Fintech: Nubank's stellar Q2 makes the case for a $250B valuation

17% Net Interest helps a lot

Hi Fintech Futurists —

Good morning. Today’s agenda below.

FINTECH: Why Nubank's Q2 earnings make the case for a $250B valuation

This week, we analyse Nubank's Q2 2025 results, published on 14th August 2025, which show the Brazilian digital bank reaching 122.7M customers with $3.7B in revenue (+40% YoY) and a 28% ROE that outpaces every major US bank. We examine what's driving the LATAM fintech's hypergrowth beyond Brazil, how its unit economics compare to developed market challengers like Chime and Revolut, and why the path from today's $60B valuation to $250B is more feasible than it appears.ANALYSIS: Robots, Crypto, and the Collapse of Old Systems (link here)

CURATED UPDATES: Paytech, Neobanks, Lending, Digital Investing

To support this writing and access our full archive of newsletters, analyses, and guides to building in Fintech & DeFi, subscribe below (if you haven’t yet). Prices will be going up soon, so lock it in now.

Digital Investment & Banking Short Takes

Why Nubank's Q2 earnings make the case for a $250B valuation

There's something remarkable happening in São Paulo that most of the fintech world is missing.

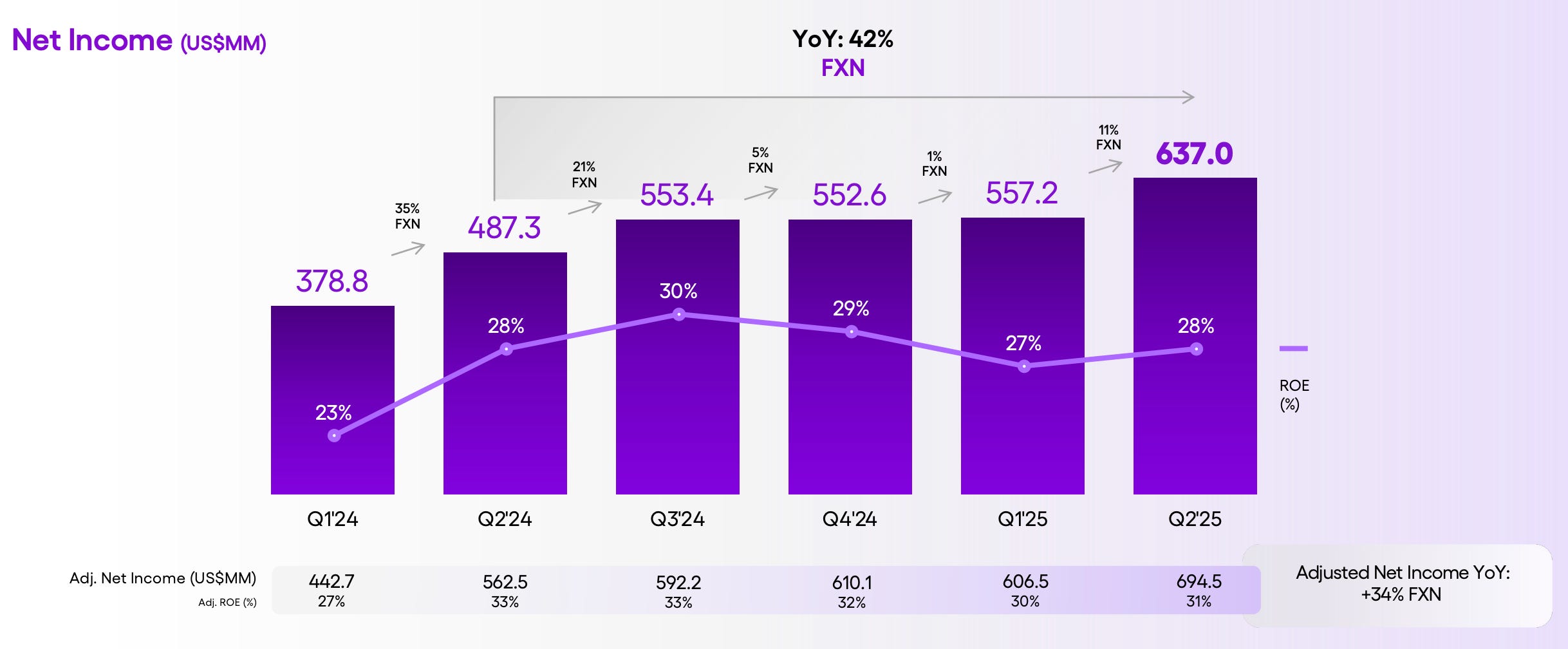

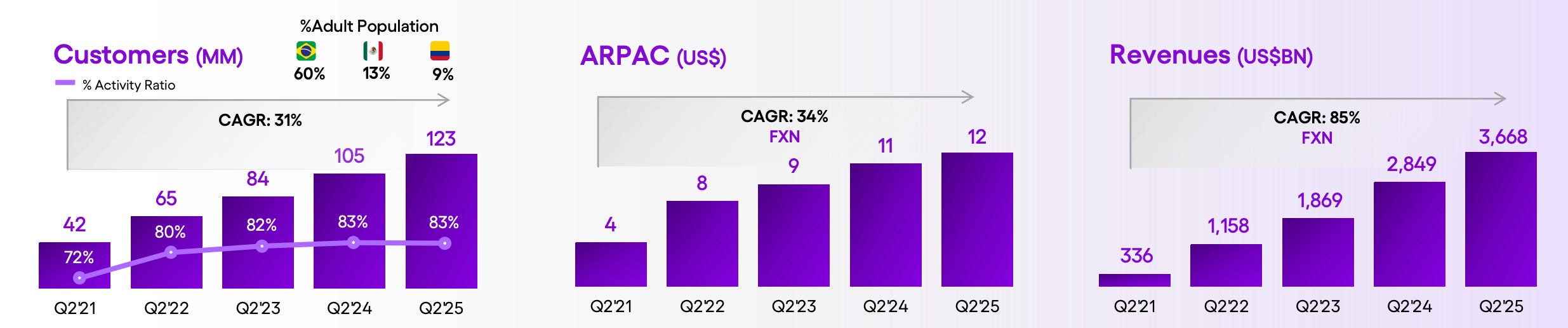

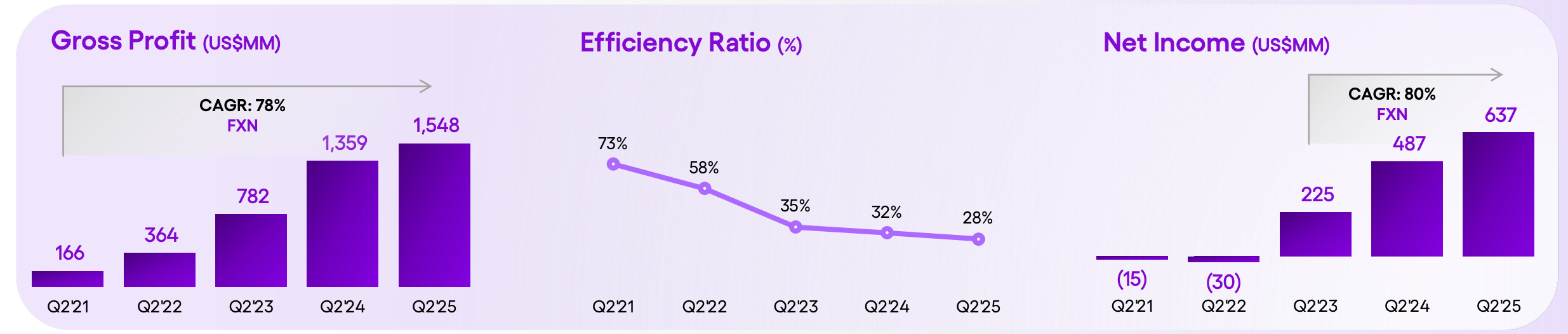

While US neobanks struggle to crack 10MM users and European challengers fight in saturated and over-regulated markets, Nubank has added another 4.1MM customers in Q2 2025, bringing its total to 120MM+ users. The company posted revenues of $3.7B (+40% YoY FXN) and net income of around $640M (+31% YoY). These numbers would be impressive for a century-old institution, let alone a 12-year-old startup.

