collateral

It’s always fun when two seemingly unrelated trends start to converge.

We have deeply covered USDC, USDT, and the parade of fiat-backed stablecoins that have recently captured the Fintech imagination. We also previously discussed how large private equity firms are issuing debt to finance the AI infrastructure boom.

What if we told you that those AI GPUs — the chips powering training ChatGPT— are also becoming the collateral for digital dollars? For context, NVIDIA's flagship H100 GPUs sell for $30,000+ each and are in high demand by the hyperscalers (Google, Tesla) and neoclouds (Coreweave). GPU spending rose from $30B in 2022, to $50B in 2023, and $100B by 2024.

This has resulted in a very good time for NVIDIA.

It has also benefited the GPU data center lenders.

But now we are seeing the same industrial logic applied to crypto-based stablecoins. Reminder that collateralized stablecoins are akin to a collateralized piece of debt, trading at par with some yield that is generated by the underlying assets. That collateral could be a money market fund, yielding 4% and thereby standing up the entire Circle business, or it could be some other exotic asset.

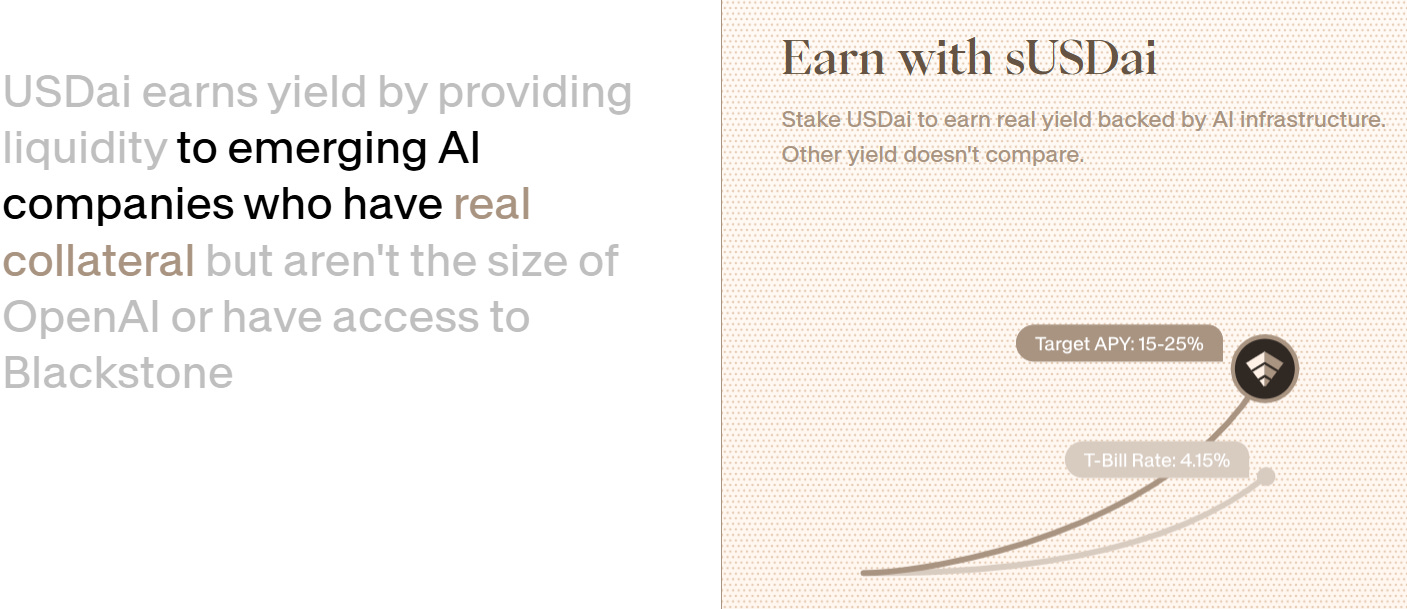

Enter USD.AI — a stablecoin backed by revenue-generating GPU clusters. The pitch for holding it is a target 15% APY (currently at 8%), which is about 3x Treasury bills and 15x what JPMorgan pays on savings. It is priced like a GPU junk bond.

The company raised $13MM from Framework Ventures in August 2025, with $50MM already deposited during private beta. The model includes USDai (dollar-pegged) and sUSDai (yield-bearing backed by compute revenues). When you buy sUSDai, you're buying future GPU rental income.

But there is always a risk that the underlying borrower cannot pay the debt.

First, consider the rate at which GPUs depreciate. NVIDIA launched the A100 in mid-2020, then obsoleted it with the H100 two years later. AMD's Instinct MI250 lasted 18 months. If your underlying asset is worth less, the bond is less secured.

Further, the rental rates are compressing. Current H100 hourly rates range from $2-13, and long-term contracts push prices to $1.80/hour. Some providers offer A100s at $0.66/hour, which is 4-8x cheaper than AWS.

