Fintech: Is an end to Goldman's consumer journey finally in sight? Goodbye Apple.

Fintech: Is an end to Goldman's consumer journey finally in sight? Goodbye Apple.

Goldman may have found someone to take over the Apple Card program

Hi Fintech Futurists —

Today’s agenda below.

FINTECH: Is an end to Goldman's consumer journey finally in sight? Goodbye Apple.

LONG TAKE: Analysis: The $100B+ Opportunity in Employment Tech, shifting from CFO to CEO (link here)

CURATED UPDATES: Paytech, Neobanks, Lending, Regulation & Policy, Digital Investing

To support this writing and access our full archive of newsletters, analyses, and guides to building in Fintech & DeFi, subscribe below. No more paywalls.

Interested in AI? We are experimenting with a new AI product newsletter here.

👉👉👉 Check it out.

Digital Investment & Banking Short Takes

Is an end to Goldman's consumer journey finally in sight? Goodbye Apple.

Last week, The Wall Street Journal reported that JPMorgan is in discussions with Apple to take over its credit card program.

While a final agreement is far from certain, negotiations that began earlier this year have made significant progress in recent weeks. This potential deal emerges approximately ten months after Apple announced its decision to end its partnership with Goldman Sachs. Since then, both companies have explored multiple options, including talks with Capital One, Synchrony, and American Express, but none of those deals came to fruition. Should the JPMorgan deal succeed, it would mark the conclusion of Goldman's troubled venture into consumer finance.

Before exploring the potential implications of this move for the companies involved, the industry, and credit card holders, it’s essential to understand the path that brought us here. In 2015, Goldman Sachs decided to enter the consumer space by acquiring GE Capital Bank’s U.S. online deposit platform, along with approximately $16 billion in deposits, and quickly thereafter launching Marcus, an online platform offering savings accounts and personal loans to retail investors. The strategy behind this move was twofold. First, while investment banking and trading — Goldman’s core focus — had been highly profitable, these sectors were inherently cyclical. Expanding into consumer finance was seen as a way to offset those fluctuations and create a more balanced revenue stream. Second, there was a broader perception that Goldman’s enterprise value lagged behind competitors due to the lack of established consumer infrastructure.

In the following years, Goldman Sachs continued to invest in and expand its consumer finance footprint. While we won’t dive into all the specifics here (we’ve covered them in detail previously), the key takeaway is that this once highly anticipated venture into the consumer space quickly became plagued by a series of setbacks. These included delayed product launches, ill-fated acquisitions, employee departures, regulatory scrutiny, and, predictably, significant financial losses. This all led to Goldman’s abrupt shift in 2022, when the firm announced plans to scale back its consumer business. As Goldman Sachs CEO remarked in 2022, “We tried to do too much, too quickly, and as a result, some of our execution wasn’t good ... you reflect on what you’ve done, learn, adapt, and move forward.”

The timeline below outlines some of the major events—or, more accurately, missteps—during this period.

This brings us back to the Apple Card.

Once expected to be the "crown jewel" of Goldman's consumer portfolio, it quickly became another example of the bank's struggles in the space. From the outset, the program faced challenges.

Eager to break into the consumer market, Goldman reportedly made concessions that other card issuers wouldn’t. For instance, Apple pushed to approve as many customers as possible. While it’s understandable that Apple, like most partners, wanted broad customer acceptance, it doesn’t mean one should oblige. Apple's customer base is vast, and owning an iPhone doesn’t necessarily qualify someone for a credit card — though Apple seemed to believe otherwise.

In their eagerness to enter the market, Goldman seemingly agreed to these terms. As a result, the bank, once known for serving top-tier clients, effectively became a subprime lender, with over a quarter of its Apple Card accounts going to customers with a sub-660 FICO score. This figure only worsened over time.