For comparison, JPM generates $40B of revenue and $15B of profit per quarter.

Nubank is the JPM of Brazil — 60% of Brazil's adult population now banks with Nubank. Back in 2020, Nubank served 25MM customers. Today's 120MM users represent a 5x increase in under five years. JPMorgan Chase has 86MM customers after two centuries in business. But raw customer numbers tell only part of the story, ignoring the large institutional and capital markets arms of the investment bank.

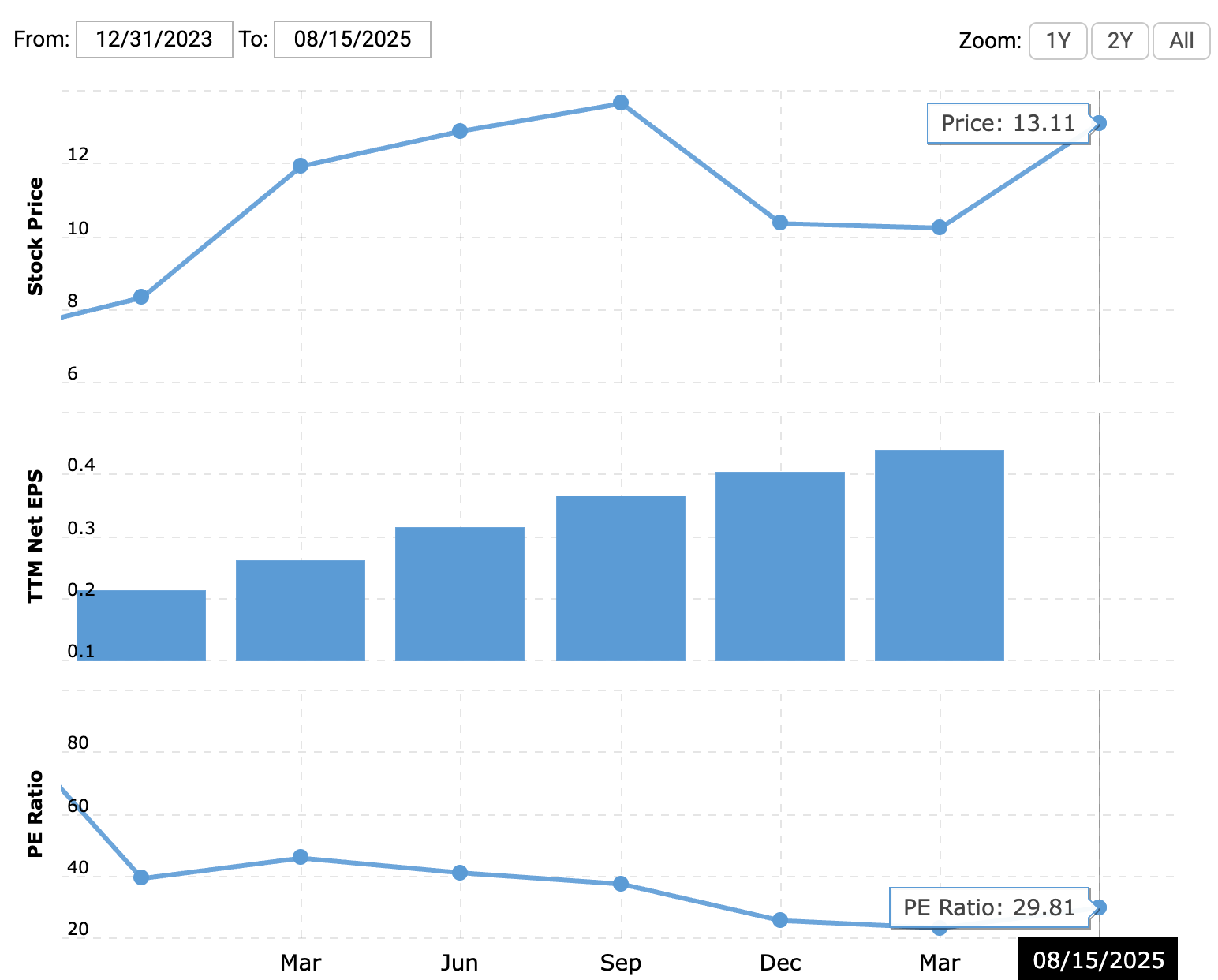

Monthly Average Revenue per Active Customer (ARPAC) crossed $12 for the first time, up from $10.70 just six months ago. Mature user cohorts are generating $27 per month. This suggests Nubank has figured out what eludes most neobanks — how to turn free users into profitable relationships.