What happens when NVIDIA floods the market with new chips? The borrower charges less for rent, and therefore has less cash to pay the coupon payments.

Therefore, the collateral underneath GPU debt coins is subject to the usual underwiting disclosures. The borrower may repay, or the borrower may default. Companies like Coreweave have been wildly successful in building out neoclouds, but it is less clear what the future looks like for the longer tail of smaller firms.

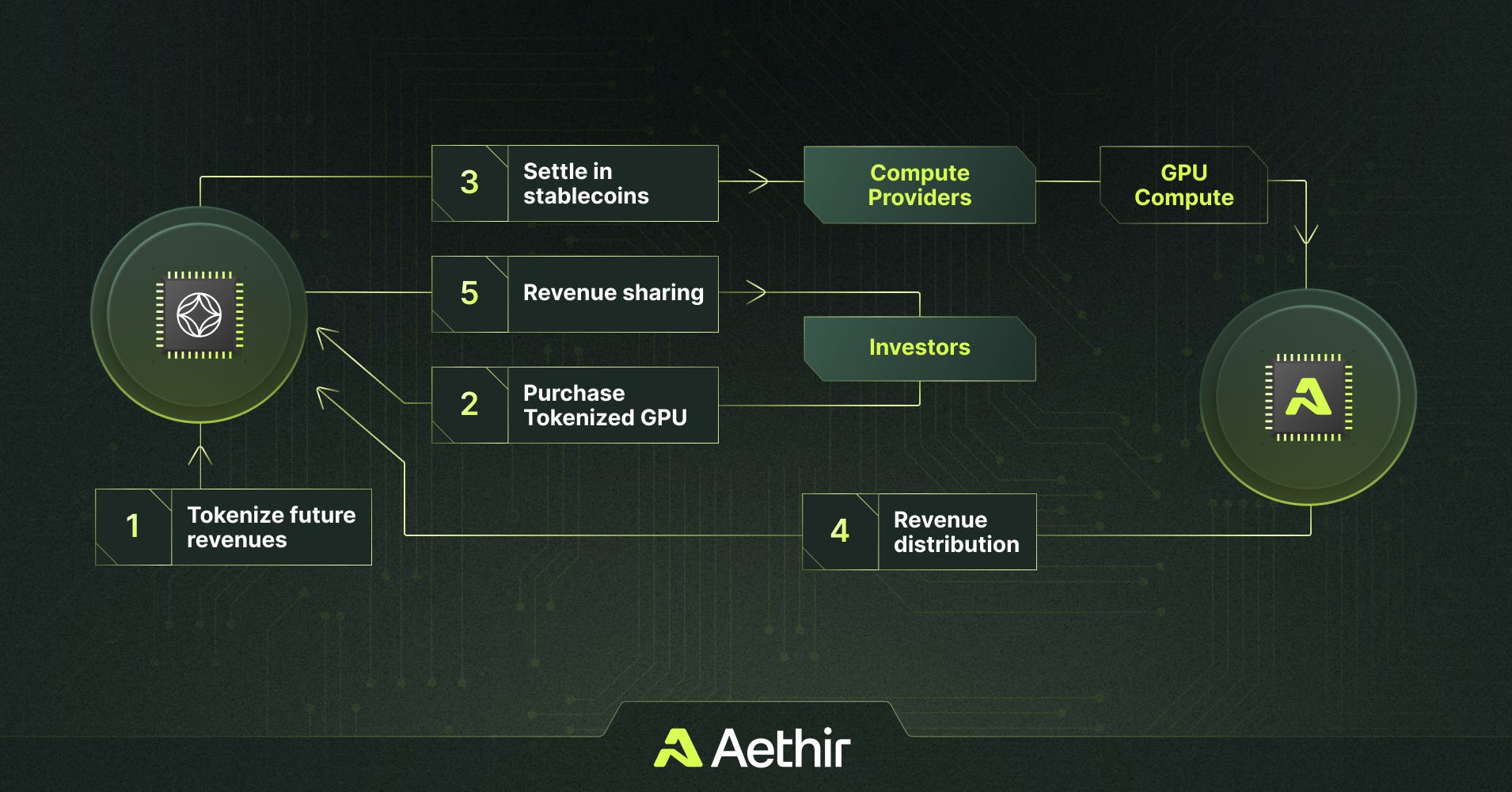

There are other proects experimenting in this vein. For example, GAIB and Aethir launched tokenizing GPUs on BNB Chain.

Their pilot — backed by market maker Amber Group — raised $100,000 in 10 minutes, but is still in early stages relative to more serious capital. Aethir brings 400,000+ GPU containers, including 3,000+ H100s/H200s, plus 62,000+ edge devices, and the protocol claims to generate $90MM+ in annualized revenue. Investors purchase tokenized GPUs using stablecoins, and those are backed by future GPU revenue and platform rewards. It looks like factoring for the AI industry.