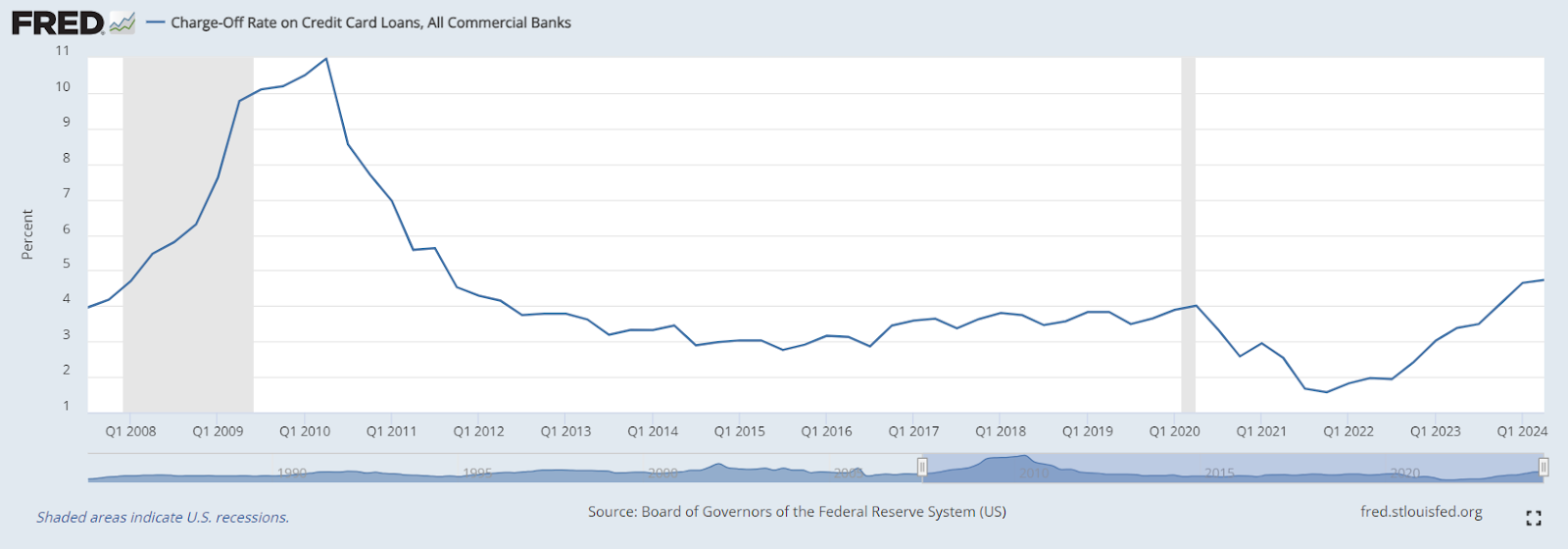

While managing a portfolio with many subprime clients can be profitable, the key is ensuring that revenue from interest, interchange fees, and other charges outweighs the losses. Unfortunately for Goldman, a perfect storm of factors made the Apple Card unprofitable.

First, it was a “no-fee” card, so the usual additional fees (like late charges) that help cover costs weren’t available. Second, many cardholders didn’t carry balances as Goldman had anticipated, resulting in lower-than-expected interest revenue. Lastly, too many of those who did carry balances failed to pay them off, forcing Goldman to charge off the accounts. These charge-off rates continued to rise, surpassing the national average and even exceeding those of other banks with large subprime portfolios, such as Capital One.

Beyond the financial challenges, Apple’s unique demands — such as having all customers receive their billing statements on the first of the month rather than the industry norm of staggered dates — created significant operational headaches for Goldman.