The company acquires 30% of new customers through word-of-mouth, then cross-sells them credit cards, personal loans, investments, insurance, and increasingly, crypto products (up 41% YoY in Q2). Note that you cannot build this flywheel without getting into lending, the core risk activity of a bank.

Let’s look at the operational metrics.

Nubank's efficiency ratio hit 28.3%, down from 40% two years ago. Traditional LATAM banks like Itaú and Bradesco operate around 45-50%. US players like Chime are below 35%. Nubank's cost to serve each customer is $0.80 monthly versus $5+ for incumbents.

The digital model doesn’t matter, until it is the only thing that matters.

Deposits reached $36.6B (+41% YoY), while the Interest-Earning Portfolio expanded to $15.7B (+55% YoY). Net interest margin is quite high at 17.7%, but appropriate for the market in which the company operates. Brazil's SELIC rate is 10.5% and credit card APRs average 350% annually.

Such rates that would trigger Congressional hearings in the US, but are standard practice in LATAM.

Geographic expansion is accelerating. Mexico now has 12MM Nubank customers after five years, which is 13% of the adult population. Colombia reached 3MM customers, with deposits surging 840% YoY. These are early signs of penetration in a 650MM person market, where 40% of the population remains unbanked.

The contrast with developed markets is stark.

CashApp plateaued at 57M users, despite Square spending heavily on merchant channels, Bitcoin integration, and celebrity endorsements. Chime, arguably the most comparable US neobank, is heading for an IPO that we estimate will value it around $12-15B.

This is less than a quarter of Nubank's current $63B market cap. There are a number of differences. For example, US interchange is capped at 0.05% versus 0.8-1.2% in Brazil. We have already highlighted the importance of lending and a multi-product portfolio to grow share of wallet.