Decentralized GPU networks are absolutely a real category, and we are excited to see interesting takes on the financialization of their economics. But too much financial engineering is also a problem, if the underlying revenue model comes under pressure.

Some of you may remember Anchor Protocol on Terra/Luna — 20% APY on UST seemed sustainable until it wasn't. There were structural failures hidden behind financial engineering, including recursive looping of collateral to back stablecoins with protocol tokens.

GPU-backed stablecoins do not have the same problem, since they have underlying hard assets — the data centers and chips. But there are long tail risks to the demand for current hardware. What happens when AI can run on fewer resources for similar tasks, and intefence is more important than training?

It may not be appropriate for retail investors — those most likely to hold stablecoins — as the infrastructure build-out slows down. Further, retail investors are usually less well diversified than institutions to take on real underwriting risk. We are reminded of the early days of Lending Club and peer-to-peer lending.

Additionally, GPU-backed stablecoins look very much like traditional securities under the Howey test: (1) Investment of money, (2) in a Common enterprise: (Pooled GPUs), (3) with an expectation of profits: (15% APY), and (4) from efforts of others.

The SEC has been permissive in the memecoin era, but it is something to consider.

On the other hand, demand is clearly still there. Many AI startups can't get GPUs, or cannot finance their own build-outs and would be willing to use a more retail instrument. Unlike algorithmic stablecoins, there's actual collateral. And GPUs are real assets generating real revenue.

The idea of tokenizing compute is powerful, and we think will survive. Web3 brings a number of financial ideas to the equation that are being tested in real time:

Primary Markets. Initial capital bootstrapping through token incentives to building decentralized GPU networks that world like a Web2 cloud

Secondary Markets. Trading of tokenized GPU-equivalent work units, as well as tokens representing various networks.

GPU Debt Coins. Collateralized loans to GPU providers as discussed today

All these things point to the building blocks of a machine economy, where the hardware for computation is plugged back into the modern financial networks of blockchain protocols. At some point in the future, an AI is just as capable of self-financing its own build out as a human being.

Even if every current protocol fails, the idea persists. In a world where compute is the new oil, someone will figure out how to financialize it.

👑Related Coverage👑

Blueprint Deep Dive

Analysis: Stripe, Circle, and Tether launching their own L1 money chains

We explore the rise of company-specific blockchains as institutions like Stripe, Circle, and Tether launch their own Layer-1s for payments and stablecoin infrastructure, diverging from Ethereum’s open, shared architecture. The trend echoes the 2015 “Blockchain, not Bitcoin” era, as firms attempt to capture vertical economics (e.g., gas fees, token value) while still relying on EVM standards.

This growing fragmentation risks recreating walled gardens, undermining the very interoperability that makes public chains valuable. Ethereum's strength has been its multipurpose adaptability, evolving through ICOs, DeFi, NFTs, and stablecoins while preserving a single composable state. The long-term opportunity lies in enhancing the shared crypto commons, rather than creating siloed appchains for individual institutions.

🎙️ Podcast: Building the $130B global payments platform, with Airwallex’s Ravi Adusumilli

In this episode, Lex speaks with Ravi Adusumilli - President and GM of the Americas at Airwallex. Ravi and Lex discuss how Airwallex has evolved into a global financial platform by offering businesses an integrated suite of cross-border payments, treasury, and banking services. Founded in 2015, Airwallex now supports 150,000 customers, processes $130 billion in annualized volume (up 73% YoY), and projects a $1 billion revenue run rate by year-end.

The company’s success stems from its end-to-end infrastructure, homegrown payment rails, and multi-product strategy, with 80% of revenue now coming from customers using more than one product. Airwallex differentiates itself by focusing on global-first B2B use cases and building regional autonomy alongside centralized infrastructure. While not prioritizing stablecoins today, the company is exploring AI-driven financial operations and aims to reach $1 trillion in transaction volume by 2030.

🚀 Postscript

Sponsor the Fintech Blueprint and reach over 200,000 professionals.

👉 Reach out here.Check out our new AI products newsletter, Future Blueprint. (Don’t tell anyone)

Read our Disclaimer here — this newsletter does not provide investment advice

Contributors: Lex, Laurence, Matt, Farhad, Daniel, Michiel, Luke

For access to all our premium content and archives, consider supporting us with a subscription. In addition to receiving our free newsletters, you will get access to all Long Takes with a deep, comprehensive analysis of Fintech, Web3, and AI topics, and our archive of in-depth write-ups covering the hottest fintech and DeFi companies.

AI and DeFi convergence is ushering in new collateral types and programmable money flows. My ongoing research series features protocol founders building AI-backed stablecoins and infrastructure bridges. What technical hurdles or real-world use cases excite—or concern—you most in this intersection?

The evolution of securitization. The evolution of negotiable instrument trading at par.