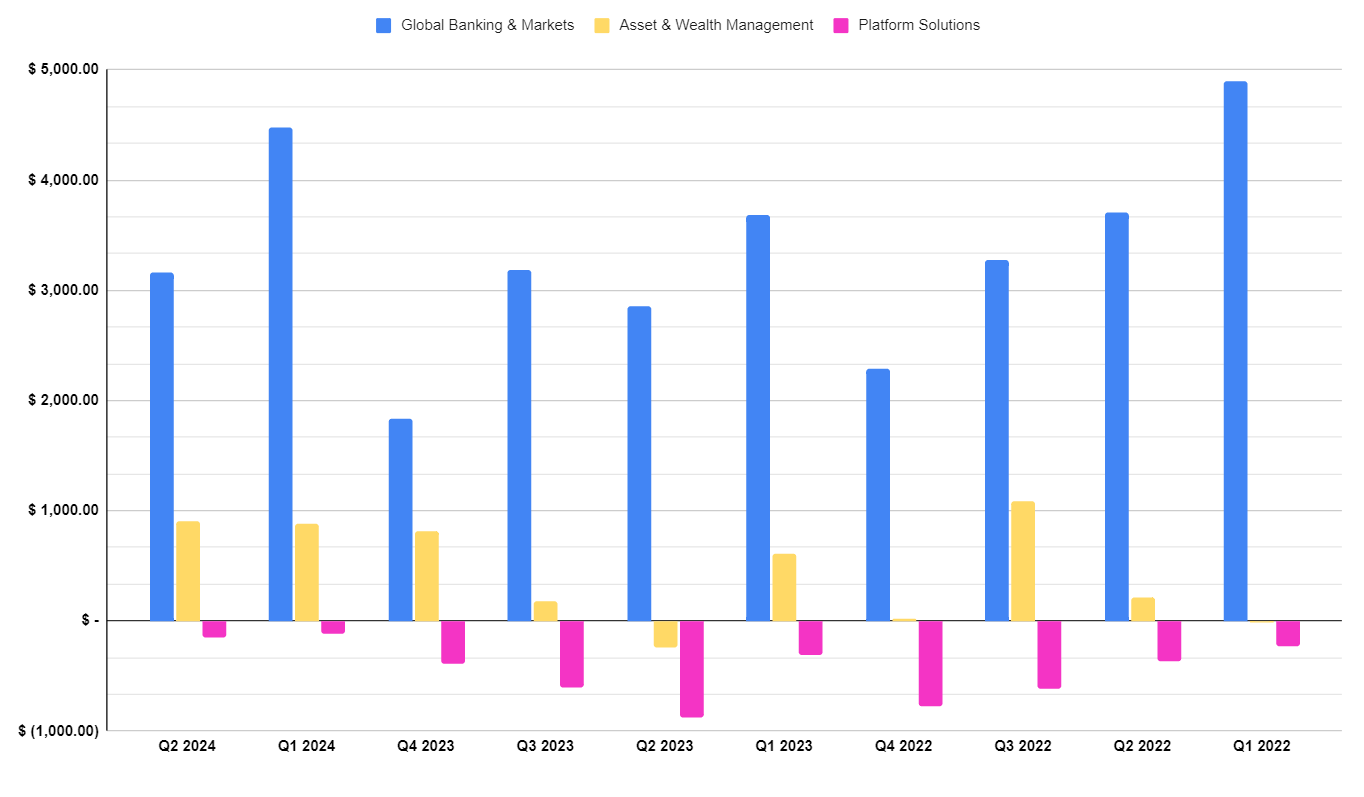

All these factors combined turned the Apple Card into a costly misadventure for Goldman, especially glaring compared to the company's successes elsewhere. The chart below highlights the performance of Goldman's Platform Solutions division (which is primarily composed of its consumer card business) in contrast to its other two core business lines.

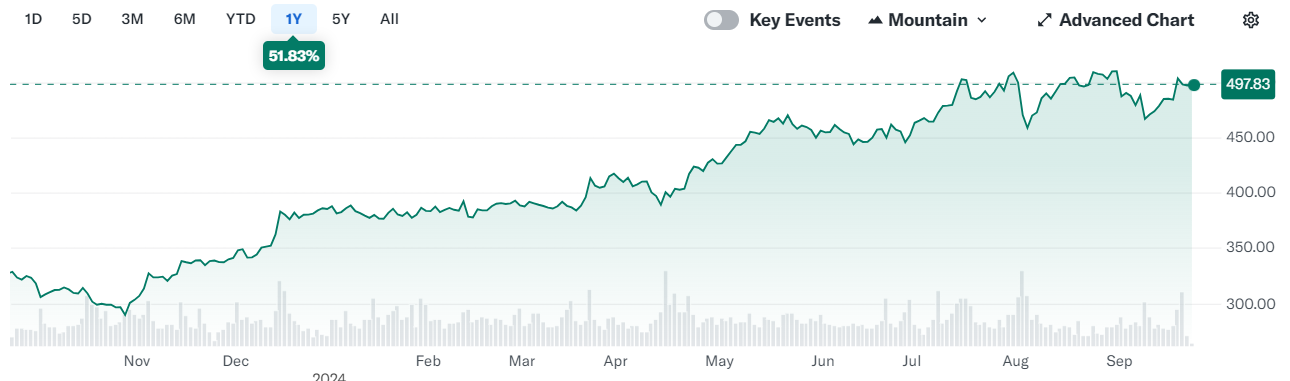

Despite the financial struggles of Goldman’s consumer efforts, news of their continued retreat from the space has been positively received by the market, with Goldman’s stock rising over 50% in the past year.

However, as we noted earlier, the deal for JPMorgan to acquire the Apple Card program is far from certain, and whether it’s a good fit remains debatable.