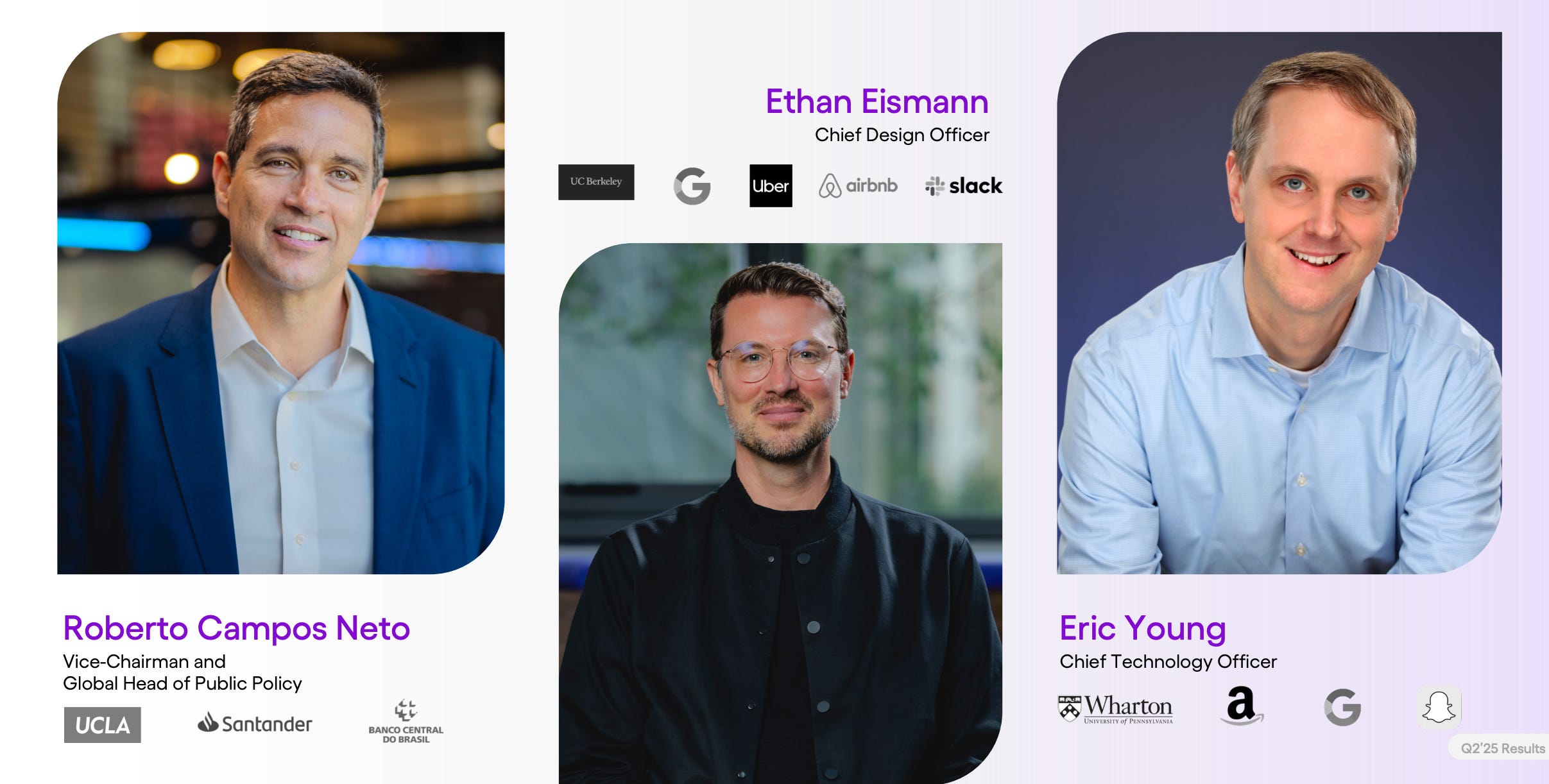

Nubank’s Management is preparing for the next phase.

Roberto Campos Neto, Brazil's former Central Bank Governor, joined as Vice Chairman. This is like Jerome Powell joining JPM. Eric Young arrived from Snap as CTO, which signals investment in AI and automation.

Nubank feels less like an incremental banking company and more like a big tech play as a result. The company uses machine learning to manage credit risk, with 15-90 day NPLs improving to 4.4% despite aggressive lending growth. Of course we should be skeptical, since many banks have tried to lean into this story in the past, only to get re-rated when the numbers don’t deliver. Which is why the numbers remain so important here.

When Berkshire Hathaway sold its entire Nubank position in Q4'24, bears proclaimed the party over. Six months later, that looks like portfolio rebalancing rather than lost confidence. Nubank is generating 28% ROE — nearly double JPMorgan's 15% — while sitting on $4.3B in excess capital.

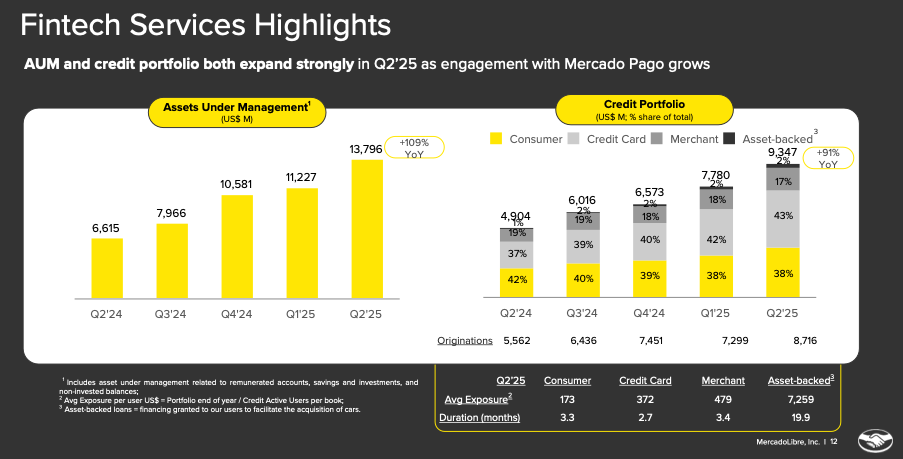

Competition is intensifying, though. Mercado Libre's fintech arm Mercado Pago reached 68MM monthly active users in Q2 (+30% YoY) with its credit portfolio surging 91% to $9.3B, leveraging built-in e-commerce distribution to grow nearly as fast as Nubank. Inter has 33M customers and trades at similar multiples despite being a quarter of Nubank's size. Revolut just landed in Brazil and Mexico with its FX-first playbook.

The moat isn't regulatory or technological, but the speed and quality of execution.

So could Nubank hit a $250B valuation, up from its current $60B? For comparison, JPM sits at $800B with $160B of annual revenue, and BAML is at $300B with $90B of revenue currently. Nubank is annualizing to $6B, which means it needs to grow a lot — maybe to $20B of revenue to get there.

The math is aggressive. There are several levers moving in the right direction: (1) from 120MM to 200MM customers (achievable by 2030 given current growth), (2) $30 ARPAC (mature cohorts are nearly there, up from $12 on average), and (3) 25% margins, that gets us close to a 4x growth. We can also expect a healthy multiple on either profits or revenue, given Nubank’s clean positioning. The stock trades at 30x P/E today, which seems fair given the growth profile.

Brazilian recession or Mexican regulatory problems could halve that growth. Successful LATAM-wide expansion could double it.

Nubank's Q2 results confirm what the numbers have suggested for years; digital banking in emerging markets grows faster than in developed ones. Large underserved populations, favorable unit economics, and incumbent complacency create opportunities that simply don't exist in the US or Europe.

Look at Ant Financial for an earlier lesson in this value creation. The purple card from São Paulo isn't just winning in Brazil. It is now the best case study for global fintech expansion.

👑 Related Coverage 👑

Long Take

We highlight three transformative trends shaping 2025: Ethereum’s 10-year milestone, a sweeping U.S. regulatory pivot toward crypto, and early-stage momentum in humanoid robotics. Ethereum’s decade-long evolution has enabled global digital finance and spawned stablecoins, DeFi, and tokenized securities—now celebrated even at Nasdaq. The SEC and White House have reversed course, launching “Project Crypto” and passing the GENIUS Act to legitimize stablecoins, self-custody, and tokenization, while banning CBDCs and dismantling previous enforcement-first strategies.

Finally, capital is now flowing into hardware robotics, particularly from China, as aging populations and economic strain signal long-term demand for mechanized labor. Together, these trends form a unified trajectory toward a more programmable, decentralized, and autonomous financial and technological future.

Curated Updates

Here are the rest of the updates hitting our radar.

Paytech

⭐ Making Payments Accessible: Wise Platform Pairs With Google - Fintech Magazine

Klarna Is Selling Up to $26 Billion of Buy-Now, Pay-Later Loans to Nelnet - Bloomberg

Citigroup considers custody and payment services for stablecoins, crypto ETFs - Reuters

Visa expands Click to Pay across Apac - Finextra

Neobanks

Lending

⭐ Private Credit-Powered AI boom at Risk of Overheating, UBS says - Bloomberg

Crypto lending firm Figure Technology files for Nasdaq IPO - Silicon Angle

Digital Investing

⭐Circle Acquires Malachite to Power Its Upcoming Arc Blockchain - YahooFinance

Perella Weinberg eyes European tech push as AI, fintech drives deals - FN London

EToro to Add Tokenization and AI Tools to Trading and Investing Platform - PYMNTS

🚀 Level Up

Join our Premium community and receive all the Fintech and Web3 intelligence you need to level up your career. Get access to Long Takes, archives, and special reports.

Sponsor the Fintech Blueprint and reach over 200,000 professionals.

👉 Reach out here.Check out our AI newsletter, the Future Blueprint, 👉 here.

Read our Disclaimer here — this newsletter does not provide investment advice

@Matt Low do you think if NuBank expands into Europe they could take on all the digital bank competition from Revolut?

Or you could choose Newtek?

- 5.12x P/E

- 17% revenue CAGR

- Funding mix shifting to deposits away from private capital, so has a faster margin expansion

- counter-cyclical growth

Would love to hear your thoughts