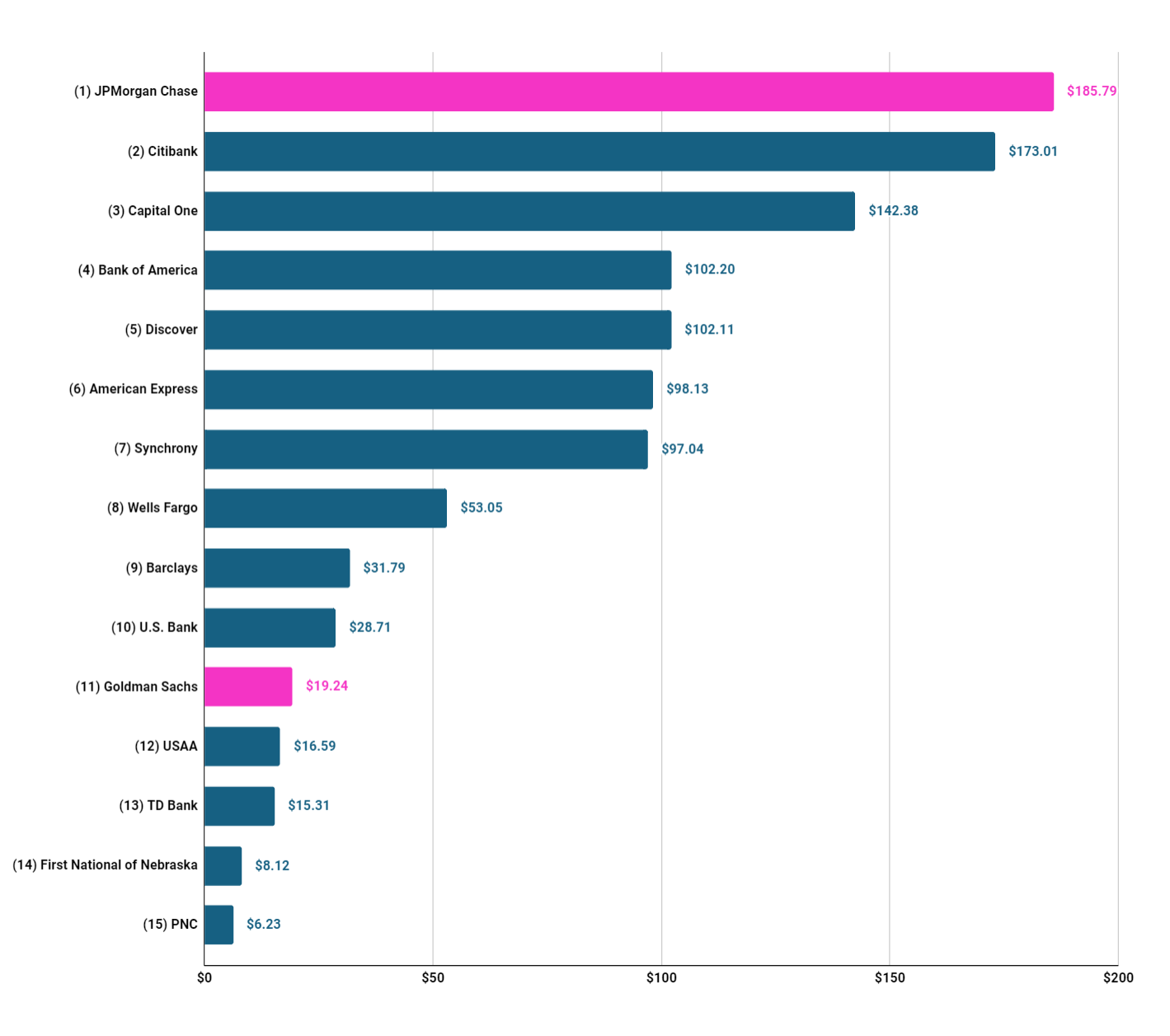

On the one hand, as the largest credit card issuer, JPMorgan’s scale and expertise in consumer lending could help turn the program around.

They’ve also successfully managed a co-branded card program for another tech giant, Amazon, since 2017. That said, in its current state, the Goldman portfolio is a far cry from JPMorgan’s current portfolio.

Perhaps the biggest hurdle in this deal is the sale price. When a portfolio has low delinquency, and people are paying interest, credit card balances can sell for more than the portfolio value. Unfortunately, that’s not the case with Goldman’s current portfolio. The crux of this deal will likely depend on how much Goldman is willing to discount the portfolio in order to exit their consumer finance experiment once and for all.

Given the struggles they endured, we’d wager it will be substantial.

👑 Related Coverage 👑

Long Take

Curated Updates

Here are the rest of the updates hitting our radar.

Paytech

Brex rolls out embedded payments tool - BankingDive

Miami-based AI bookkeeping startup Finally has raised another big round: $200M in equity and debt - TechCrunch

Swift to develop concrete plans for CBDC and tokenised asset exchange - Finextra

Paymob secures $22m to bolster digital payment infrastructure in MENA - Fintech Global

Neobanks

⭐Revolut eyes expansion in Gulf with a licence application - The Paypers

Dutch neobank Bunq goes on hiring spree, targeting digital nomads, as other fintechs slash jobs - Bloomberg

Bad Loans Pile Up at Nubank, Latin America’s New No. 1 Bank - Yahoo Finance

Lending

Barclays Joins Push to Get Rid of Faxes in the Loan Market - Yahoo Finance

Regulation & Policy

⭐FDIC Unveils Fintech Account Proposal to Stop Synapse Repeat - Bloomberg Law

Innovation may slow amid bank-fintech partnership scrutiny: analysts - BankingDive

Brazil preps new round of CBDC pilots - Finextra

Digital Investing

BBVA Switzerland adds support for USDC stablecoin - Ledger Insights

US FinTech companies completed 5 of the top 10 deals globally in H1 - FinTech Global

🚀 Level Up

Join our Premium community and receive all the Fintech and Web3 intelligence you need to level up your career. Get access to Long Takes, archives, and special reports.